The Bull Case For Flowserve (FLS) Could Change Following Mixed Q1 2026 Beat And Guidance Reaffirmation

Flowserve Corporation FLS | 0.00 |

- Flowserve Corporation has reported past first-quarter 2026 results, with sales of US$1,068.27 million versus US$1,144.54 million a year earlier, while net income rose to US$81.68 million and diluted EPS from continuing operations increased to US$0.64 from US$0.56.

- Despite the year-on-year sales decline and a miss versus analyst revenue expectations, Flowserve delivered EPS above forecasts and reaffirmed its full-year adjusted EPS guidance, highlighting management’s focus on profitability and cost control.

- Next, we’ll consider how Flowserve’s EPS beat and maintained full-year guidance may influence its investment narrative built around margin progress.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Flowserve Investment Narrative Recap

To own Flowserve, you generally need to believe that its margin progress and exposure to long cycle energy, nuclear, and water projects can translate into higher, more stable earnings, even if revenue growth is choppy. The latest quarter fits that narrative: revenue missed expectations and fell year on year, but EPS came in ahead of forecasts and full year adjusted EPS guidance was reaffirmed, so the core near term catalyst around margin execution looks largely intact, while project timing and order volatility remain key risks.

In that context, the April 15 refinancing of Flowserve’s credit facilities is worth noting. Locking in a US$1,000 million revolving facility and a US$450 million term loan through 2031 gives the company added financial flexibility around working capital, project execution, and ongoing cost programs, which ties directly into the margin and earnings story that underpins the current investment case, even as revenue volatility and project delays remain in focus.

Yet against this earnings resilience, investors still need to consider how project delays and tariff related cost pressures could affect Flowserve’s ability to...

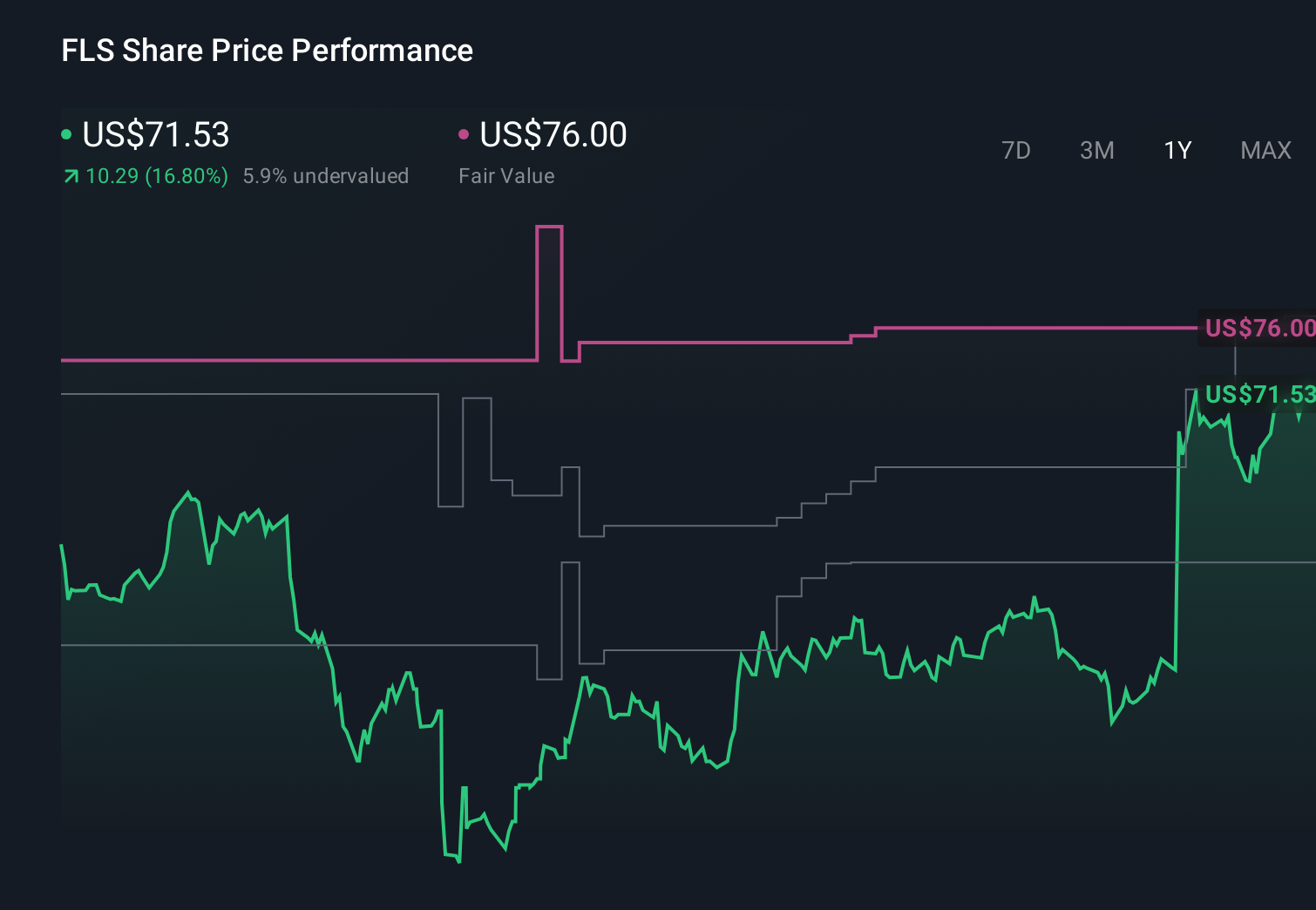

Flowserve's narrative projects $5.6 billion revenue and $660.0 million earnings by 2029.

Uncover how Flowserve's forecasts yield a $94.80 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Compared with the consensus, the most cautious analysts were already baking in only about 3.5 percent annual revenue growth and US$586.6 million of earnings by 2028, reflecting deeper worries about tariffs and macro risk. With Q1 revenue down and EPS ahead of forecasts, you can now weigh whether that more pessimistic view still fits, or if the margin story and recent results suggest a wider range of possible outcomes.

Explore 5 other fair value estimates on Flowserve - why the stock might be worth as much as 21% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Flowserve research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Flowserve research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Flowserve's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 53 companies with promising cash flow potential yet trading below their fair value.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.