The Bull Case For Moelis (MC) Could Change Following Renewed U.S.-China Optimism And Institutional Support

Moelis & Co. Class A MC | 0.00 |

- In recent days, Moelis & Company was lifted by optimism following a U.S.-China trade summit and supportive U.S. economic data, which together improved investor confidence in advisory-focused financial firms.

- At the same time, Kayne Anderson Rudnick Investment Management reaffirmed its sizeable passive ownership in Moelis, underscoring ongoing institutional interest in the firm’s advisory franchise.

- Next, we’ll examine how renewed optimism around U.S.-China relations could influence Moelis’ existing investment narrative and outlook on advisory activity.

We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Moelis Investment Narrative Recap

To own Moelis, you need to believe that its advisory-focused model can turn periods of stronger macro and cross border activity into steadier fees, despite inherent deal cycle swings. The latest U.S. China trade thaw and firmer U.S. data support the near term catalyst of a healthier M&A and financing calendar, but they do not remove the key risk that revenues remain volatile if this window closes or fails to translate into completed transactions.

The most relevant recent announcement in this context is Moelis’ continued capital return through its 2026 share repurchase plan, with US$51.13 million of stock bought back in Q1 2026. For investors, this matters because it tightens the share count at a time when advisory pipelines could benefit from improved sentiment, but it also leans on cash flows that still depend heavily on transaction fees rather than recurring revenue.

Yet while optimism is improving, investors should be aware that Moelis’ deal driven model still leaves it exposed if...

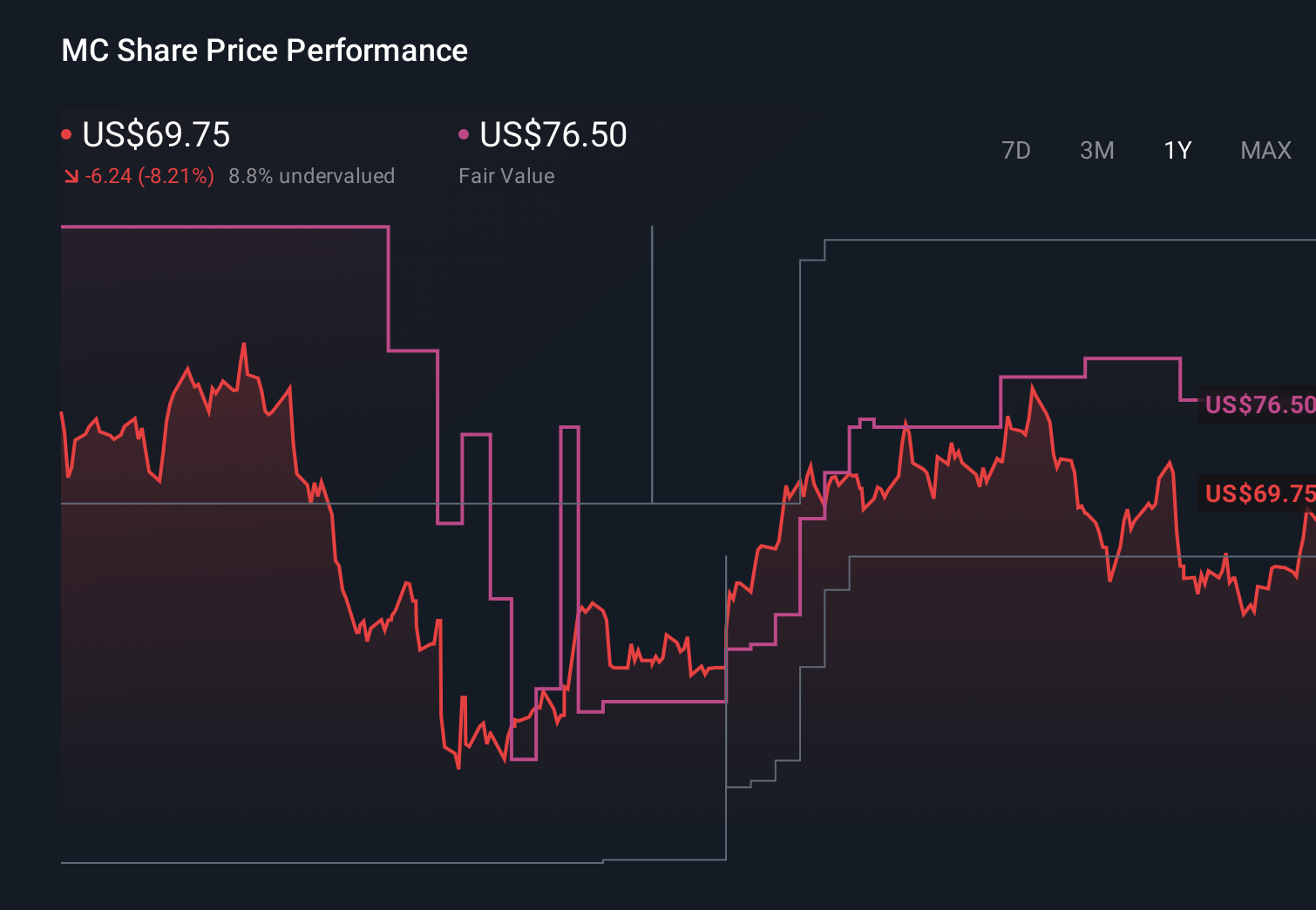

Moelis' narrative projects $2.1 billion revenue and $381.7 million earnings by 2028. This requires 15.3% yearly revenue growth and a $183.6 million earnings increase from $198.1 million today.

Uncover how Moelis' forecasts yield a $76.50 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts look much more cautious than the consensus, even before this news, with revenue expectations around US$2.3 billion and earnings near US$462.9 million by 2029, and they worry that digital capital access could structurally pressure Moelis’ advisory fees compared with the baseline focus on cyclical deal flow recovery, so it is worth weighing how this latest trade and macro shift might challenge or support both views.

Explore 3 other fair value estimates on Moelis - why the stock might be worth just $76.50!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Moelis research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Moelis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Moelis' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 42 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.