The Bull Case For Photronics (PLAB) Could Change Following Advanced Korea AMOLED Mask Writer Upgrade

Photronics, Inc. PLAB | 40.49 40.49 | -0.88% 0.00% Pre |

- Photronics recently took delivery of what it calls the most advanced flat panel display mask writer at its Korea facility, with installation completed after the second quarter of 2026 to support cutting-edge AMOLED and Gen 8.6 photomasks.

- This upgrade materially enhances the precision, stability and throughput of Photronics’ display photomask production, potentially strengthening its role in enabling higher-resolution, brighter, faster-refresh displays for customers.

- We’ll now explore how this advanced Korea mask writer investment could influence Photronics’ existing investment narrative around technology upgrades and growth.

AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Photronics Investment Narrative Recap

To own Photronics, you need to believe in its role as an essential supplier of high end photomasks for both IC and advanced displays, while accepting heavy, ongoing capital spending and cyclical end‑market swings. The new Korea mask writer fits this thesis by reinforcing its technology position in AMOLED and Gen 8.6 display masks, but it does not remove near term risks around demand visibility, customer concentration in Asia, or the strain that elevated capex can place on cash generation.

Against this backdrop, the recent Q1 2026 results and Q2 revenue guidance of US$212 million to US$220 million are an important reference point, because they show how Photronics is currently translating past investment into revenue and earnings. When you set those figures alongside the new mask writer outlay in Korea, the key question becomes how effectively future demand for advanced AMOLED and IT OLED masks will support returns on the company’s higher capital base.

Yet while the technology story is appealing, investors should also be aware of the rising capital intensity and what happens if...

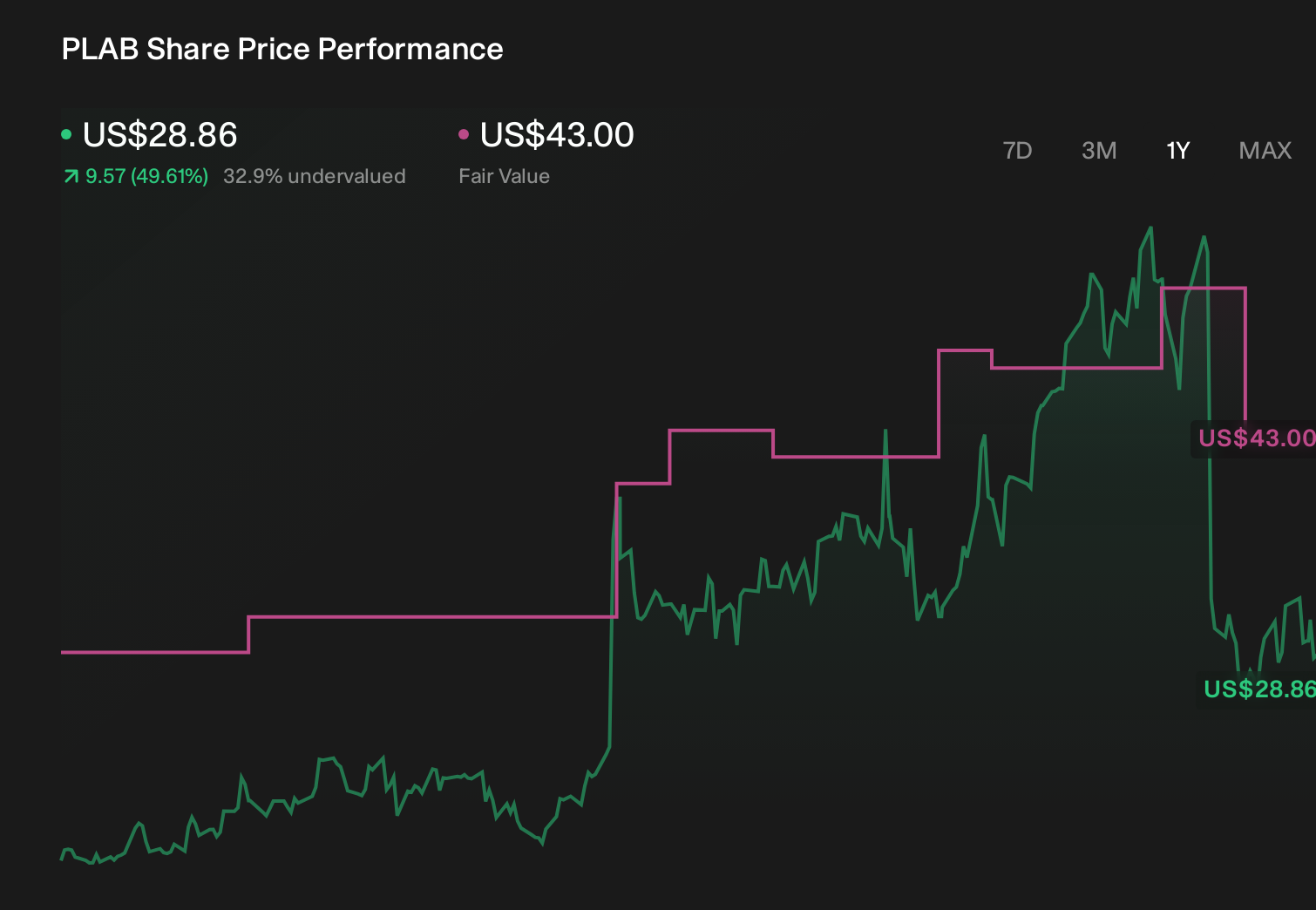

Photronics' narrative projects $973.4 million revenue and $138.1 million earnings by 2029. This requires 4.1% yearly revenue growth and a modest $1.6 million earnings increase from $136.5 million today.

Uncover how Photronics' forecasts yield a $47.00 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Eight members of the Simply Wall St Community currently see fair value for Photronics between US$19.08 and US$47. In light of this spread, the new Korea mask writer underscores how technology upgrades can amplify both the potential benefits of high end demand and the financial risk of sustained heavy capex, so it is worth weighing several viewpoints before deciding how this fits into your own expectations.

Explore 8 other fair value estimates on Photronics - why the stock might be worth as much as 15% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Photronics research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Outshine the giants: these 22 early-stage AI stocks could fund your retirement.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 26 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.