The Bull Case For Krystal Biotech (KRYS) Could Change Following UK Vyjuvek Approval And Rising Profitability

Krystal Biotech, Inc. KRYS | 0.00 |

- In May 2026, Krystal Biotech received Medicines and Healthcare products Regulatory Agency approval in the UK for Vyjuvek, its gene therapy for dystrophic epidermolysis bullosa, and also reported first-quarter 2026 net income of US$55.93 million with higher earnings per share than a year earlier.

- This combination of new market access for Vyjuvek and rising profitability strengthens Krystal Biotech’s position in rare genetic disease treatments and adds a fresh dimension to its growth profile.

- We’ll now examine how UK approval of Vyjuvek, expanding its rare-disease footprint, could influence Krystal Biotech’s existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 17 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Krystal Biotech Investment Narrative Recap

To own Krystal Biotech, you need to believe VYJUVEK can anchor a durable rare-disease franchise while the pipeline gradually reduces single-product dependence. The UK approval adds another market for VYJUVEK, which could support the near term catalyst of international expansion, but it does not remove the key risk of revenue “waviness” from variable treatment patterns and heavy reliance on one commercial asset.

The most relevant recent update here is Krystal’s first quarter 2026 earnings, with net income of US$55.93 million and higher earnings per share than a year earlier. This profitability, alongside new UK market access, gives the company more financial flexibility to support ongoing launches in Europe and Japan, but it also heightens the importance of how stable VYJUVEK demand proves to be as Krystal invests in its broader pipeline.

But even with UK approval in hand, investors should be aware that VYJUVEK’s quarter to quarter revenue “waviness” could still...

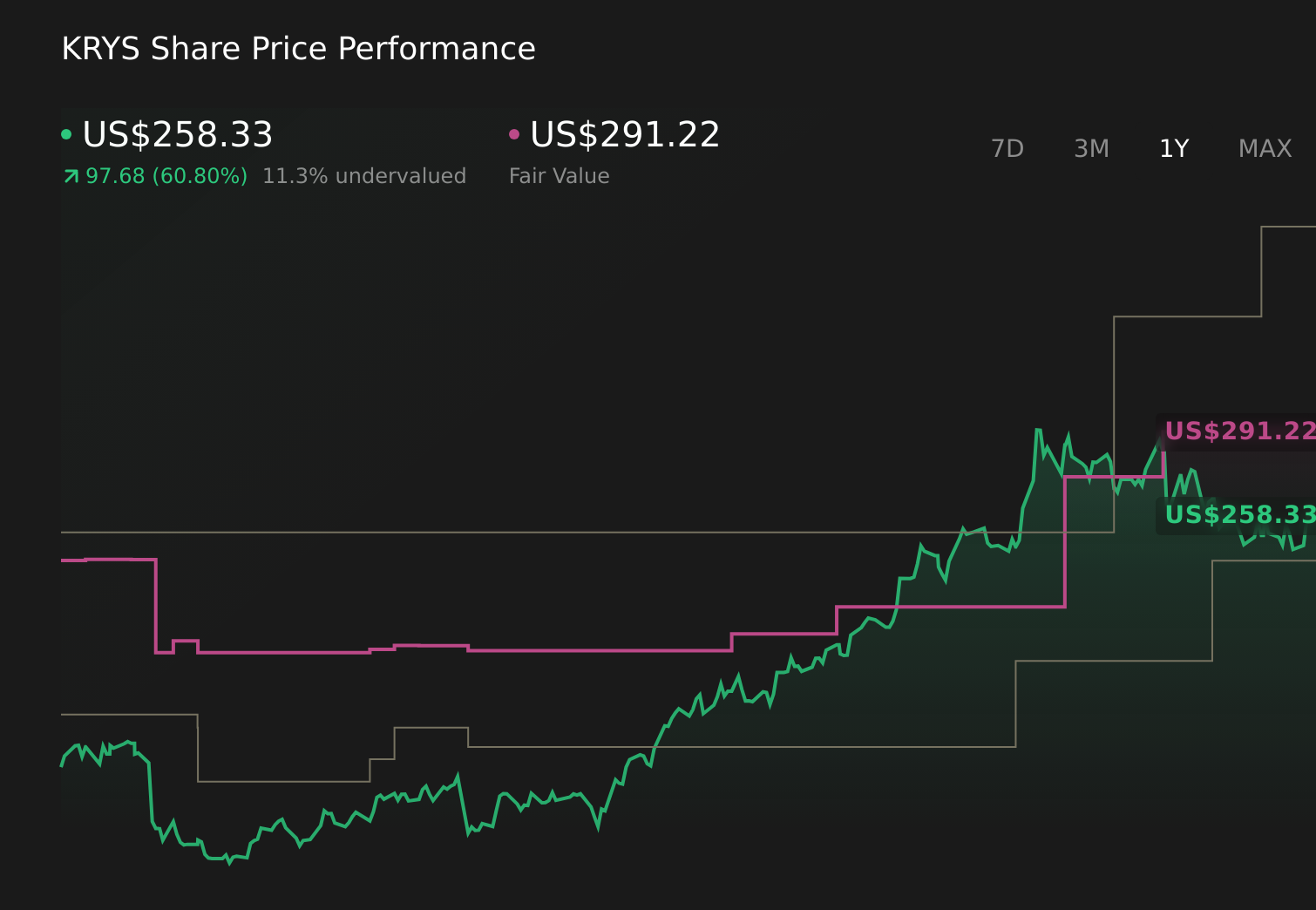

Krystal Biotech's narrative projects $987.9 million revenue and $571.3 million earnings by 2029. This requires 36.4% yearly revenue growth and an earnings increase of about $366.5 million from $204.8 million today.

Uncover how Krystal Biotech's forecasts yield a $315.00 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts, who were already modeling revenue of about US$1.4 billion and earnings near US$947 million by 2029, see UK approval as a potential accelerant, while others worry that ongoing VYJUVEK sales variability might still temper how those forecasts evolve from here.

Explore 6 other fair value estimates on Krystal Biotech - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Krystal Biotech research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Krystal Biotech research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Krystal Biotech's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.