Three Promising Middle East Stocks with Strong Potential

FOURTH MILLING 2286.SA | 0.00 |

The Middle East stock markets have recently experienced a positive shift, with Gulf bourses rising as geopolitical tensions eased following diplomatic developments between the U.S. and Iran. As indices like Dubai's benchmark index rebound from previous losses, investors are increasingly looking for opportunities in sectors such as consumer discretionary, healthcare, and technology that show resilience amid broader market fluctuations. In this environment, identifying promising stocks involves focusing on companies with strong fundamentals and growth potential that can capitalize on the region's dynamic economic landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Al Wathba National Insurance Company PJSC | 3.95% | 9.01% | -11.62% | ★★★★★★ |

| Analyst I.M.S. Investment Management Services | NA | 33.12% | 45.12% | ★★★★★★ |

| MOBI Industry | 7.46% | 5.89% | 17.98% | ★★★★★★ |

| Saudi Chemical Holding | 45.06% | 17.98% | 39.24% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | 14.04% | 16.38% | 23.83% | ★★★★★★ |

| Baazeem Trading | 11.43% | -0.08% | 1.26% | ★★★★★☆ |

| Etihad GO Telecom | 0.74% | 38.31% | 54.97% | ★★★★★☆ |

| Nofoth Food Products | 29.23% | 15.50% | 18.29% | ★★★★★☆ |

| Y.D. More Investments | 139.60% | 26.66% | 36.56% | ★★★★★☆ |

| Zahrat Al Waha For Trading | 56.06% | -0.88% | -37.72% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

