The Bull Case For Salesforce (CRM) Could Change Following Russell Exit And Guggenheim Upgrade Shift

Salesforce.com, inc. CRM | 0.00 |

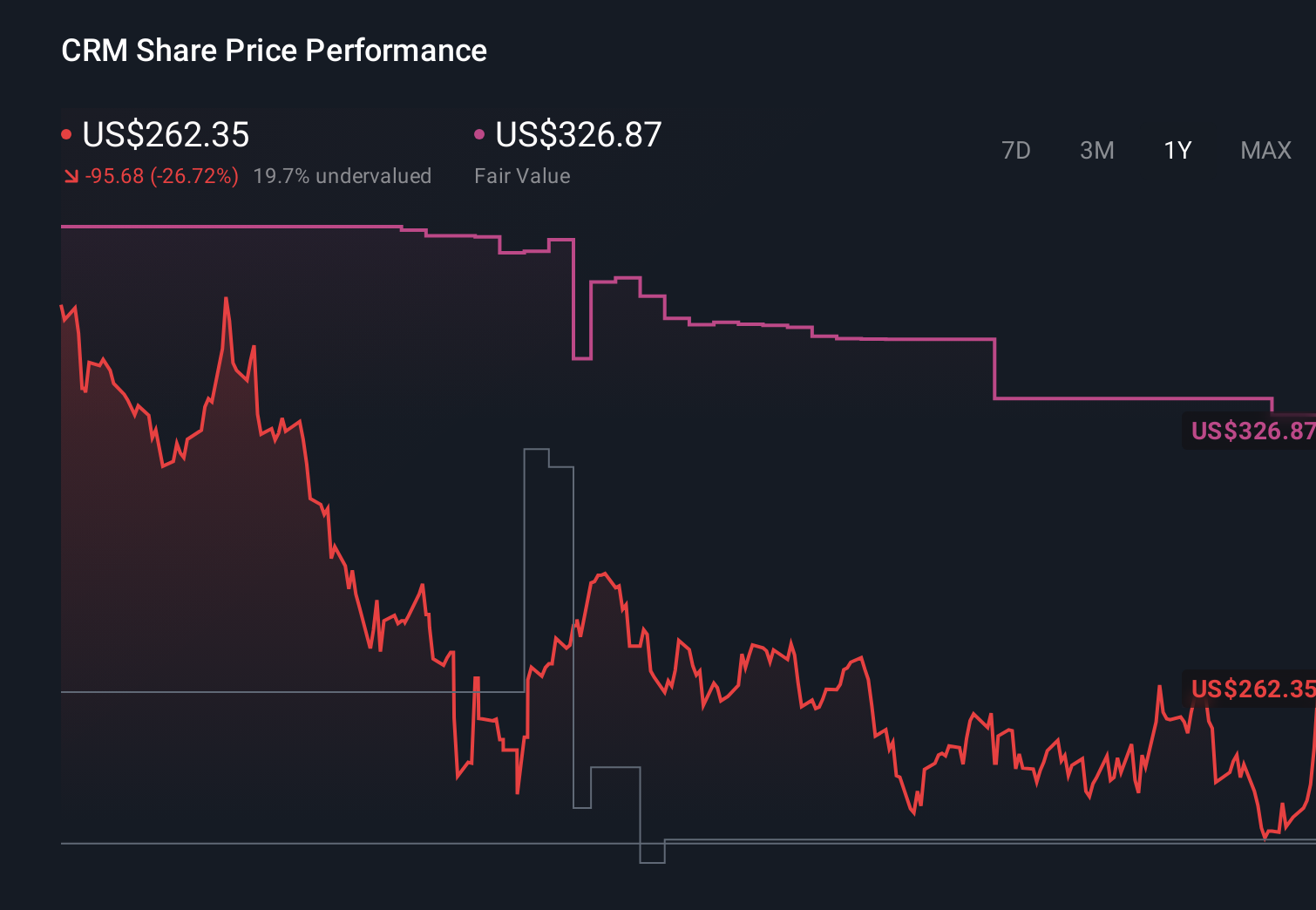

- In late June 2026, Salesforce, Inc. (NYSE: CRM) was removed from multiple Russell growth benchmarks, including the Russell Top 50, Russell Top 200 Growth, Russell 1000 Growth, Russell 3000 Growth, and Russell 3000E Growth indices.

- Around the same time, Guggenheim’s upgrade of Salesforce to Buy, framed as a valuation call amid overdone AI disruption fears and supported by strong Agentforce traction and a very large US$25.00 billion accelerated share repurchase, helped reframe sentiment on the stock’s fundamental story.

- We’ll now examine how Guggenheim’s valuation-driven upgrade amid heightened AI concerns interacts with Salesforce’s pre-existing investment narrative and outlook.

The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Salesforce Investment Narrative Recap

To own Salesforce today, you need to believe that its AI and data cloud strategy can keep lifting contract values and margins despite slower headline growth and tough competition. The biggest near term catalyst is continued adoption of Agentforce and Data Cloud across existing customers, while a key risk is that AI driven commoditization and vendor consolidation cap pricing power. Salesforce’s removal from multiple Russell growth indices is largely technical and does not materially change these fundamentals in the short term.

Against that backdrop, Guggenheim’s upgrade, framed around valuation after a steep share price pullback and backed by a US$25.00 billion accelerated repurchase, is particularly relevant. It sits alongside strong reported growth in AI and data ARR, as well as high profile Agentforce deployments such as the Visa Cash App Racing Bulls Formula 1 partnership, which showcase how Salesforce is trying to keep its platform central to customer operations and support its investment case.

Yet beneath the AI success stories, there is still a real risk that rising AI native competition could slowly chip away at Salesforce’s pricing power and long term growth potential that investors should be aware of...

Salesforce's narrative projects $56.6 billion revenue and $10.2 billion earnings by 2029. This requires 9.8% yearly revenue growth and about a $2.2 billion earnings increase from $8.0 billion today.

Uncover how Salesforce's forecasts yield a $248.24 fair value, a 49% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far more cautious picture, assuming revenue grows to about US$54.2 billion by 2029 with margins compressing, so it is worth weighing that against the risk that AI native rivals could pressure Salesforce’s pricing power and seeing how your own expectations compare.

Explore 30 other fair value estimates on Salesforce - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Salesforce research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Salesforce research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Salesforce's overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.