The Bull Case For Walker & Dunlop (WD) Could Change Following Alleged Chicago Loan Misrepresentation Case

Walker & Dunlop, Inc. WD | 0.00 |

- Earlier this month, Walker & Dunlop filed foreclosure lawsuits alleging that Chicago multifamily investor Chaim Bialostozky used same‑day, back‑to‑back property sales to misrepresent values and secure inflated Freddie Mac loans, later leaving the buildings to deteriorate and defaulting on at least US$7.10 million of debt and legal costs.

- The cases highlight how loan quality, counterparty behavior, and the potential use of court‑appointed receivers can affect Walker & Dunlop’s risk management and exposure on agency-backed multifamily deals.

- We’ll now examine how Walker & Dunlop’s alleged exposure to misrepresented Chicago multifamily loans may influence its broader investment narrative.

The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Walker & Dunlop Investment Narrative Recap

To own Walker & Dunlop, you need to believe in its ability to originate and service agency-backed multifamily loans while managing credit and reputational risk. The Chicago foreclosure allegations appear relatively contained in dollar terms, but they do underline that loan quality and counterparty behavior remain a key near term risk, especially when agency relationships and fee income are so central to the business model.

The recent Q1 2026 earnings release, showing US$301.33 million in revenue and positive net income, gives a more complete view of Walker & Dunlop’s fundamentals alongside this legal development. Against a backdrop of weaker recent profit margins and dependence on GSE volumes, the results help frame whether current earnings power and balance sheet flexibility are sufficient to absorb isolated credit issues without derailing the main catalysts investors are watching.

Yet, investors should be aware that Walker & Dunlop’s heavy reliance on Fannie Mae and Freddie Mac means...

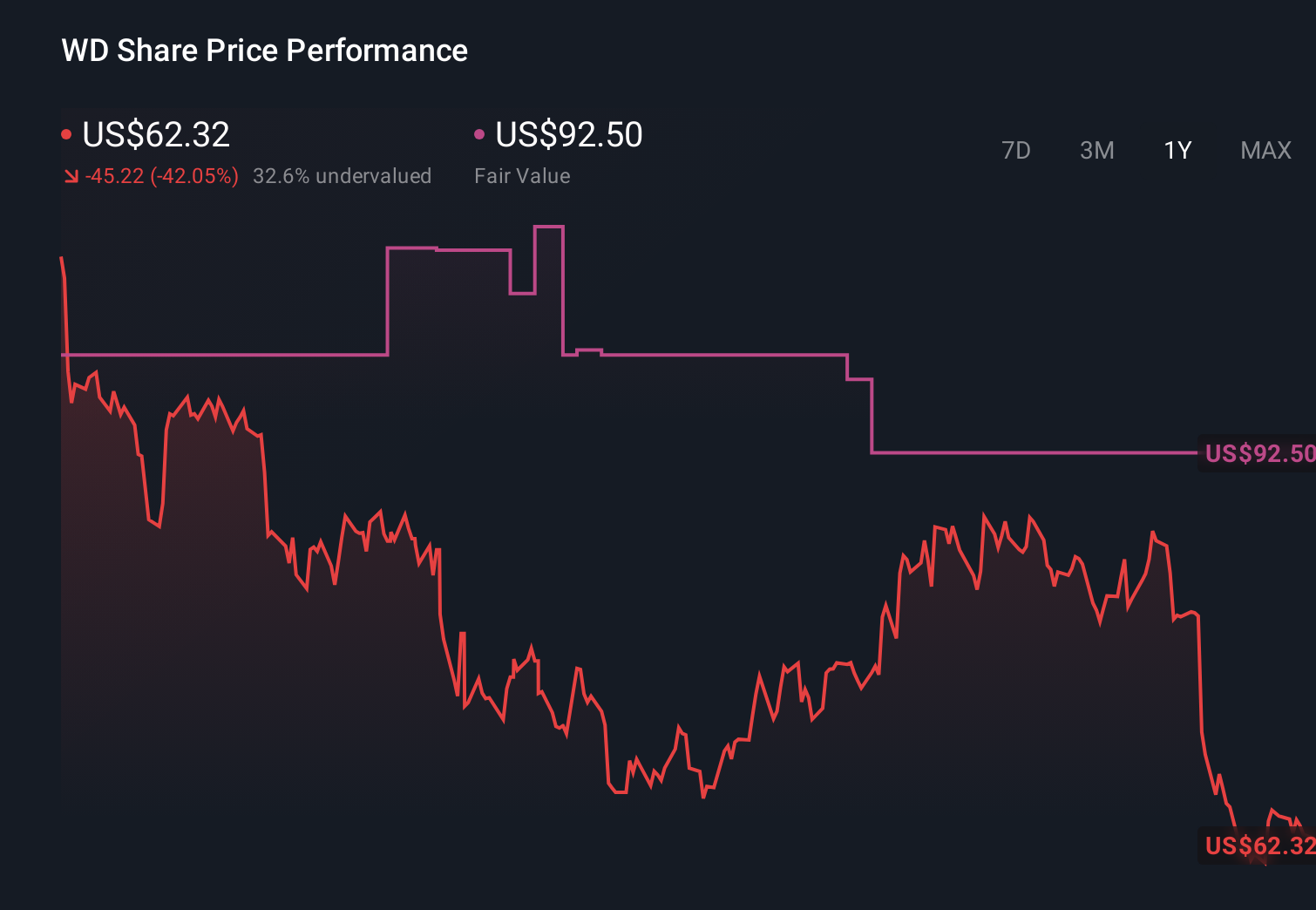

Walker & Dunlop's narrative projects $1.7 billion revenue and $214.2 million earnings by 2029. This requires 12.2% yearly revenue growth and about a $145.9 million earnings increase from $68.3 million today.

Uncover how Walker & Dunlop's forecasts yield a $68.67 fair value, a 32% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community see Walker & Dunlop’s fair value between US$31.55 and US$68.67, reflecting a wide spread of expectations. You should weigh these differing views against the company’s reliance on government sponsored entities and consider how changes to agency volumes or regulations could influence future performance before forming your own opinion.

Explore 3 other fair value estimates on Walker & Dunlop - why the stock might be worth as much as 32% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Walker & Dunlop research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Walker & Dunlop research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Walker & Dunlop's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.