THOR Industries (THO) Valuation After Earnings Beat And Cautious Full Year Guidance

Thor Industries, Inc. THO | 77.36 | -0.65% |

Why THOR Industries (THO) is back on investors’ radar

THOR Industries (THO) recently beat revenue and earnings estimates for the latest quarter, helped by strong customer interest in new RV models, yet paired that performance with more cautious full year guidance than peers.

THOR Industries’ share price has picked up momentum recently, with an 11.1% 1 month share price return and an 11.9% year to date share price return. The 1 year total shareholder return of 18.2% reflects the market’s mixed but improving view as strong quarterly beats contrast with cautious guidance in a maturing RV cycle.

If THOR’s recent rebound has you thinking about where capital could work next, it might be worth scanning auto manufacturers for other auto names showing interesting trends.

With THOR trading near US$117.95 after a strong run, and revenue and earnings outperformance set against cautious guidance and soft longer term growth, is the recent strength still offering value, or is the market already pricing in future gains?

Preferred P/E of 22.1x: Is it justified?

THOR Industries currently trades on a P/E of 22.1x, which sits just below its peer average of 22.6x, yet screens as expensive versus some other benchmarks.

The P/E multiple compares the current share price to earnings per share, so you are effectively paying 22.1 times THOR’s recent earnings for each share. For a cyclical, consumer exposed business like RVs, this matters because it reflects how much future earnings strength the market is already factoring in after a strong run in the share price.

On one hand, THOR looks slightly cheap against its direct peer average P/E of 22.6x, suggesting the market is not assigning a premium despite earnings growing 34.4% over the past year and a 1 year total shareholder return of 18.2%. On the other hand, the same 22.1x P/E is marked as expensive versus an estimated fair P/E of 17.5x and also higher than the global auto industry average of 18.6x, a gap that could close if sentiment or earnings expectations shift.

Given that contrast, the current P/E stands above what the fair ratio work suggests the market could eventually gravitate toward, and also above the broader auto group even after THOR’s strong relative share performance.

Result: Price-to-Earnings of 22.1x (OVERVALUED)

However, you still have to weigh risks, such as THOR trading above its US$111.75 price target and the potential for softer RV demand to pressure earnings expectations.

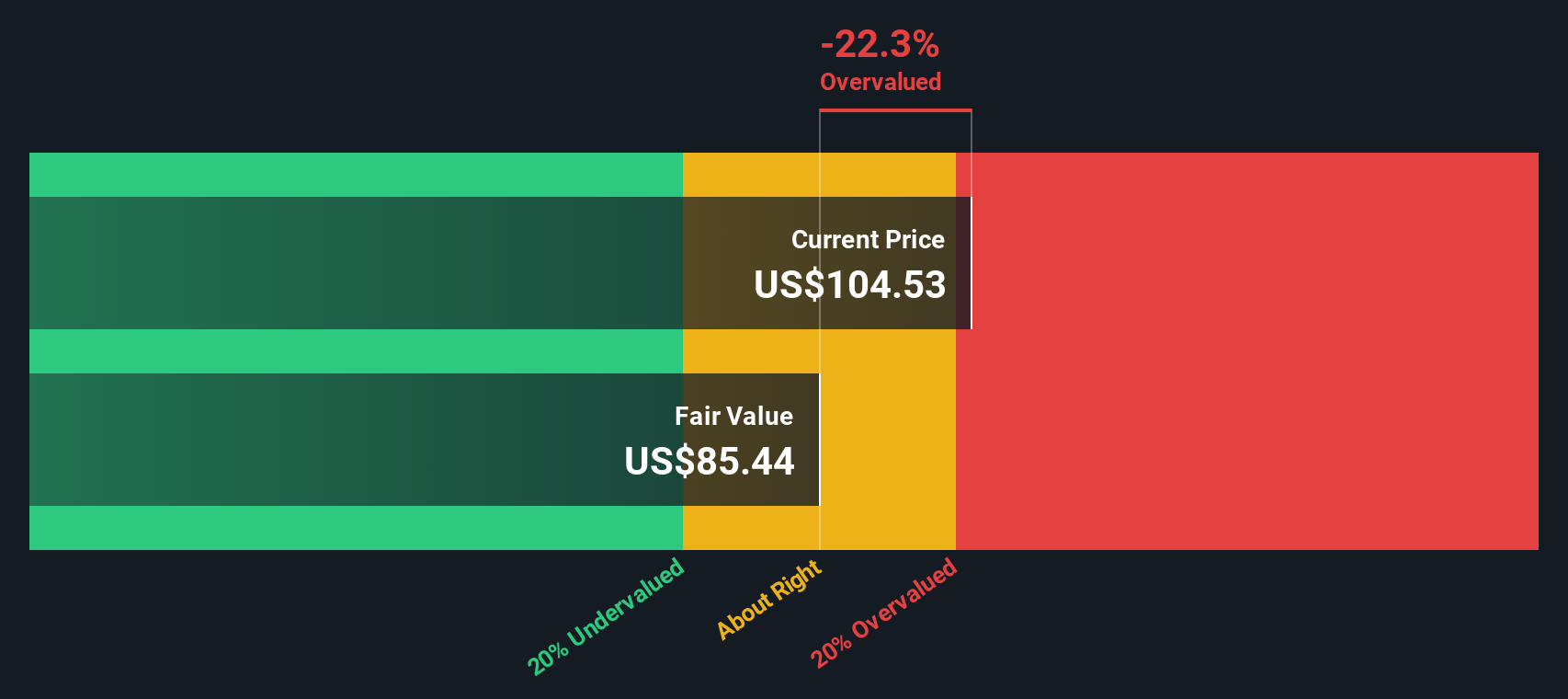

Another View: Cash Flows Point To A Different Story

Our DCF model values THOR Industries at about $109.56 per share, compared with the current $117.95 price. That suggests the recent share strength could be running ahead of what projected cash flows support, which raises a fair question: is sentiment getting ahead of fundamentals?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out THOR Industries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 880 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own THOR Industries Narrative

If this view does not quite fit how you see THOR, you can review the same numbers yourself and develop a narrative that suits your approach, then Do it your way.

A great starting point for your THOR Industries research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are weighing what to do after looking at THOR, do not stop here, there are plenty of other angles you can put to work.

- Scan for potential value by checking out these 880 undervalued stocks based on cash flows that currently screen as priced below what their cash flows might support.

- Tap into emerging tech themes by reviewing these 24 AI penny stocks that are tied to growth in artificial intelligence applications.

- Target consistent income by focusing on these 12 dividend stocks with yields > 3% that could help you build a steadier return profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.