The Bull Case For Plexus (PLXS) Could Change Following Major Credit Facility Expansion - Learn Why

Plexus Corp. PLXS | 0.00 |

- Plexus Corp. recently entered into a Second Amended and Restated Credit Agreement, replacing its 2022 facility with a revolving credit line of up to US$500 million, extendable to US$750 million, and pushing the maturity date out to June 5, 2031.

- The extended term, larger borrowing capacity and covenant structure tied to leverage and interest coverage ratios give Plexus added financial flexibility that could influence how it funds operations, acquisitions and global expansion over the coming years.

- We’ll now examine how this expanded revolving credit capacity and longer-dated funding may reshape Plexus’s existing investment narrative and risk profile.

AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Plexus Investment Narrative Recap

To own Plexus, you need to believe it can keep winning complex, higher value manufacturing and engineering programs in healthcare, industrial and aerospace and defense, while managing customer concentration, cyclical demand and margin pressure. The new US$500 million revolving credit facility (expandable to US$750 million) mainly strengthens liquidity and funding optionality; it could support near term growth initiatives, but it does not materially change the immediate demand driven revenue and margin risks.

The recent Riverside Research partnership in intelligence and defense markets is especially relevant here, as it highlights Plexus’s push into secure, complex aerospace and defense hardware that can deepen customer relationships. When viewed alongside the expanded credit facility, investors may focus on how additional funding flexibility could support similar high complexity program ramps, which are central to the current growth catalyst narrative.

Yet while Plexus’s new credit line increases flexibility, investors should still be aware of how rising working capital and inventory levels could...

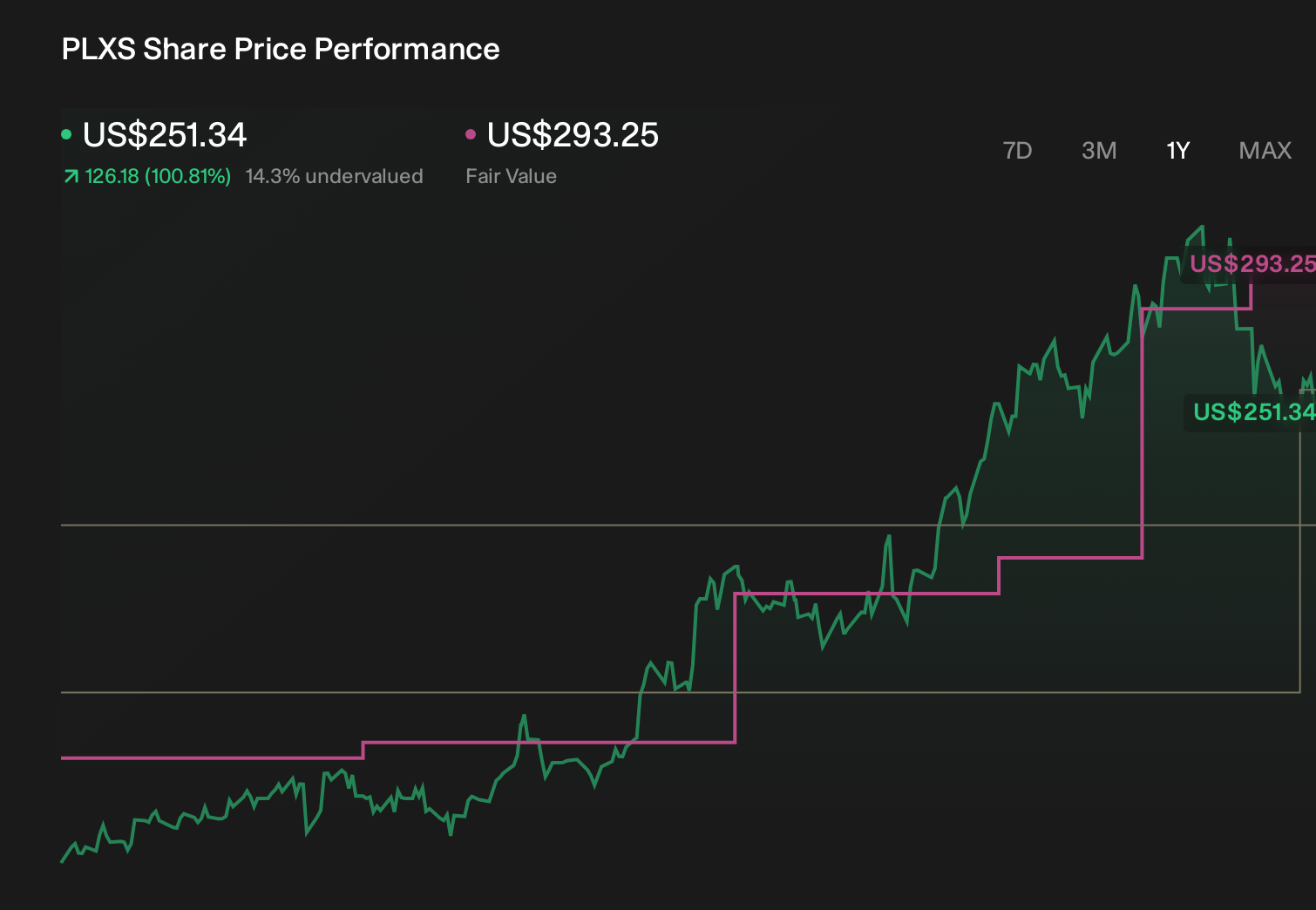

Plexus' narrative projects $6.0 billion revenue and $278.4 million earnings by 2029.

Uncover how Plexus' forecasts yield a $280.75 fair value, in line with its current price.

Exploring Other Perspectives

Compared with the baseline view, the most bullish analysts were already assuming Plexus could reach about US$5.2 billion in revenue and US$257 million in earnings, so this expanded credit line may either reinforce that optimism or prompt a rethink if concerns about rising working capital and inventory prove more pressing than expected.

Explore 2 other fair value estimates on Plexus - why the stock might be worth 45% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Plexus research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Plexus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Plexus' overall financial health at a glance.

Seeking Other Investments?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.