The Bull Case For MercadoLibre (MELI) Could Change Following New AI Initiatives And Insider Buying - Learn Why

MercadoLibre, Inc. MELI | 0.00 |

- In early May 2026, MercadoLibre confirmed it had released its Q1 2026 results on May 7 and held a video conference, call, and webcast to discuss performance across its Latin American e-commerce and fintech ecosystem.

- Analysts and data providers highlighted mixed earnings estimate revisions but pointed to ongoing product innovation, AI-driven initiatives, and insider buying as reasons for sustained interest in MercadoLibre’s integrated commerce and payments platform.

- We’ll now examine how optimism around AI-driven product innovation and ecosystem growth could influence MercadoLibre’s existing investment narrative.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

MercadoLibre Investment Narrative Recap

To own MercadoLibre, you need to believe its Latin American e commerce and fintech ecosystem can keep deepening user engagement and monetization despite volatile macro conditions and rising competition. The near term catalyst is how Q1 2026 results and AI initiatives shape confidence in sustained ecosystem growth. Recent mixed estimate revisions, reduced price targets, and a Zacks Strong Sell view raise near term concern, but do not yet fundamentally alter the core long term thesis.

Against this backdrop, MercadoLibre’s plan to invest US$3.4 billion in Argentina in 2026 stands out. It ties directly into the key catalyst of ecosystem expansion by funding logistics, distribution centers, and Mercado Pago’s growth. At the same time, such heavy spending in a volatile market intersects with the biggest current risk around credit quality and profitability, especially if economic conditions or currency swings make it harder to translate usage growth into resilient earnings.

Yet behind the optimism around AI and ecosystem growth, investors should be aware of how rising credit exposure in volatile markets could...

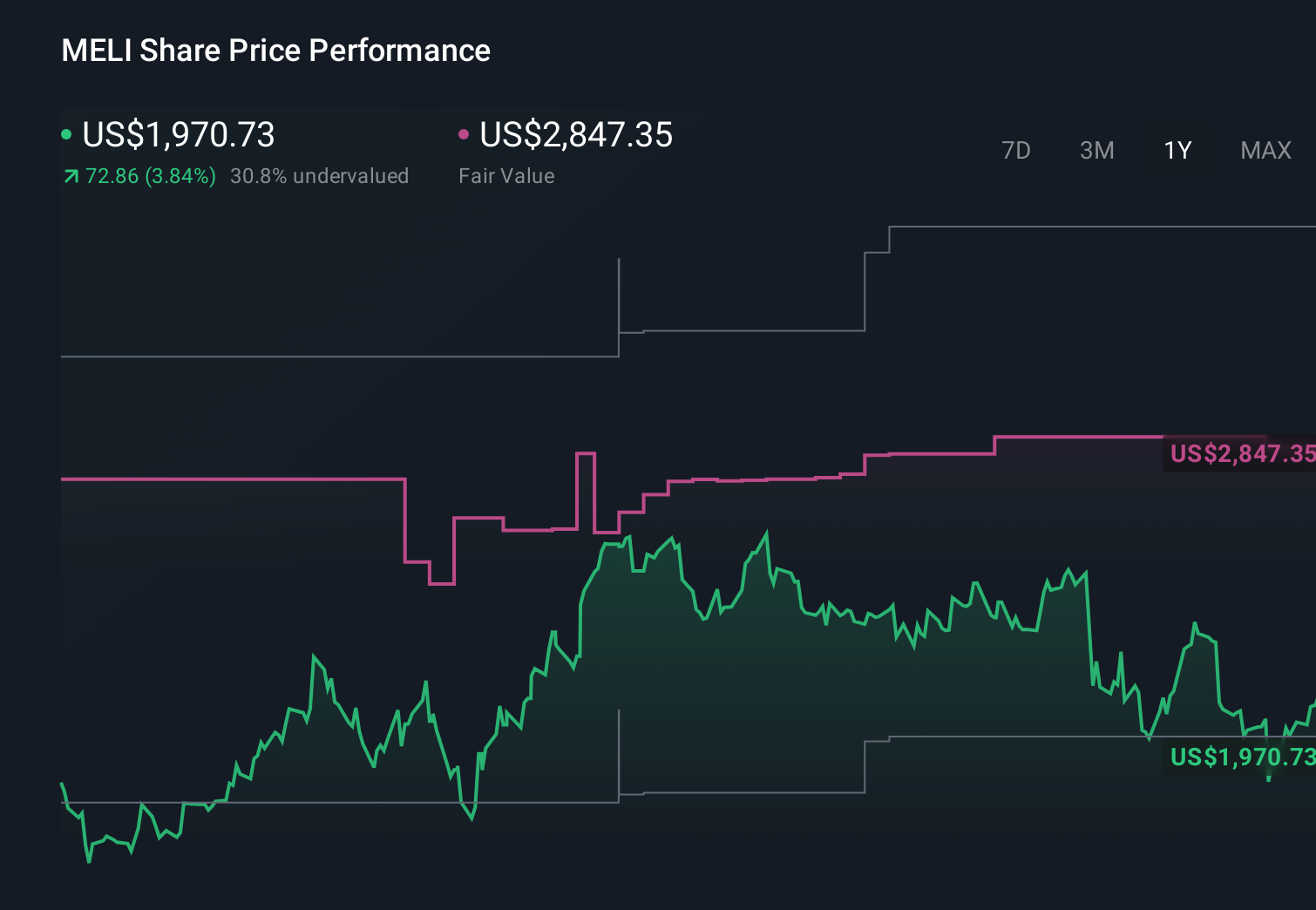

MercadoLibre's narrative projects $57.9 billion revenue and $4.8 billion earnings by 2029. This requires 26.1% yearly revenue growth and a $2.8 billion earnings increase from $2.0 billion today.

Uncover how MercadoLibre's forecasts yield a $2440 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming revenue of about US$55.6 billion and earnings near US$4.4 billion by 2029, yet they still warn that rising logistics and compliance costs, combined with intensifying regional competition, could leave far less room for margins to improve than the latest AI optimism might suggest, which is why it is worth comparing several viewpoints before you decide how this new information fits your own expectations.

Explore 28 other fair value estimates on MercadoLibre - why the stock might be worth just $1827!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MercadoLibre research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free MercadoLibre research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MercadoLibre's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.