TIC Solutions: Examining the Valuation After New $277 Million Shelf Registration Filing

TIC Solutions TIC | 6.83 | +3.80% |

TIC Solutions has filed a shelf registration to offer up to $277 million of common stock. This move gives the company flexibility to raise capital and leaves investors considering what it might signal for future growth plans.

After the recent shelf registration news and Tic Solutions’ corporate name change, investors were quick to react. While the 1-day and 7-day share price returns show some short-term softness, a 1-month share price return of nearly 9% hints that sentiment has started to improve as expectations adjust. Overall, the stock's momentum has picked up in the last month, even if longer-term performance remains subdued.

If you’re watching how capital-raising plans can spark new trends, it might also be time to broaden your radar and discover fast growing stocks with high insider ownership.

With shares showing recent gains but still trading well below analyst targets, the key question is whether value remains on the table or if the market is already factoring in all of TIC Solutions’ growth potential.

Most Popular Narrative: 23.3% Undervalued

The most widely followed narrative places TIC Solutions’ fair value well above its latest closing price of $11.89. Analysts and market watchers see this gap as a potential opportunity, based on high growth expectations ahead.

“The combination with NV5 significantly broadens Acuren's end-market exposure (including faster-growth verticals such as data centers and infrastructure) and enhances cross-selling potential for turnkey, integrated inspection and engineering solutions. This is likely to drive higher future revenue and margin expansion.”

Want to know what’s driving this bold valuation? The narrative’s most optimistic assumptions are built around explosive revenue gains and dramatic margin changes over the next few years. Find out the surprising financial leaps that justify such a premium.

Result: Fair Value of $15.5 (UNDERVALUED)

However, risks remain, including the company's elevated debt load and potential integration challenges. Both of these factors could undermine the bullish growth case ahead.

Another View: SWS DCF Model Sees Overvaluation

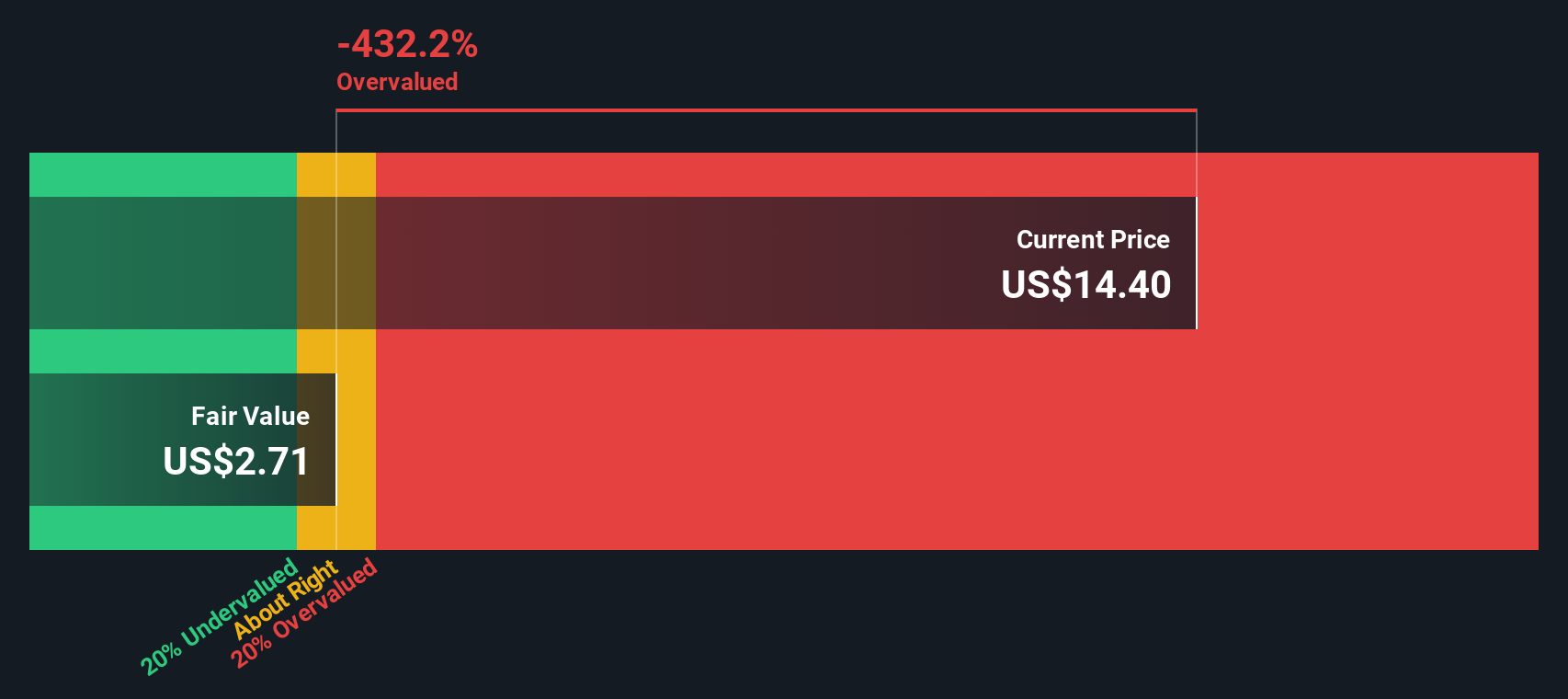

While analyst targets make TIC Solutions look undervalued, our SWS DCF model tells a different story. This approach pegs fair value at just $2.46 per share. At current prices, this points to significant overvaluation. Could the market be pricing in too much optimism for the company's future cash flows?

Build Your Own TIC Solutions Narrative

If these conclusions don’t fit your perspective, or you want to explore the numbers for yourself, you can easily craft your own view in just a few minutes. Do it your way.

A great starting point for your TIC Solutions research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t let a great opportunity pass by. The Simply Wall Street Screener uncovers stocks with strong growth, unique technology, or powerful market trends. Be sure to check out what’s next.

- Spot companies harnessing artificial intelligence for real-world disruption with these 24 AI penny stocks, setting new standards in automation and innovation.

- Shoot for steady income and long-term reliability by reviewing these 18 dividend stocks with yields > 3%, focusing on established players with attractive yields topping 3%.

- Act on deep value opportunities and stay ahead of the crowd by analyzing these 878 undervalued stocks based on cash flows, linked to robust projected cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.