The Bull Case For Lucid Group (LCID) Could Change Following Mixed 2025 Results And 2026 Guidance

Lucid LCID | 9.96 | +4.18% |

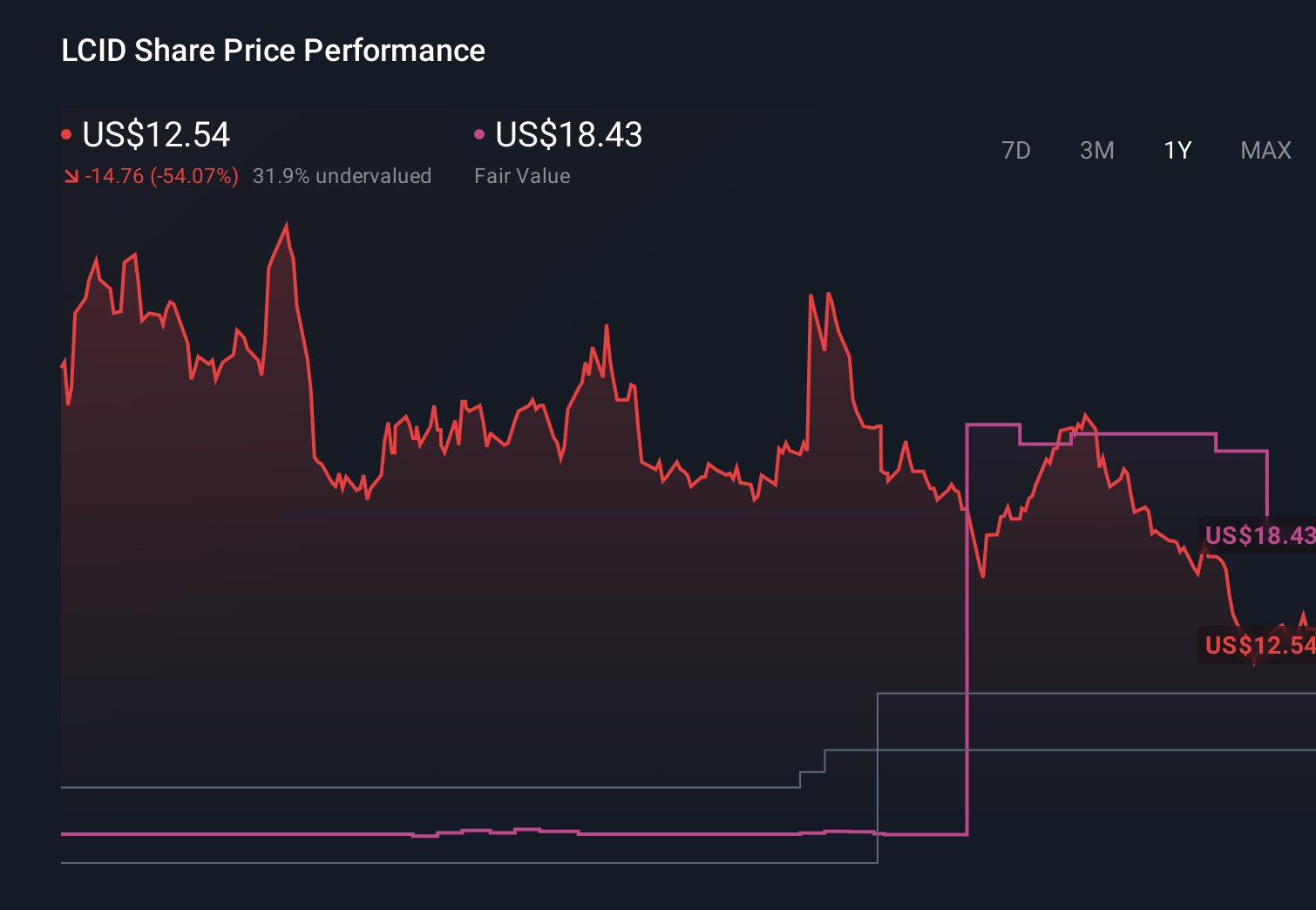

- In late February 2026, Lucid Group reported fourth-quarter and full-year 2025 results showing sharply higher sales but continued very large net losses, and it issued 2026 production guidance of 25,000–27,000 vehicles.

- The combination of rising revenue, persistent heavy losses, and fresh production targets has sharpened investor focus on whether Lucid can eventually scale profitably.

- Next, we’ll examine how Lucid’s continued heavy losses, despite stronger sales, may reshape the previously optimistic investment narrative around future profitability.

Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

Lucid Group Investment Narrative Recap

To own Lucid today, you have to believe its technology, brand and partnerships can eventually turn growing sales into a sustainable, profitable EV business. The latest results, with sharply higher 2025 revenue but an even larger quarterly net loss and 2026 production guidance of 25,000 to 27,000 vehicles, put the near term spotlight on one thing: whether Lucid can scale production without its cash burn and dilution risk becoming unmanageable. That tension now sits at the center of the story.

The most relevant recent development here is Lucid’s 2026 production guidance alongside its Q4 2025 earnings. Full year sales rose to US$1,353.79 million, but the company still lost US$2,698.05 million, and Q4 alone saw an US$814.02 million net loss. Against ambitious catalysts like the Uber and Nuro robotaxi partnership, this mix of rising volume and persistent losses will likely influence how much confidence you place in those longer term growth plans.

Yet investors should also be aware that while revenue is growing, Lucid’s continued heavy losses and reliance on external capital mean the real risk may be...

Lucid Group's narrative projects $5.6 billion revenue and $285.8 million earnings by 2028.

Uncover how Lucid Group's forecasts yield a $16.67 fair value, a 65% upside to its current price.

Exploring Other Perspectives

Compared with the baseline story, the lowest analysts were already more cautious, assuming about US$3.3 billion of revenue and only US$167.4 million of earnings by 2028, so this latest update could either reinforce or soften their view depending on how you interpret Lucid’s worsening losses alongside its chosen path to scaling production.

Explore 8 other fair value estimates on Lucid Group - why the stock might be worth less than half the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Lucid Group research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Lucid Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lucid Group's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.