The Bull Case For Insmed (INSM) Could Change Following New Brinsupri Data And Hiring Push - Learn Why

Insmed Incorporated INSM | 0.00 |

- At the 2026 American Thoracic Society conference held earlier this year, Insmed showcased encouraging post‑hoc Phase III data for Brinsupri, its first‑to‑market DPP‑1 inhibitor for non‑cystic fibrosis bronchiectasis, while also granting inducement stock awards to 103 new employees under its 2025 Inducement Plan.

- The combination of positive clinical signals for Brinsupri and expanded equity‑based hiring underscores Insmed’s effort to build both medical leadership and internal capabilities around bronchiectasis.

- We’ll now examine how Brinsupri’s Phase III symptom data at a major respiratory conference may influence Insmed’s existing investment narrative.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Insmed Investment Narrative Recap

To own Insmed, you need to believe that BRINSUPRI can become a meaningful bronchiectasis franchise while ARIKAYCE and TPIP broaden the respiratory portfolio. The latest ATS symptom data and new‑hire inducement grants support this core story but do not appear to change the near term focus on BRINSUPRI’s U.S. launch timing or the key risk around payer access and real world adoption.

Among recent announcements, the positive Phase IIIb ENCORE readout for ARIKAYCE in newly diagnosed MAC lung disease is most relevant. Together with the ATS BRINSUPRI data, it highlights how Insmed is working to strengthen its respiratory footprint ahead of potential label expansion filings, which could become important secondary catalysts alongside the first full commercial year of BRINSUPRI.

Yet, while the ATS data are encouraging, investors should still watch how payer decisions could tighten BRINSUPRI access and potentially reshape expectations...

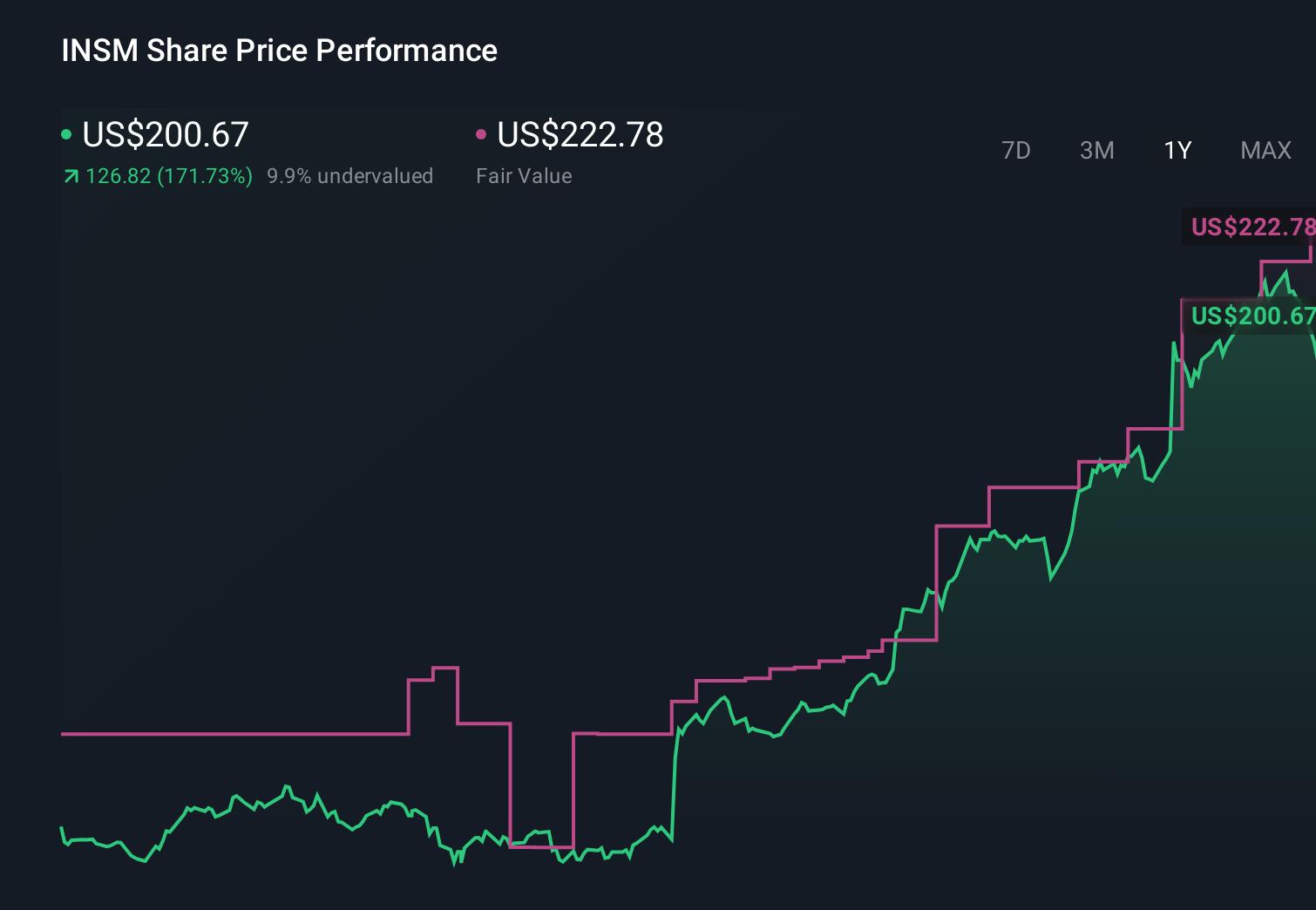

Insmed's narrative projects $4.2 billion revenue and $1.1 billion earnings by 2029. This requires 71.9% yearly revenue growth and about a $2.3 billion earnings increase from -$1.2 billion today.

Uncover how Insmed's forecasts yield a $200.00 fair value, a 91% upside to its current price.

Exploring Other Perspectives

Some analysts were already assuming BRINSUPRI could help lift revenue toward about US$5.2 billion by 2029, so this new ATS data might either reinforce that optimism or prompt you to rethink how uptake, payer behavior, and long term earnings could differ from those best case forecasts.

Explore 4 other fair value estimates on Insmed - why the stock might be a potential multi-bagger!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Insmed research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Insmed research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Insmed's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 13 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.