The Bull Case For Netflix (NFLX) Could Change Following Live Breakfast Club And Wonka Brand Push

Netflix NFLX | 0.00 |

- In May 2026, iHeartMedia and Netflix expanded their video podcast partnership so that The Breakfast Club began streaming live on Netflix each weekday, while Netflix also deepened its kids and family push through new Wonka-themed collaborations with Ferrero and toy lines with Moose Toys.

- These moves highlight how Netflix is extending its franchises beyond the screen, into live creator-driven formats and licensed consumer products, to broaden engagement around its content.

- Next, we’ll examine how adding a daily live version of The Breakfast Club may influence Netflix’s investment narrative around content and advertising.

This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

Netflix Investment Narrative Recap

To own Netflix today, you need to believe it can keep turning its global content engine and new ad tier into steady, profitable growth despite rising competition and content spend. The recent iHeartMedia partnership and Wonka consumer products are directionally helpful for engagement, but they do not materially change the near term focus on scaling advertising and managing content costs, or the key risk that those costs rise faster than revenue.

The daily live launch of The Breakfast Club on Netflix is especially relevant because it sits at the intersection of content and advertising. It expands creator driven programming that can deepen habitual viewing and potentially support future ad inventory, while also testing Netflix’s live infrastructure. How well Netflix integrates this kind of always on show with its broader content slate could matter for both engagement and monetization trends.

Yet, against this backdrop of experimentation, investors should also be aware of the risk that escalating content costs and competitive pressure may eventually...

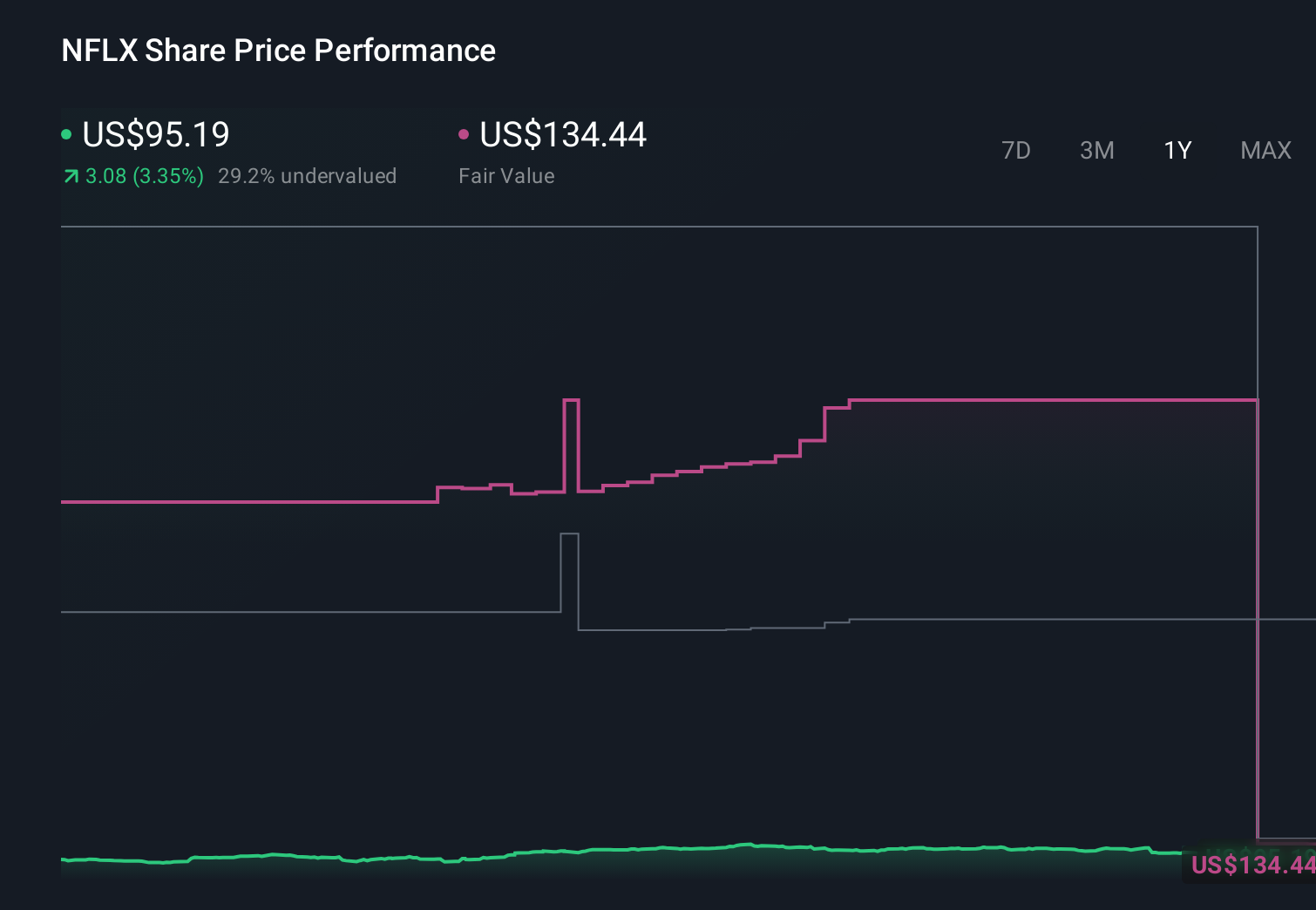

Netflix’s narrative projects $64.7 billion revenue and $19.7 billion earnings by 2029. This requires 11.3% yearly revenue growth and a roughly $6.3 billion earnings increase from $13.4 billion today.

Uncover how Netflix's forecasts yield a $114.56 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts paint a much harsher picture than the consensus, even before this news, with revenue only reaching about US$61.4 billion and earnings about US$16.8 billion by 2029, reminding you that views on issues like rising content costs and attention shifting to alternatives can differ widely and may need revisiting as initiatives such as live podcasts and new consumer products unfold.

Explore 27 other fair value estimates on Netflix - why the stock might be worth just $90.80!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Netflix research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Netflix research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Netflix's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.