The Bull Case For Quanta Services (PWR) Could Change Following New Buyback, Dividend And Board Appointment

Quanta Services, Inc. PWR | 0.00 |

- Earlier this month, Quanta Services appointed Joseph Kim to its board, authorized a US$1.00 billion share repurchase program, and affirmed a quarterly dividend of US$0.11 per share payable on July 13, 2026.

- These moves combine fresh boardroom expertise in supply chain and logistics with capital returns that underscore management’s current priorities around buybacks and steady income.

- Next, we’ll examine how the new US$1.00 billion buyback authorization could influence Quanta’s existing investment narrative around power infrastructure.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Quanta Services Investment Narrative Recap

To own Quanta Services, you need to believe that long term spending on grid modernization, renewables, and AI driven power infrastructure will keep underpinning its large backlog and earnings base. The most important near term catalyst is continued execution on these complex projects, while the biggest current risk is that utility and data center capital spending slows. The appointment of Joseph Kim and the new US$1.00 billion buyback do not materially change those core drivers.

The new US$1.00 billion share repurchase program is the most relevant announcement here, because it interacts directly with Quanta’s already rich valuation and capital intensive growth plan. With the stock trading at a premium P/E versus peers and the business still investing heavily in acquisitions and power infrastructure capabilities, how aggressively management uses this authorization could influence how investors weigh upside from backlog against balance sheet and execution risks.

Yet while the capital return story is appealing, investors should also be aware of the growing risk that large, politically sensitive transmission projects could face...

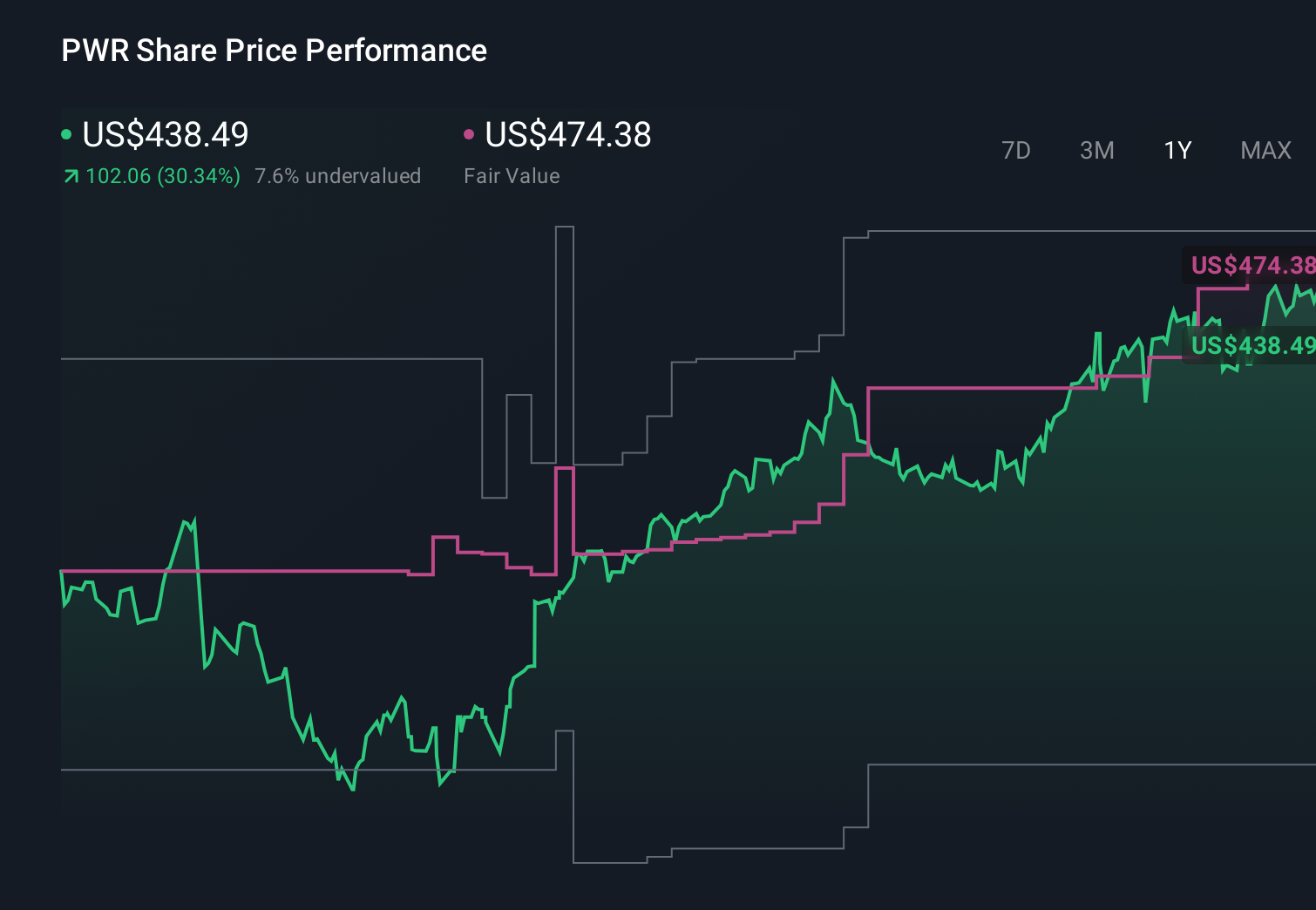

Quanta Services' narrative projects $42.8 billion revenue and $2.1 billion earnings by 2029. This requires 14.6% yearly revenue growth and about a $1.1 billion earnings increase from $1.0 billion today.

Uncover how Quanta Services' forecasts yield a $593.30 fair value, a 19% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$49.2 billion and earnings US$3.3 billion by 2029, so this fresh US$1.00 billion buyback and board appointment may either reinforce that upbeat view or prompt you to question whether integration and project risk could make those forecasts too aggressive.

Explore 5 other fair value estimates on Quanta Services - why the stock might be worth as much as $710.00!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Quanta Services research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Quanta Services research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Quanta Services' overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.