The Bull Case For W. R. Berkley (WRB) Could Change Following EPS Growth And Completed Buyback Program

W. R. Berkley Corporation WRB | 65.99 | +1.09% |

- W. R. Berkley Corporation recently reported its fourth-quarter and full-year 2025 results, showing higher revenue year on year but lower quarterly net income, alongside an update that it completed a long-running share repurchase program first announced in 2006.

- The company has bought back 161,482,852 shares over the life of the program for about US$4.33 billion, materially shrinking its share count while continuing to grow earnings per share from continuing operations in 2025 versus 2024.

- With earnings growth per share and a long-running buyback now completed, we’ll explore how these developments shape W. R. Berkley’s investment narrative.

Find 55 companies with promising cash flow potential yet trading below their fair value.

What Is W. R. Berkley's Investment Narrative?

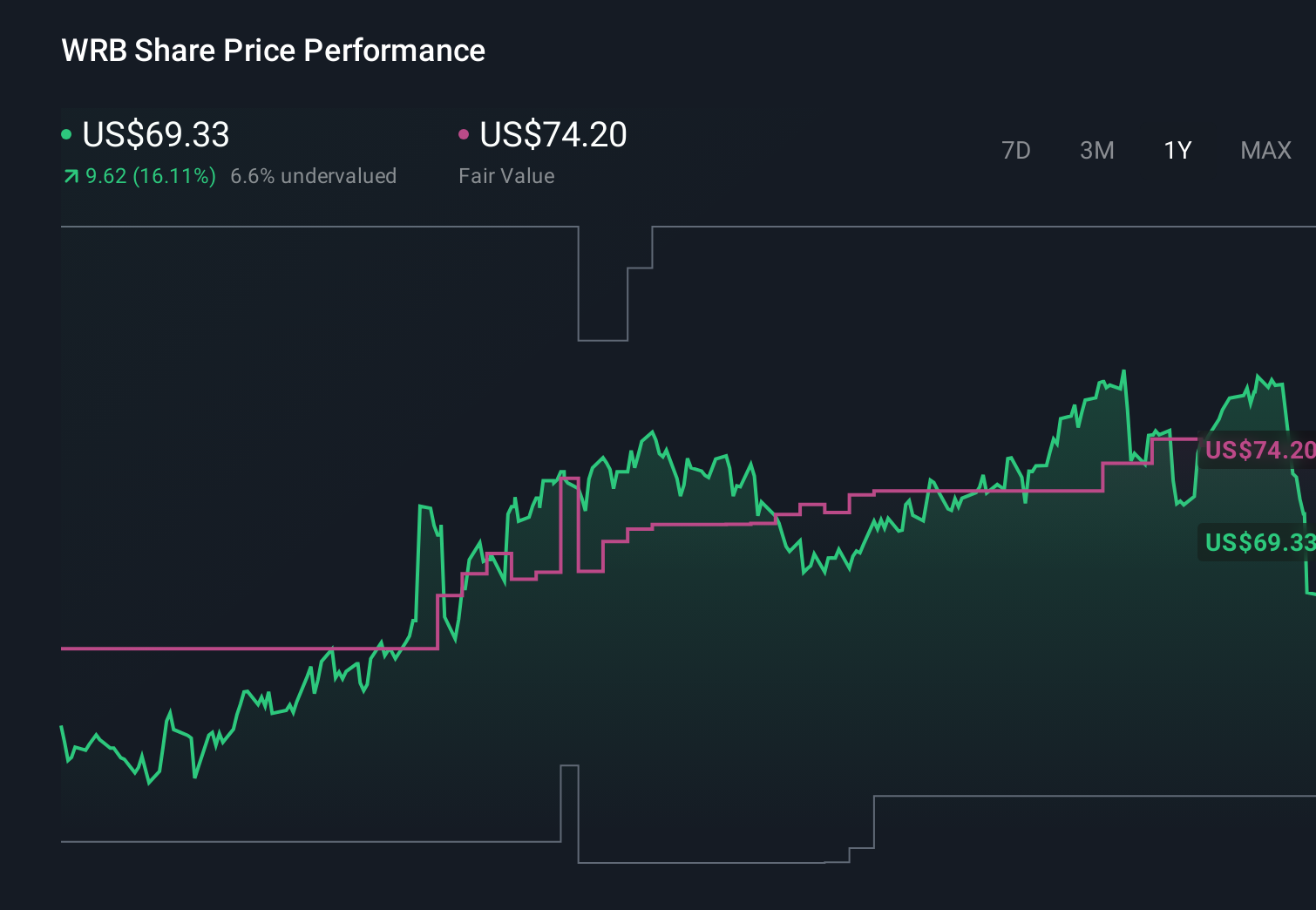

To own W. R. Berkley, you need to be comfortable with a steady, underwriting-led insurer that leans on disciplined capital returns rather than rapid expansion. The latest results reinforce that picture: full-year revenue and net income edged higher, even as fourth-quarter earnings per share dipped, reminding investors that quarterly volatility is part of the story. The completion of the long-running buyback program, alongside a recent authorization increase, underlines management’s preference for returning cash, but it also removes a long-standing technical tailwind unless a new program is actively executed. With the share price roughly in line with consensus targets after a very strong multi-year total return, the key short term catalysts remain underwriting performance and pricing conditions, while softer profit growth and a richer earnings multiple sit on the risk side of the ledger.

However, investors should be aware of the risk that slower profit growth meets a premium valuation. W. R. Berkley's shares have been on the rise but are still potentially undervalued by 43%. Find out what it's worth.Exploring Other Perspectives

Explore 3 other fair value estimates on W. R. Berkley - why the stock might be worth less than half the current price!

Build Your Own W. R. Berkley Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your W. R. Berkley research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free W. R. Berkley research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W. R. Berkley's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Capitalize on the AI infrastructure supercycle with our selection of the 33 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.