The Bull Case For General Dynamics (GD) Could Change Following New U.S. Defense Sustainment Contracts – Learn Why

General Dynamics GD | 0.00 |

- General Dynamics recently secured a US$106 million task order from the U.S. Space Systems Command for long-term sustainment support and a US$39.19 million Navy personnel-system contract modification, reinforcing its role in critical defense infrastructure and secure communications.

- These awards, combined with solid cash generation, shareholder returns, and a robust contract backlog, underline how General Dynamics converts consistent contract wins into durable revenue visibility and operational strength across its Marine Systems, Aerospace, and technology-focused divisions.

- Against this backdrop of fresh defense contract wins and reinforced backlog visibility, we’ll examine how these developments influence General Dynamics’ investment narrative.

Find 46 companies with promising cash flow potential yet trading below their fair value.

General Dynamics Investment Narrative Recap

To own General Dynamics, you need to believe its mix of Marine Systems, Aerospace, and defense IT can keep translating contract wins and backlog into steady cash generation and shareholder returns. The recent US$106 million Space Systems Command task order and US$39.19 million Navy personnel-system modification support near term revenue visibility, but do not materially change the key short term catalyst, which remains execution on large Marine and Aerospace programs, or the main risk around supply chain and program delays.

The Space Systems Command task order, which runs with options out to 2031, is most relevant here because it reinforces General Dynamics’ role in secure communications and long-cycle defense infrastructure. It ties directly into the company’s broader catalyst of growing demand for IT modernization and cyber resilient systems in the Mission Systems and GDIT divisions, helping support the investment case that recurring, service oriented defense work can complement more cyclical aircraft and shipbuilding programs.

Yet, against this backdrop of long dated contracts and cash generation, investors still need to consider the risk that persistent supply chain instability in Marine Systems could...

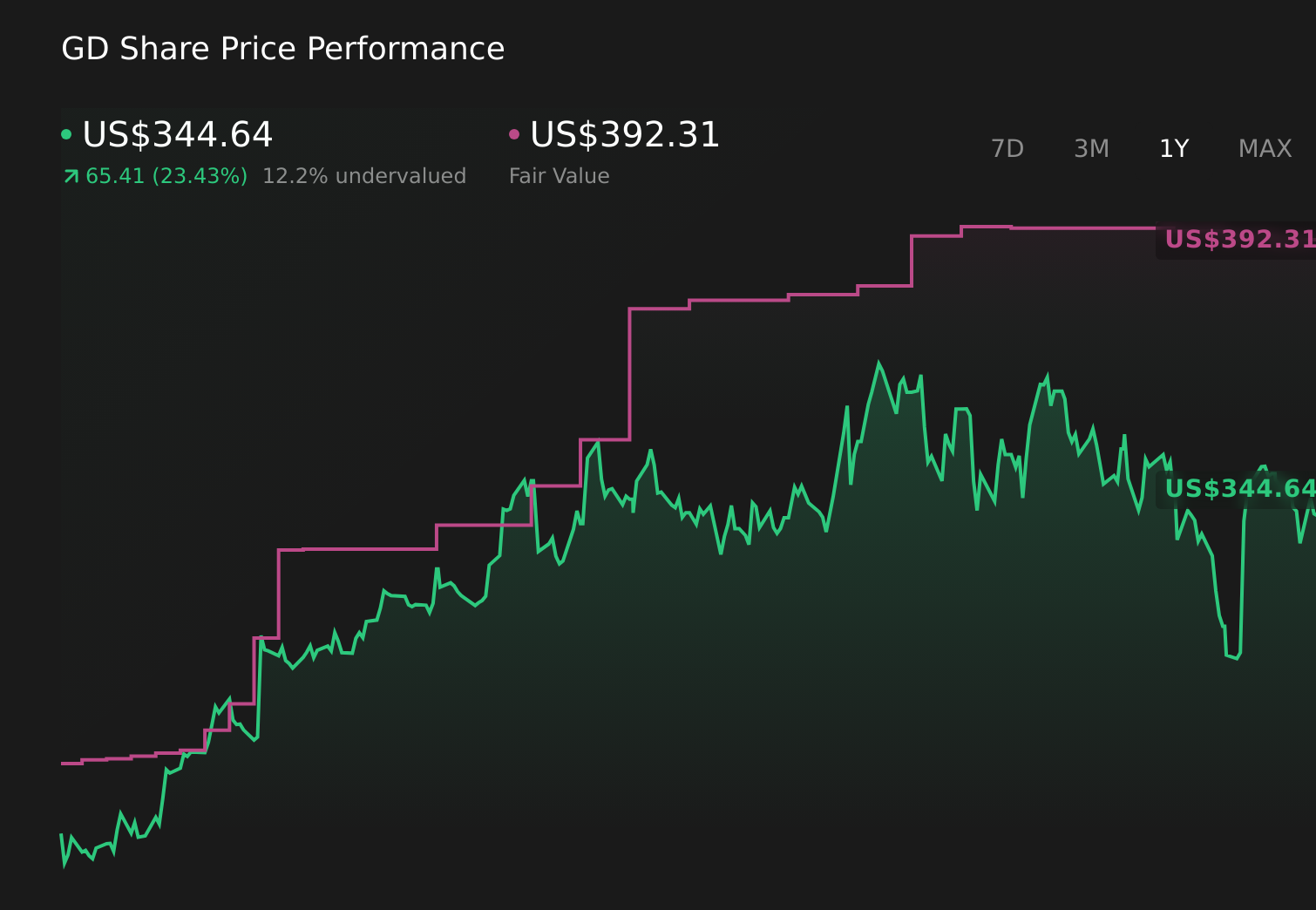

General Dynamics' narrative projects $60.7 billion revenue and $5.4 billion earnings by 2029. This requires 4.1% yearly revenue growth and about a $1.1 billion earnings increase from $4.3 billion today.

Uncover how General Dynamics' forecasts yield a $392.31 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community currently place General Dynamics’ fair value tightly between US$392.22 and US$405.74 per share. You can weigh these views against the company’s reliance on multi year defense backlogs, and consider how any slowdown in contract awards or program execution could affect the longer term earnings profile.

Explore 3 other fair value estimates on General Dynamics - why the stock might be worth as much as 17% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your General Dynamics research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free General Dynamics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Dynamics' overall financial health at a glance.

Curious About Other Options?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.