The Bull Case For Southwest Airlines (LUV) Could Change Following Spirit Rescue Fares And Legal Payout

Southwest Airlines Co. LUV | 0.00 |

- In late April 2026, Southwest Airlines began offering discounted fares and A-List status matches to travelers stranded by Spirit Airlines’ shutdown, while also concluding a long-running legal dispute by paying US$946,102.87 in damages to former flight attendant Charlene Carter.

- This combination of opportunistic customer outreach to Spirit passengers and the resolution of a nearly decade-long legal case could influence how investors weigh Southwest’s growth opportunities against its legal and reputational risks.

- We’ll now examine how Southwest’s outreach to displaced Spirit customers may shape its existing investment narrative around distribution, pricing, and earnings.

Find 51 companies with promising cash flow potential yet trading below their fair value.

Southwest Airlines Investment Narrative Recap

To own Southwest today, you need to believe its customer centric model, cost discipline, and new revenue initiatives can support earnings growth despite macro, fuel, and competitive pressures. The Spirit shutdown outreach looks tactically smart, but the more immediate stock driver is whether Southwest can sustain its recent earnings recovery, while the Carter case reinforces ongoing legal and reputational risk without materially changing the short term financial catalyst.

The most relevant recent update here is Southwest’s Q1 2026 earnings: revenue of US$7,249 million and net income of US$227 million, a swing from a loss a year ago. Against that backdrop, the Carter payout of US$946,102.87 and potential contempt proceedings highlight that legal and governance issues can sit alongside an improving income statement and active capital returns such as the completed 7.26% share buyback.

Yet beneath the improving results, investors should also be aware of the unresolved legal and regulatory overhang from the Carter case and wider compliance issues that could...

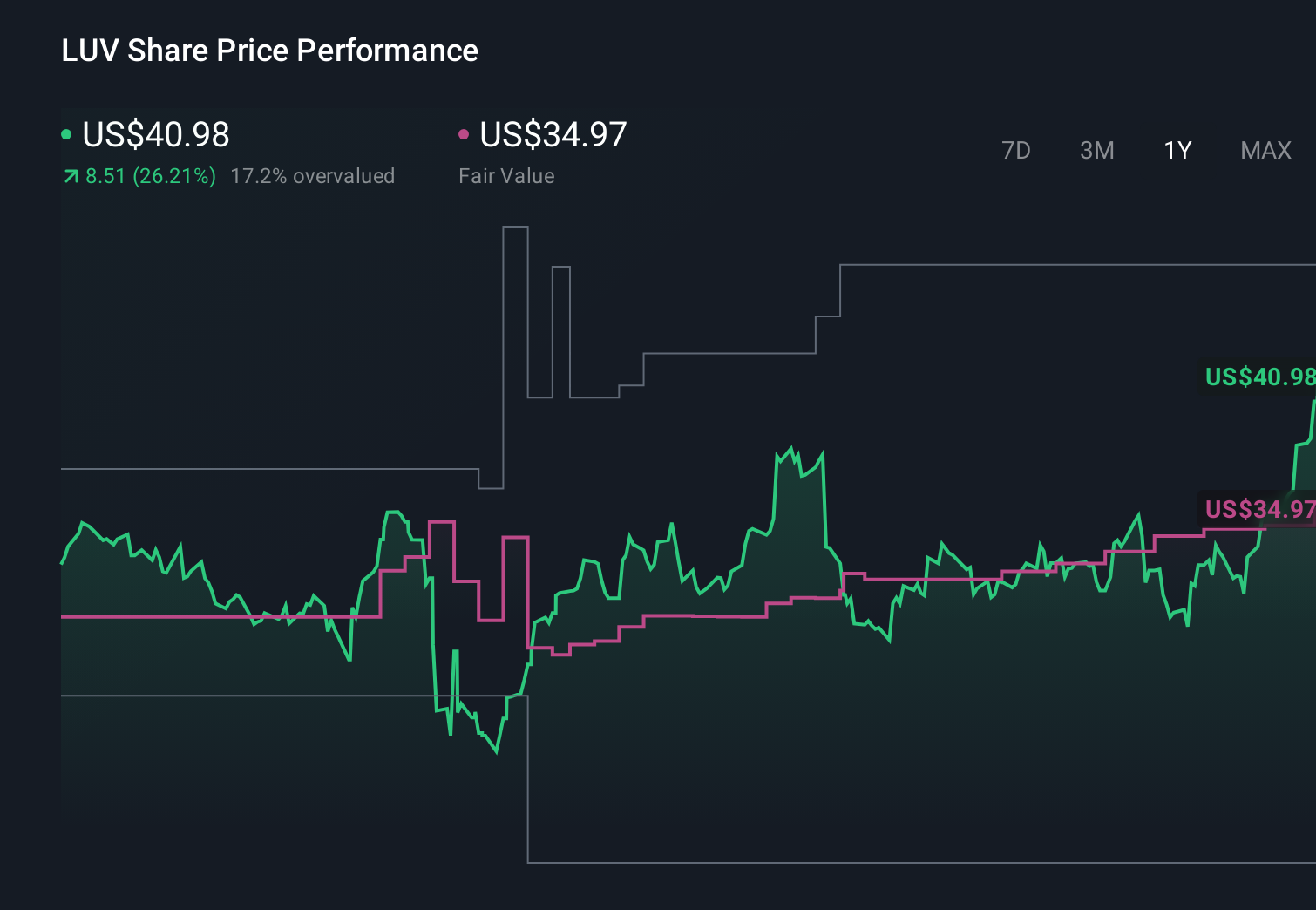

Southwest Airlines' narrative projects $34.5 billion revenue and $2.3 billion earnings by 2029. This requires 6.1% yearly revenue growth and about a $1.5 billion earnings increase from $817.0 million today.

Uncover how Southwest Airlines' forecasts yield a $45.25 fair value, a 14% upside to its current price.

Exploring Other Perspectives

While consensus focuses on new products and booking channels, the most bearish analysts were assuming only about 4 percent annual revenue growth to roughly US$31.6 billion and earnings of US$1.7 billion, which is a more cautious lens you might use to reassess the latest legal and customer experience news.

Explore 4 other fair value estimates on Southwest Airlines - why the stock might be worth just $45.25!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Southwest Airlines research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southwest Airlines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southwest Airlines' overall financial health at a glance.

No Opportunity In Southwest Airlines?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.