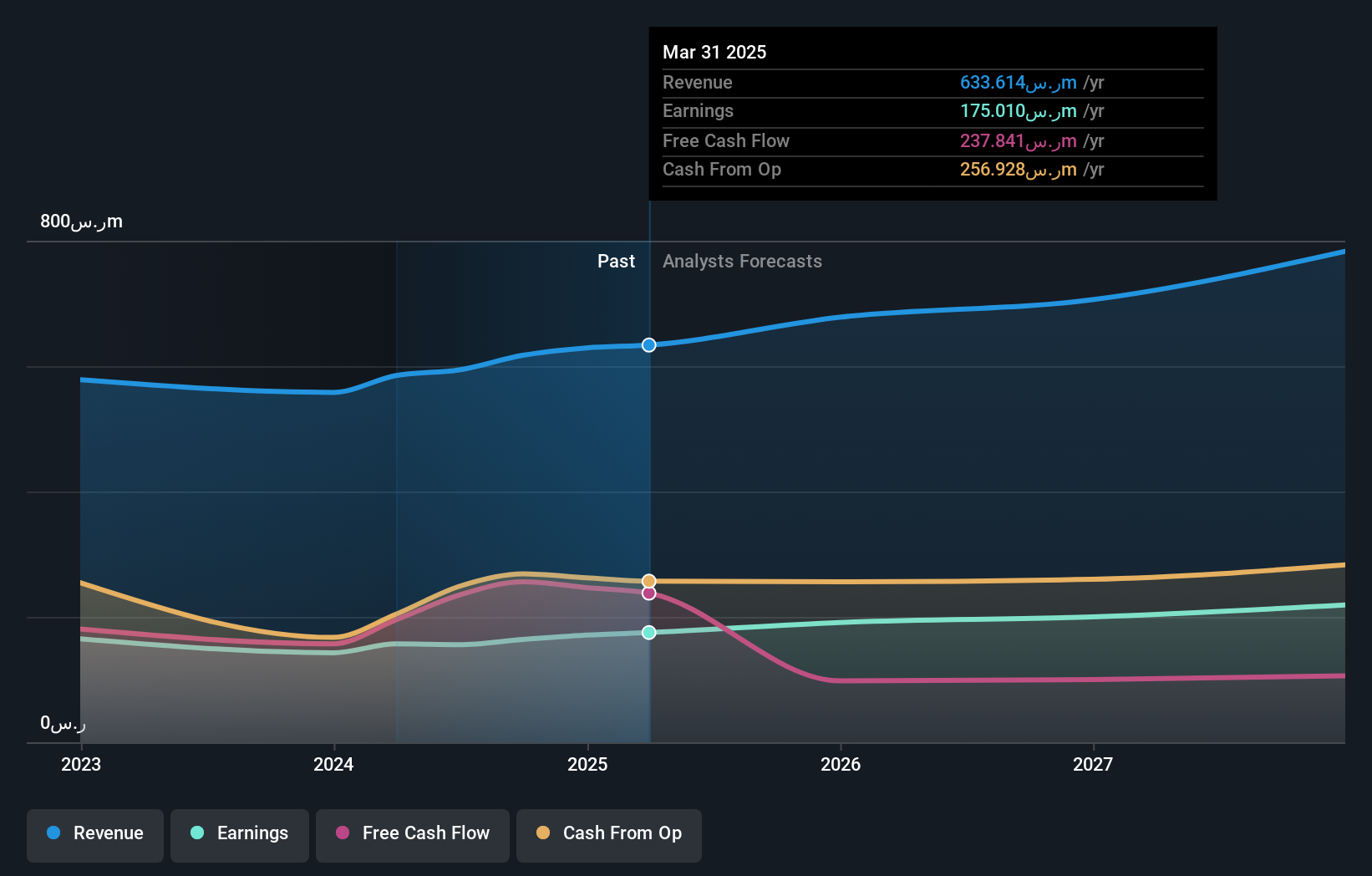

Fourth Milling (SASE:2286)

Simply Wall St Value Rating: ★★★★★☆

Overview: Fourth Milling Company operates in the production of flour, feed, bran, and wheat derivatives both within Saudi Arabia and internationally with a market capitalization of SAR2.19 billion.

Operations: Fourth Milling Company generates revenue primarily from the production of flour, feed, bran, and wheat derivatives. The company's financial performance is influenced by its cost structure and market dynamics in Saudi Arabia and international markets.

Fourth Milling, a promising player in the Middle East, has been making strides with its earnings growing by 15.1% over the past year, outpacing the food industry which saw a -16.6% shift. The company is debt-free and trades at 40.6% below its estimated fair value, indicating potential for investors seeking undervalued opportunities. Recent financials reveal sales of SAR 660 million for 2025 compared to SAR 629 million previously, with net income rising to SAR 200 million from SAR 170 million. A dividend increase to SAR 0.13 per share further underscores Fourth Milling's commitment to rewarding shareholders amidst robust performance metrics.

