The Bull Case For UnitedHealth Group (UNH) Could Change Following Guidance Hike And Buyback Plan - Learn Why

UnitedHealth Group Incorporated UNH | 0.00 |

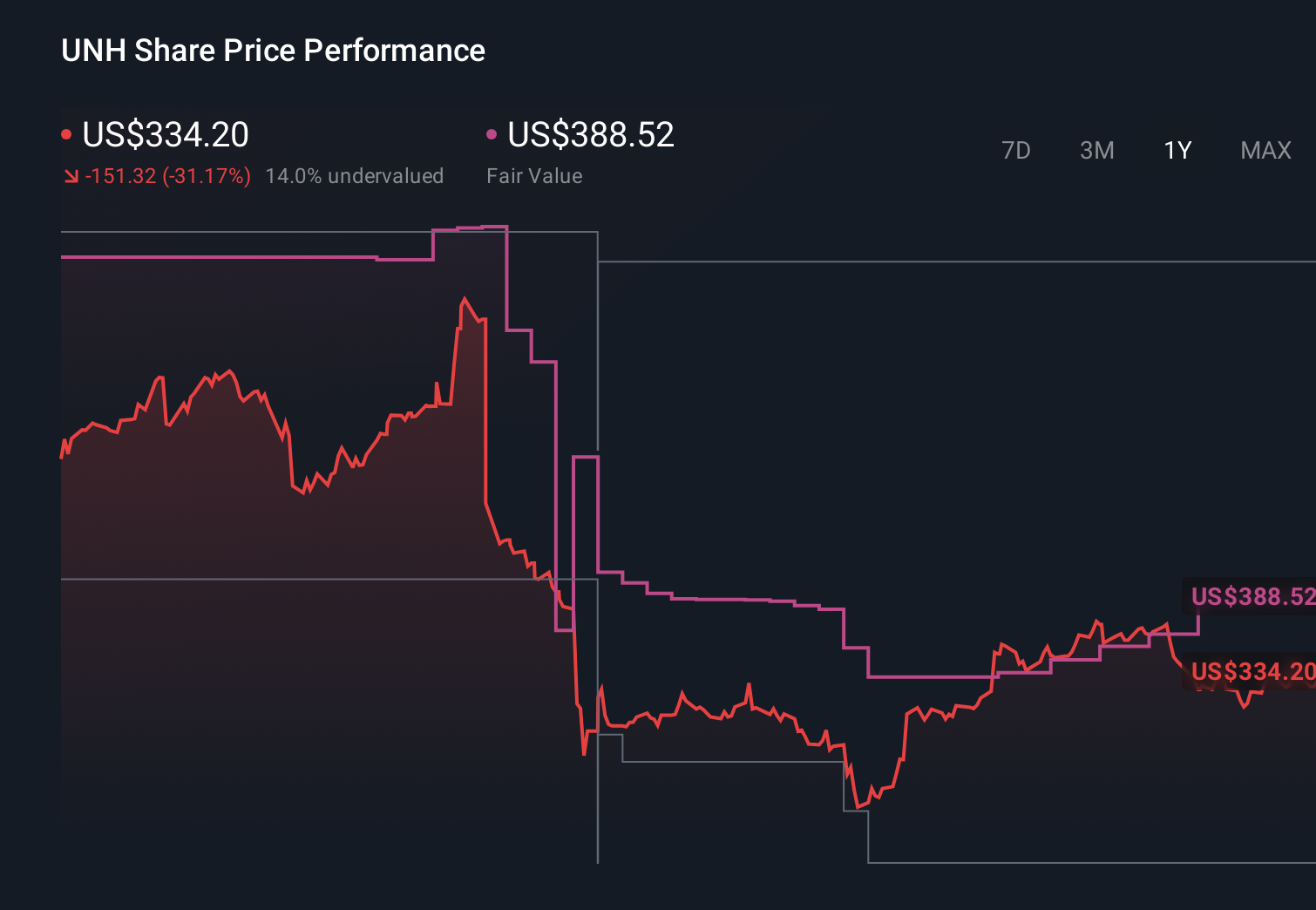

- In April 2026, UnitedHealth Group reported first-quarter 2026 results showing revenue of US$111.72 billion, net income of US$6.28 billion, and diluted EPS from continuing operations of US$6.90, modestly higher than a year earlier.

- Alongside these results, the company raised its full-year 2026 adjusted EPS outlook and announced at least US$2 billion in share buybacks, while opposing a shareholder proposal to require an independent board chair, underscoring how it is balancing capital returns, governance debates, and investment in areas such as AI.

- With UnitedHealth Group boosting its full-year earnings guidance, we’ll now examine how this update reshapes the company’s broader investment narrative.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

UnitedHealth Group Investment Narrative Recap

To own UnitedHealth Group, you have to be comfortable with a complex, highly regulated insurer that is trying to offset Medicare-related pressures with technology, Optum-driven services, and disciplined underwriting. Right now, the key short term catalyst is whether management can keep medical costs in check after a difficult 2025, while the biggest risk remains further Medicare Advantage and regulatory disruption. The latest earnings and governance news do not fundamentally change those near term priorities.

The most relevant new data point is UnitedHealth Group’s decision to raise its full year 2026 adjusted EPS outlook after reporting first quarter 2026 revenue of US$111.72 billion and net income of US$6.28 billion. That outlook lift, paired with at least US$2 billion of share buybacks, reinforces the earnings recovery catalyst many investors are watching, even as the company faces ongoing debates around board independence and wider scrutiny of its Medicare and Optum businesses.

Yet even with stronger guidance and buybacks, investors should be aware of mounting regulatory and Medicare Advantage pressures that could...

UnitedHealth Group's narrative projects $492.0 billion revenue and $21.1 billion earnings by 2029. This implies 3.0% yearly revenue growth and an earnings increase of about $9.1 billion from $12.0 billion today.

Uncover how UnitedHealth Group's forecasts yield a $386.08 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts expected earnings to reach about US$23.1 billion by 2029, versus roughly US$12.0 billion today, which is far more bullish than consensus and could look either more achievable or more stretched as new Medicare rules, DOJ scrutiny and Q1 2026 cost trends continue to develop.

Explore 88 other fair value estimates on UnitedHealth Group - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your UnitedHealth Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free UnitedHealth Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate UnitedHealth Group's overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Outshine the giants: these 18 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.