The Market Waits For No One

Here's the problem with waiting for more attractive market conditions to buy stocks.

"The market waits for no one," Morgan Stanley's Mike Wilson wrote in his research note last month.

"Equity markets trade in the future where information is imperfect and uncertain," he added. "Just like they discounted much of the uncertainty we are now seeing in the headlines, they are now looking ahead to the resolution of that uncertainty and better visibility on the rolling recovery that began a year ago."

Many of the folks struggling to make sense of this year's market action continue to make the mistake of assuming that stocks are supposed to reflect what's happening today, when in reality they represent expectations for the future and the premium investors are willing to pay for that future.

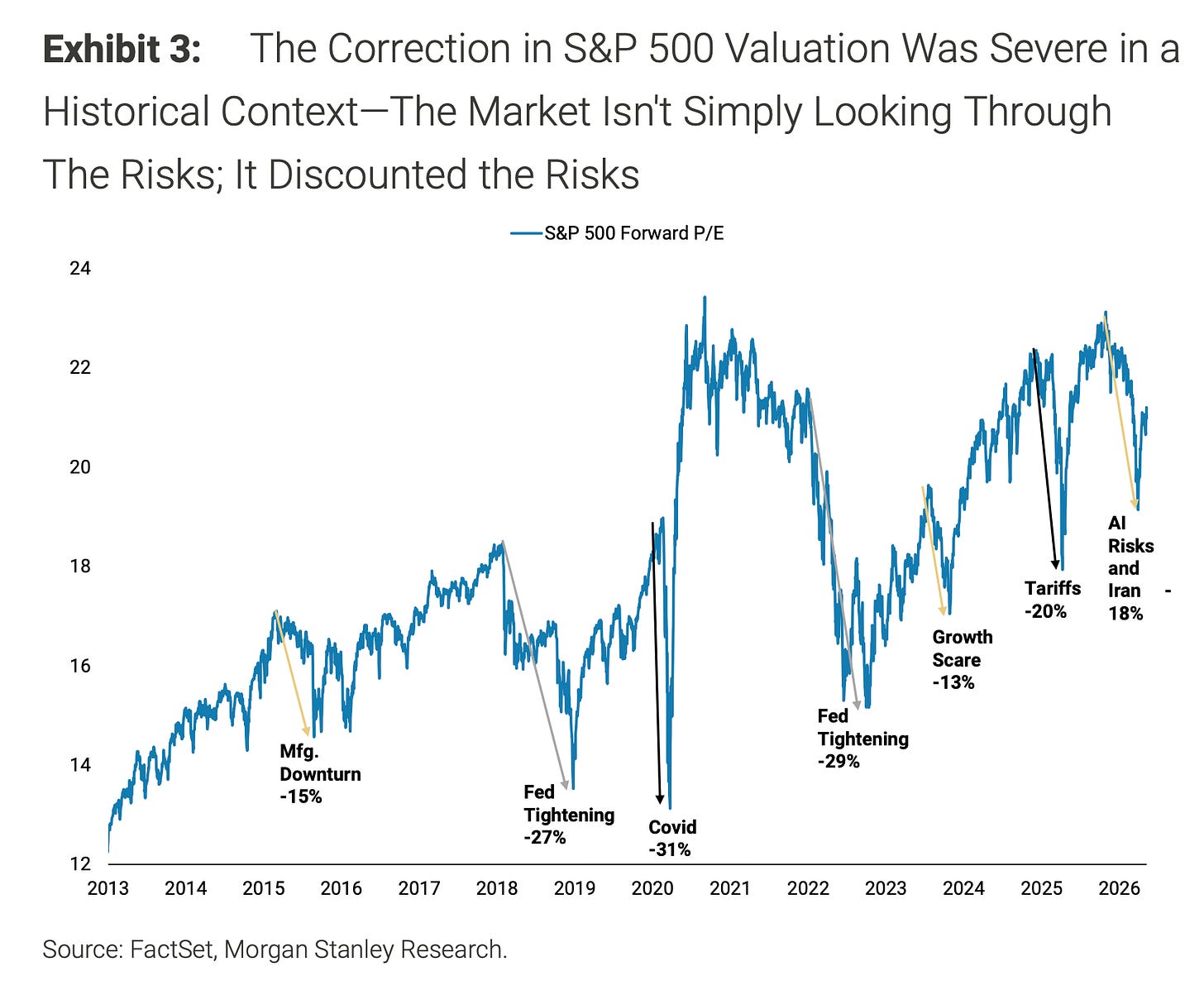

To be fair, while stock prices may not appear to reflect heightened uncertainty, stock valuations certainly do.

Stocks are cheaper, but their prices are higher

As the S&P 500 fell 9% peak-to-trough earlier this year, the forward price-to-earnings (P/E) ratio dropped 18%.