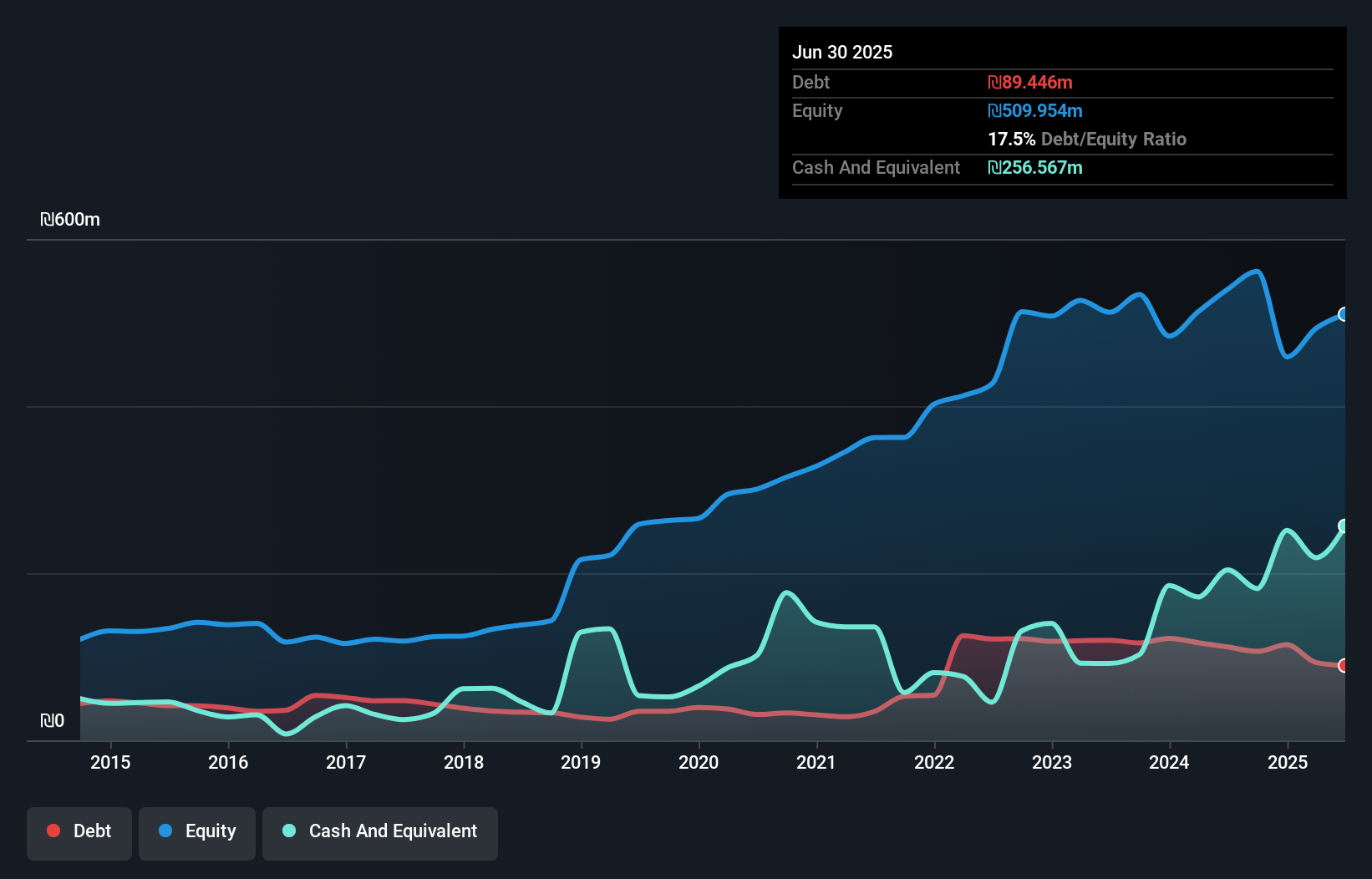

Danel (Adir Yeoshua) (TASE:DANE)

Simply Wall St Value Rating: ★★★★★☆

Overview: Danel (Adir Yeoshua) Ltd is an Israeli company specializing in human resources services, with a market capitalization of ₪2.71 billion.

Operations: Danel generates revenue primarily from its services in the human resources segment, with significant contributions from facilities for people with special needs (₪616.23 million) and nursing auxiliary services (₪1.55 billion).

Danel (Adir Yeoshua) has shown a notable turnaround with earnings surging 258% over the past year, far outpacing the Professional Services industry's 7.9% growth. The company reported net income of ILS 116.95 million for 2025, a significant leap from ILS 20.51 million in the previous year, reflecting its high-quality earnings profile and profitability. Despite an increase in debt to equity ratio from 9.3% to 14.4% over five years, Danel's interest payments are well covered by EBIT at a robust multiple of 29.6x, suggesting strong operational efficiency and financial health amidst its small cap status in the region.

Willy-Food Investments (TASE:WLFD)

Simply Wall St Value Rating: ★★★★★★

Overview: Willy-Food Investments Ltd is involved in developing, importing, marketing, and distributing a variety of food products both in Israel and internationally, with a market cap of ₪848.51 million.

Operations: Willy-Food generates revenue primarily from its dairy products and substitutes segment, which accounts for ₪213.48 million, followed by canned vegetables and fruits at ₪110.26 million. The company also earns significant income from canned fish and rice cereal and pasta segments, contributing ₪86.30 million and ₪74.58 million respectively to its revenue stream.

Willy-Food Investments, a small player in the Middle East market, has shown impressive growth with earnings up 24.8% over the past year, outpacing its industry. The company reported sales of ₪610.61 million for 2025, compared to ₪575.8 million in the previous year, while net income climbed to ₪55.06 million from ₪44.11 million a year ago. Despite a significant one-off gain of ₪33.9 million impacting recent results, Willy-Food remains debt-free and is trading at 52.6% below estimated fair value, suggesting potential for value investors looking for underappreciated opportunities in consumer retailing.

Summing It All Up

- Delve into our full catalog of 231 Middle Eastern Undiscovered Gems With Strong Fundamentals here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.