The five-year loss for Janus International Group (NYSE:JBI) shareholders likely driven by its shrinking earnings

Janus International Group, Inc. JBI | 4.92 | -2.77% |

Ideally, your overall portfolio should beat the market average. But the main game is to find enough winners to more than offset the losers So we wouldn't blame long term Janus International Group, Inc. (NYSE:JBI) shareholders for doubting their decision to hold, with the stock down 46% over a half decade.

The recent uptick of 6.0% could be a positive sign of things to come, so let's take a look at historical fundamentals.

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

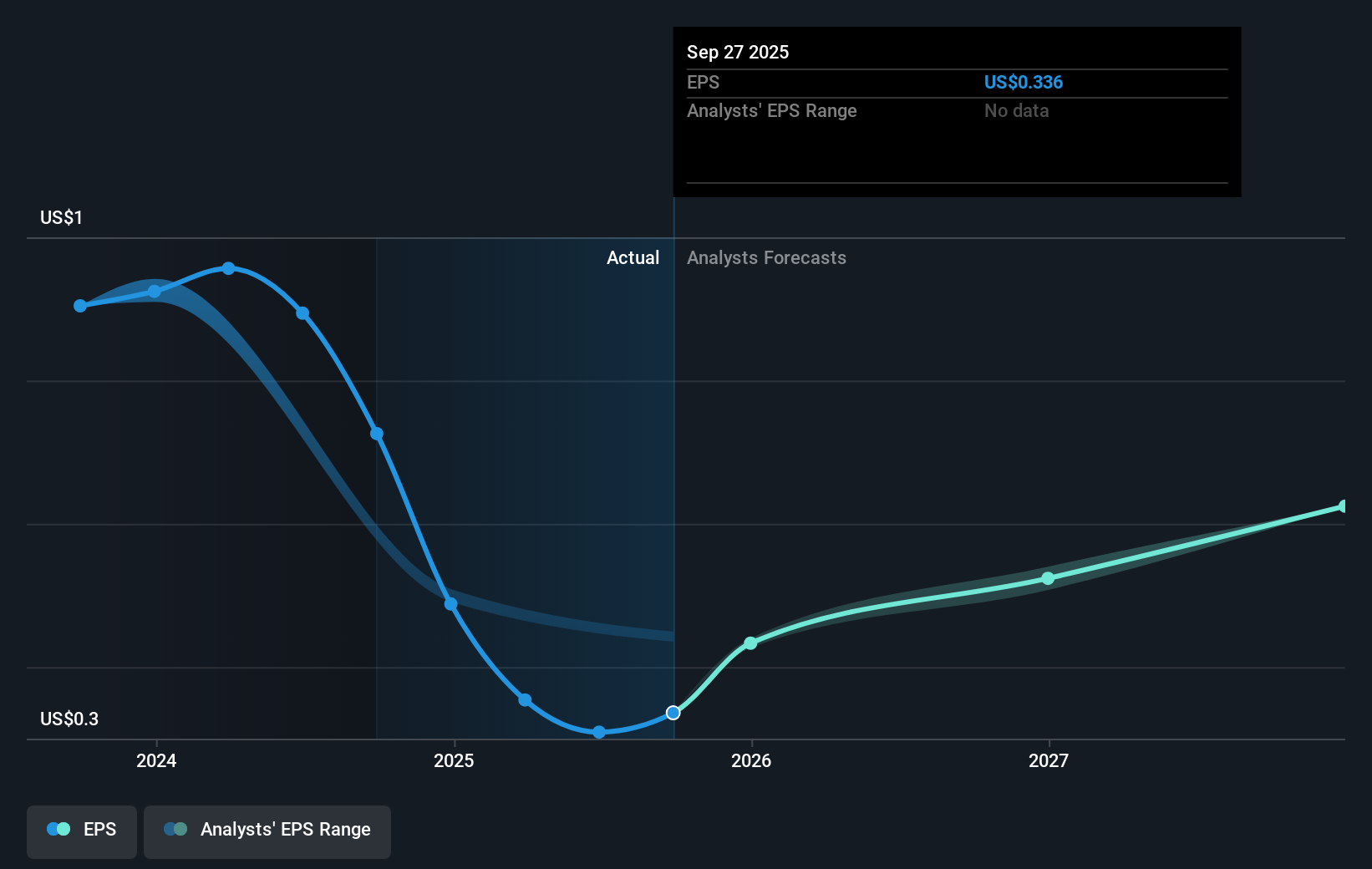

Looking back five years, both Janus International Group's share price and EPS declined; the latter at a rate of 17% per year. This fall in the EPS is worse than the 12% compound annual share price fall. So the market may previously have expected a drop, or else it expects the situation will improve.

The graphic below depicts how EPS has changed over time (unveil the exact values by clicking on the image).

A Different Perspective

While the broader market gained around 15% in the last year, Janus International Group shareholders lost 11%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Unfortunately, longer term shareholders are suffering worse, given the loss of 8% doled out over the last five years. We'd need to see some sustained improvements in the key metrics before we could muster much enthusiasm. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Take risks, for example - Janus International Group has 2 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.