And while prices have more than recovered those losses, the P/E ratios remain off their highs, suggesting investors are paying a lower premium for future earnings.

"That's not complacency, in our view, but a market that did a substantial amount of work to price in the numerous risks that appeared over the past 6 months — Iran war/oil spike, AI disruption and private credit concerns being the most significant," Wilson wrote on Wednesday.

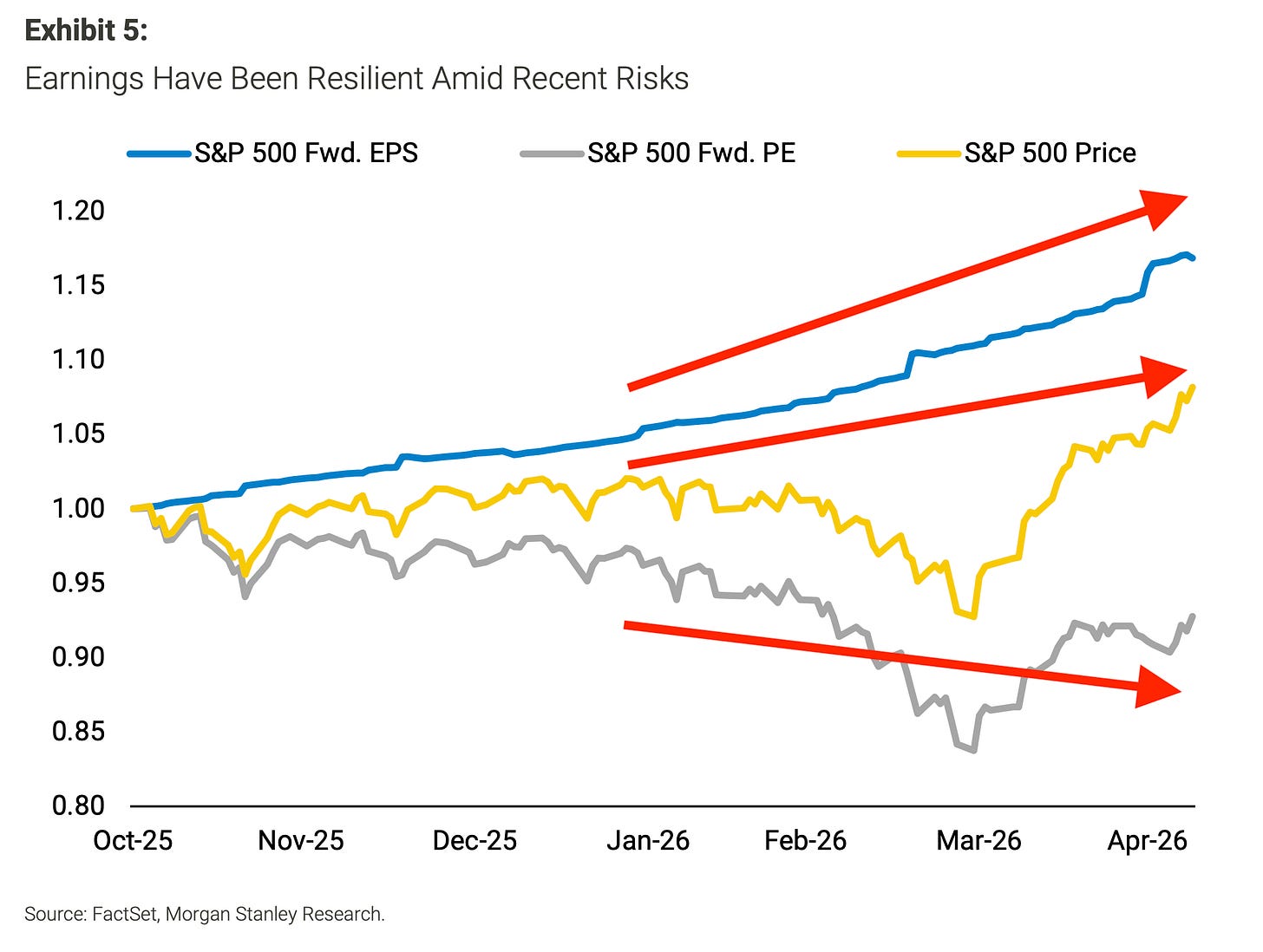

But how can stocks be higher in price but also cheaper in valuation?

It's simple: Earnings are looking up!

While we were all distracted by the recent bout of market volatility, reported earnings have been better than expected and estimates for future earnings have been going up.

When the E in P/E is rising faster than the P, it's possible to get an outcome where the P is up while the P/E is down. That's just math.

The chart below from Wilson illustrates this dynamic nicely. The blue line (earnings) has outpaced the yellow line (price), causing the grey line (valuation) to trend lower.

To Wilson's point about the market waiting for no one, this has been very true about expectations for future earnings.

