Titan America (TTAM) Could Be 27% Below Fair Value Following Its Recent Rally

Titan America SA TTAM | 0.00 |

Recent Price Action and Business Snapshot

Titan America (TTAM) has drawn attention after recent price moves, with the stock last closing at $18.77. The company reports revenue of $1.67b and net income of $185.08m, entirely from United States operations.

The recent move to a $18.77 share price follows a period of strong momentum, with a 30-day share price return of 23.65% and a 1-year total shareholder return of 49.13%, reflecting shifting expectations around Titan America’s growth prospects and risk profile.

If Titan America’s recent gains have you thinking about what else might be setting up for a strong run, now could be a good time to scan 34 power grid technology and infrastructure stocks

Titan America’s recent surge and a reported 27.1% intrinsic discount raise a key question for investors: is the stock still trading below its underlying value, or has the market already priced in much of its future growth potential?

Most Popular Narrative: 34.1% Overvalued

The most followed narrative for Titan America puts fair value at $14.00 using an 8.65% discount rate, compared with the recent $18.77 close, so it frames the current price as rich and heavily dependent on execution.

The heavy reliance on large infrastructure and private nonresidential projects, including data centers and major environmental works, leaves Titan America exposed if public funding cycles slow or reshoring and reindustrialization project pipelines moderate. This would pressure volumes and revenue concentration from these categories.

Want to see what is baked into that $14.00 fair value for Titan America? The narrative leans on specific revenue growth, margin expansion and a lower future earnings multiple. Curious which of those levers does the heavy lifting in the model, and how tightly they are calibrated to current project pipelines and funding trends.

Result: Fair Value of $14.00 (OVERVALUED)

However, Titan America could outperform this cautious narrative if infrastructure and data center projects across Florida and the Mid Atlantic remain robust, supporting volumes, pricing and margins.

Another View on Titan America’s Valuation

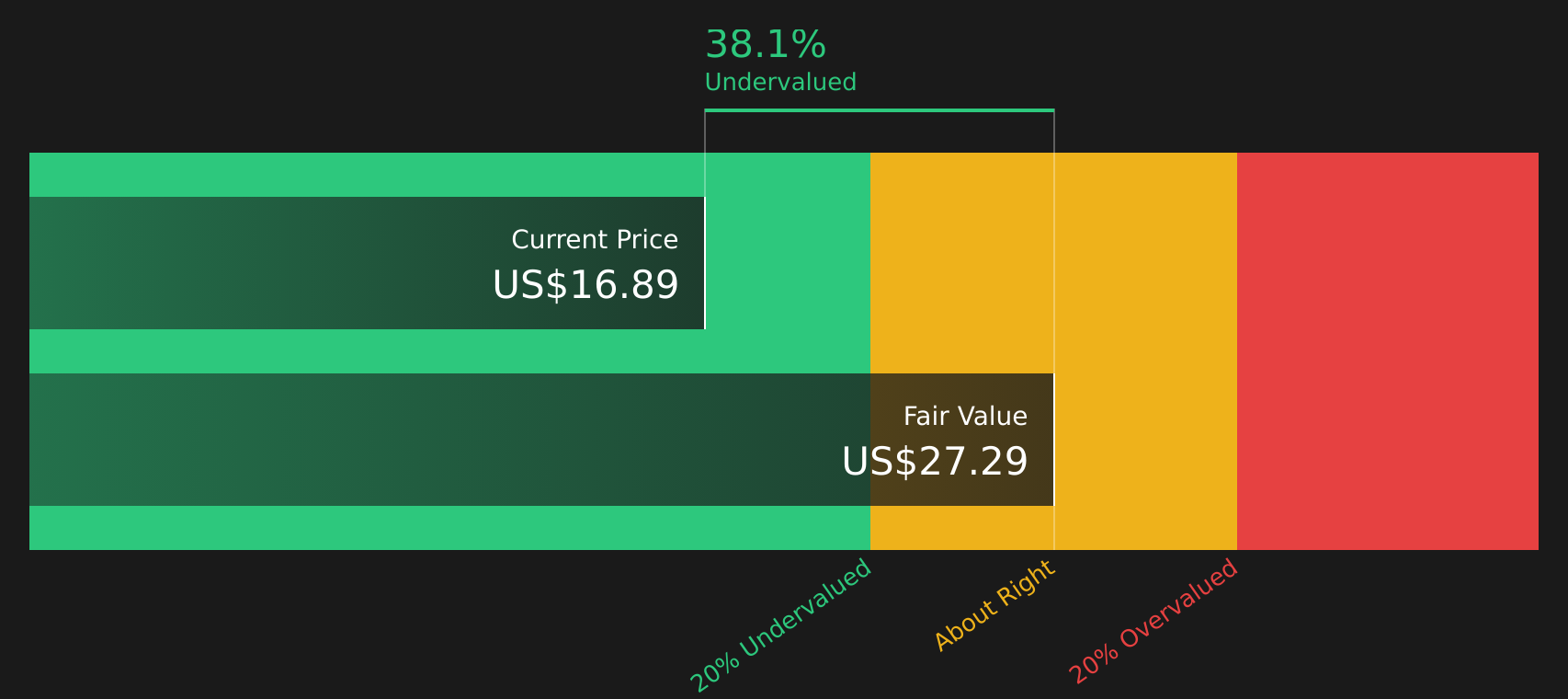

The bearish narrative argues Titan America is 34.1% overvalued at $18.77, using a fair value of $14.00. Yet our DCF model points the other way, with Titan America recently trading at $17.92 versus an estimated future cash flow value of $25.74, which implies the stock was trading at a discount.

In practical terms, the DCF view treats current cash generation and forecast growth as supportive of a higher value. The bearish fair value, by contrast, leans on more cautious assumptions about project risk, margins and future multiples. The real question for you is which set of assumptions feels closer to how Titan America will actually run its business.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Titan America for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around Titan America have you on the fence, now is a good moment to review the underlying data yourself and move quickly. To see which potential rewards investors are currently focused on, take a closer look at the 3 key rewards.

Looking for more investment ideas beyond Titan America?

If Titan America has sharpened your focus on valuation and risk, do not stop here. Use the Simply Wall St screener to surface other compelling opportunities.

- Target resilient cash generators with the 44 high quality undervalued stocks that combines quality fundamentals with pricing that may still look reasonable.

- Prioritize stability and income potential by scanning the 7 dividend fortresses for companies offering higher yields with a focus on durability.

- Reduce portfolio shocks by checking the 68 resilient stocks with low risk scores and concentrating on businesses that score well on financial and risk checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.