The Bull Case For MasTec (MTZ) Could Change Following Upgraded 2026 Guidance And Margin Improvement – Learn Why

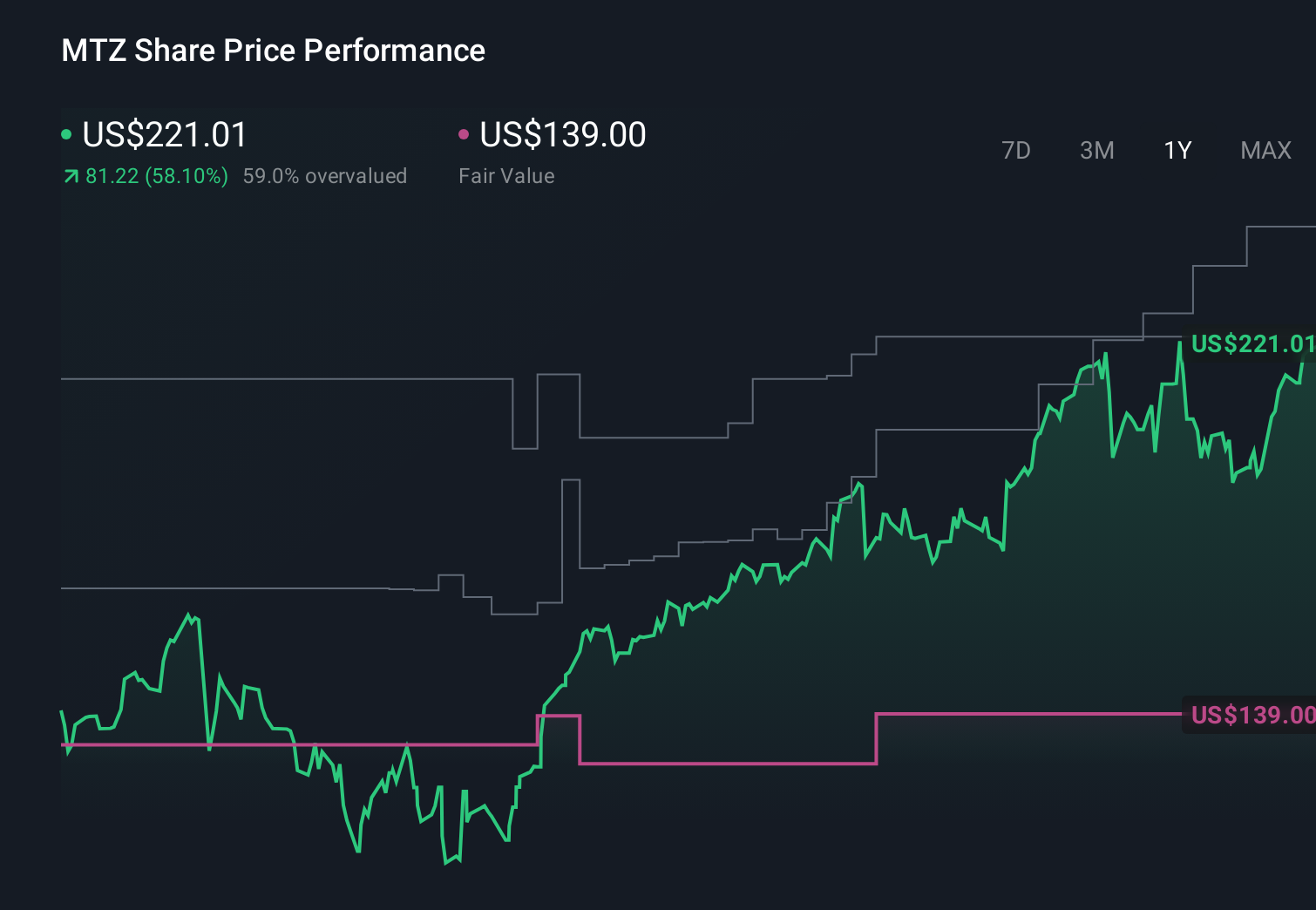

MasTec, Inc. MTZ | 0.00 |

- MasTec, Inc. has already reported its Q1 2026 results, posting sales of US$3,828.8 million and net income of US$60.84 million, with basic EPS from continuing operations of US$0.78, all higher than the same period last year.

- Alongside stronger earnings, MasTec lifted its full-year revenue and Adjusted EPS guidance, while highlighting higher operating margins and a growing backlog, which together point to increased visibility on future project activity.

- We’ll now examine how MasTec’s upgraded full-year guidance and margin improvement influence its existing investment narrative and forward-looking assumptions.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

MasTec Investment Narrative Recap

To own MasTec, I think you need to believe in its role as a large-scale infrastructure builder across communications, power, clean energy and pipelines, and in its ability to turn a large backlog into profitable work. The latest quarter’s stronger revenue and net income, plus raised full-year guidance and better margins, support the near term catalyst of improved earnings quality, while the biggest current risk still looks like execution on a rapidly growing project book and cost base.

The most relevant recent announcement here is MasTec’s February 26 guidance for Q1 and FY 2026, which the company has now exceeded on sales and net income in Q1. This beat, alongside higher full-year revenue and Adjusted EPS guidance following the result, directly ties into the catalyst of backlog conversion and margin improvement, but it does not remove the underlying risks around project execution, client concentration, and the impact of any delays or cancellations in key end markets.

Yet beneath the stronger Q1 numbers, investors should still be watching how execution risk around that enlarged backlog could begin to affect...

MasTec's narrative projects $20.3 billion revenue and $880.9 million earnings by 2029.

Uncover how MasTec's forecasts yield a $348.72 fair value, a 12% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue of about US$20.6 billion and earnings near US$814 million by 2029, so this Q1 beat may prompt them to revisit how much execution and political risk they are baking in compared with the more optimistic narrative you have just read.

Explore 6 other fair value estimates on MasTec - why the stock might be worth as much as $348.72!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MasTec research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MasTec research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MasTec's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.