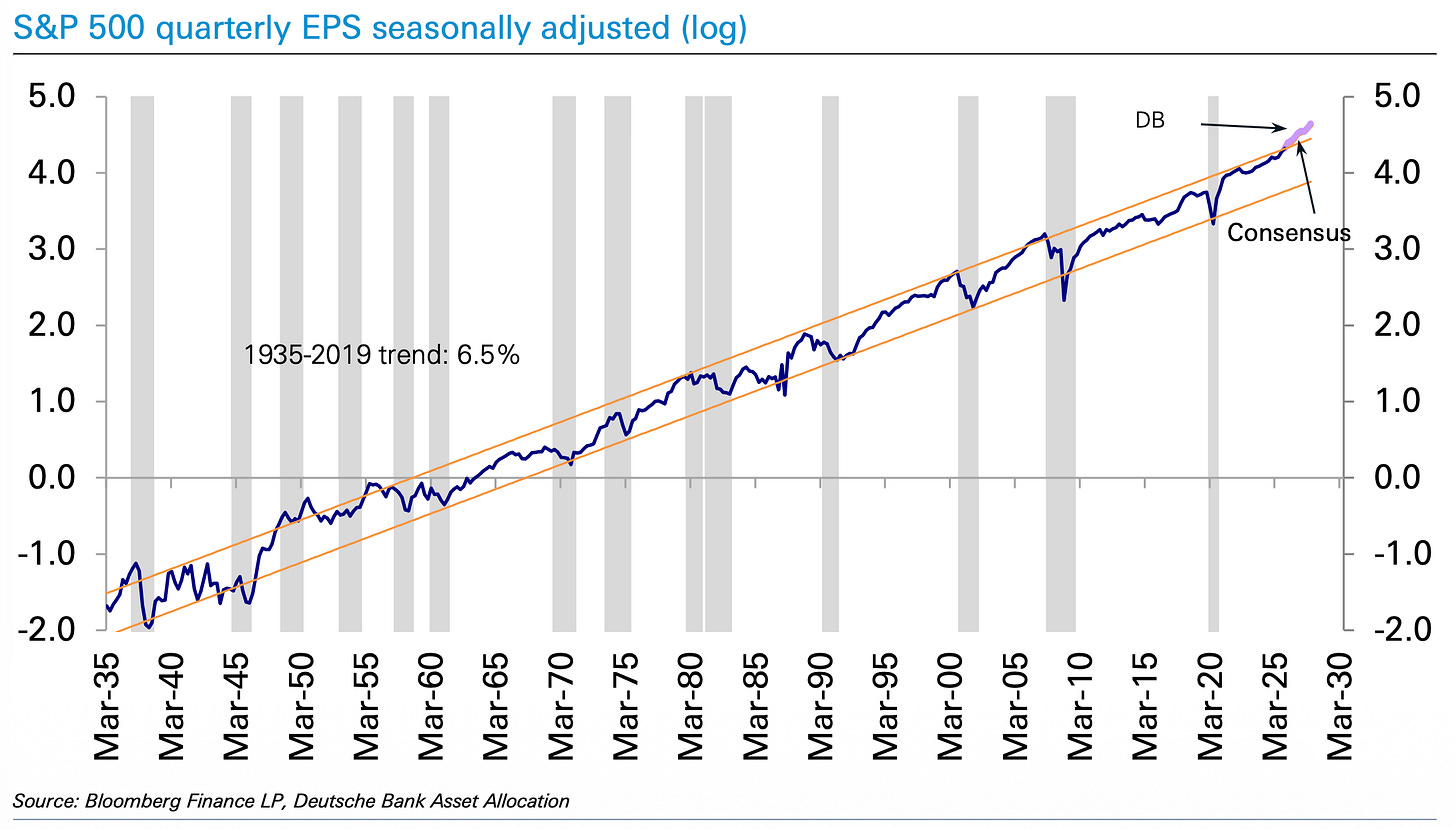

Something I've grown to appreciate with age is that time doesn't stop. And earnings tend to go up with time — at least, that's been the trend for S&P 500 earnings for at least 90 years, according to this long-term log chart from Deutsche Bank.

That means if you're waiting for cheaper valuations to buy stocks, time is your enemy. Because as time passes, earnings tend to go up. That creates the condition where you're at risk of paying up when you finally get what you think is an attractive valuation.

The big picture

You could sit on the sidelines, fretting over how valuations appear unattractive. Maybe they do eventually meet your definition of a reasonable valuation.

But remember: Publicly traded companies will never stop pursuing earnings growth. It's something that's been going on since the beginning of capitalism. (Read more about that here and here.)

So, the longer you wait for that attractive valuation to come, the greater the risk that earnings are much higher and you find that attractive valuation comes with a much higher price.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

–