Top Undervalued Small Caps With Insider Action In June 2026

National Vision Holdings, Inc. EYE | 0.00 |

Over the last 7 days, the United States market has remained flat, yet it has experienced a remarkable 24% increase over the past year with earnings forecasted to grow by 19% annually. In this context of steady growth and optimistic projections, identifying small-cap stocks that are undervalued with notable insider action can offer unique opportunities for investors seeking to capitalize on potential market inefficiencies.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Kingstone Companies | 7.6x | 1.0x | 48.16% | ★★★★★☆ |

| Ferroglobe | NA | 0.6x | 24.14% | ★★★★★☆ |

| Appian | 1991.7x | 2.3x | 31.34% | ★★★★★☆ |

| Industrial Logistics Properties Trust | NA | 1.3x | 33.59% | ★★★★★☆ |

| First Bancorp | 9.5x | 3.6x | 27.15% | ★★★★☆☆ |

| Angel Oak Mortgage REIT | 13.2x | 6.0x | 24.79% | ★★★★☆☆ |

| Bank of Marin Bancorp | NA | 11.9x | 33.25% | ★★★☆☆☆ |

| Patria Investments | 25.8x | 4.7x | 4.98% | ★★★☆☆☆ |

| Shore Bancshares | 12.1x | 3.4x | 46.63% | ★★★☆☆☆ |

| National Vision Holdings | 32.0x | 0.7x | 34.05% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

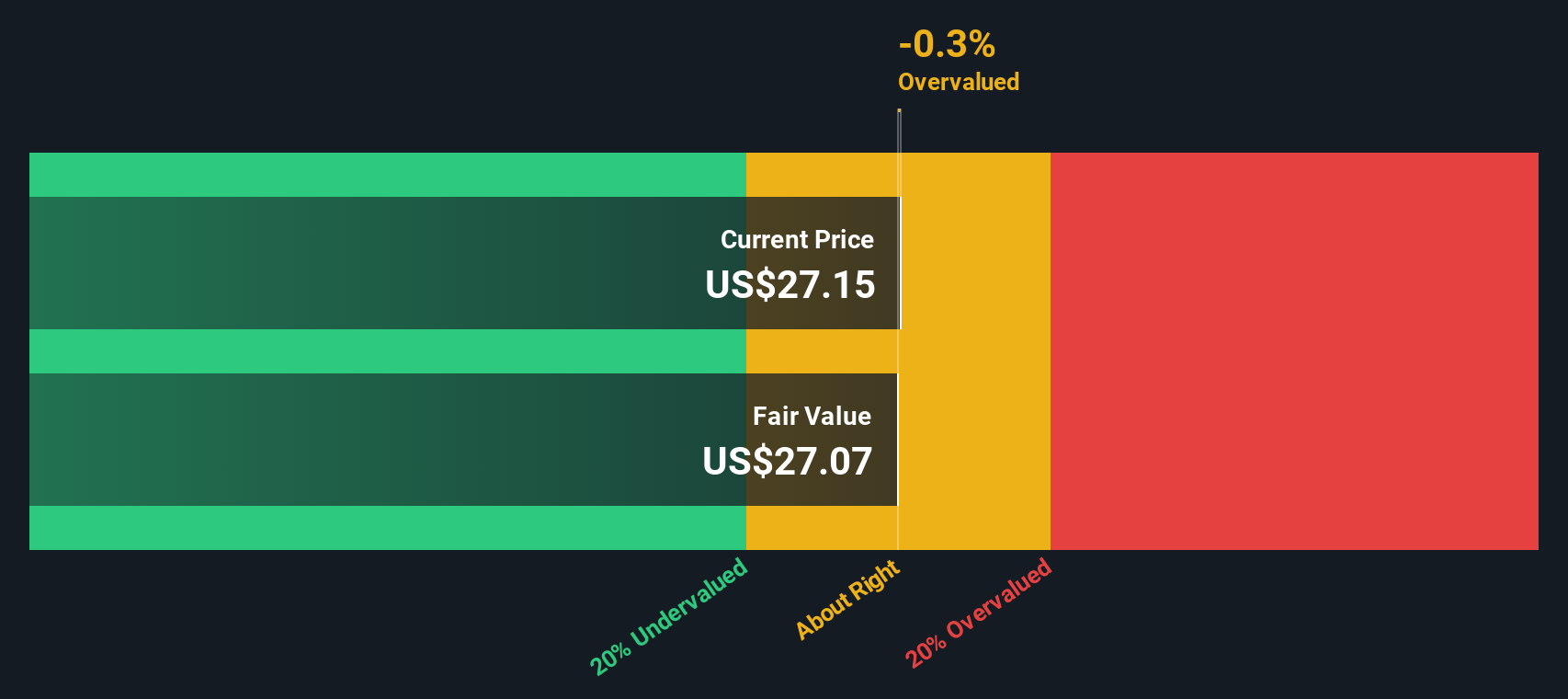

National Vision Holdings (EYE)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: National Vision Holdings operates as a retail optical company, providing affordable eye care services and products through its owned and host locations, with a market cap of approximately $2.56 billion.

Operations: The company generates revenue primarily from its Owned & Host segment, amounting to $2.00 billion, with additional contributions from the Corporate/Other segment at $19.81 million. The gross profit margin has fluctuated over time, reaching 58.77% in early 2026 after a period of variability between 2016 and 2025. Operating expenses include significant components such as General & Administrative and Sales & Marketing expenses, impacting overall profitability trends observed in net income margins across different periods.

PE: 32.0x

National Vision Holdings, a company with a focus on eye care retail, is showing signs of being undervalued in the current market. Their earnings are projected to grow by 27% annually, indicating potential for future profitability. Despite relying entirely on external borrowing for funding, insider confidence is evident as Michael Nicholson purchased 50,000 shares worth US$776,000 recently. The company reported Q1 2026 revenue of US$543 million and net income of US$31 million. With plans to open 30-35 new stores this year and projected revenues between US$2.03 billion and US$2.09 billion for fiscal year-end January 2027, there's room for growth despite funding risks.

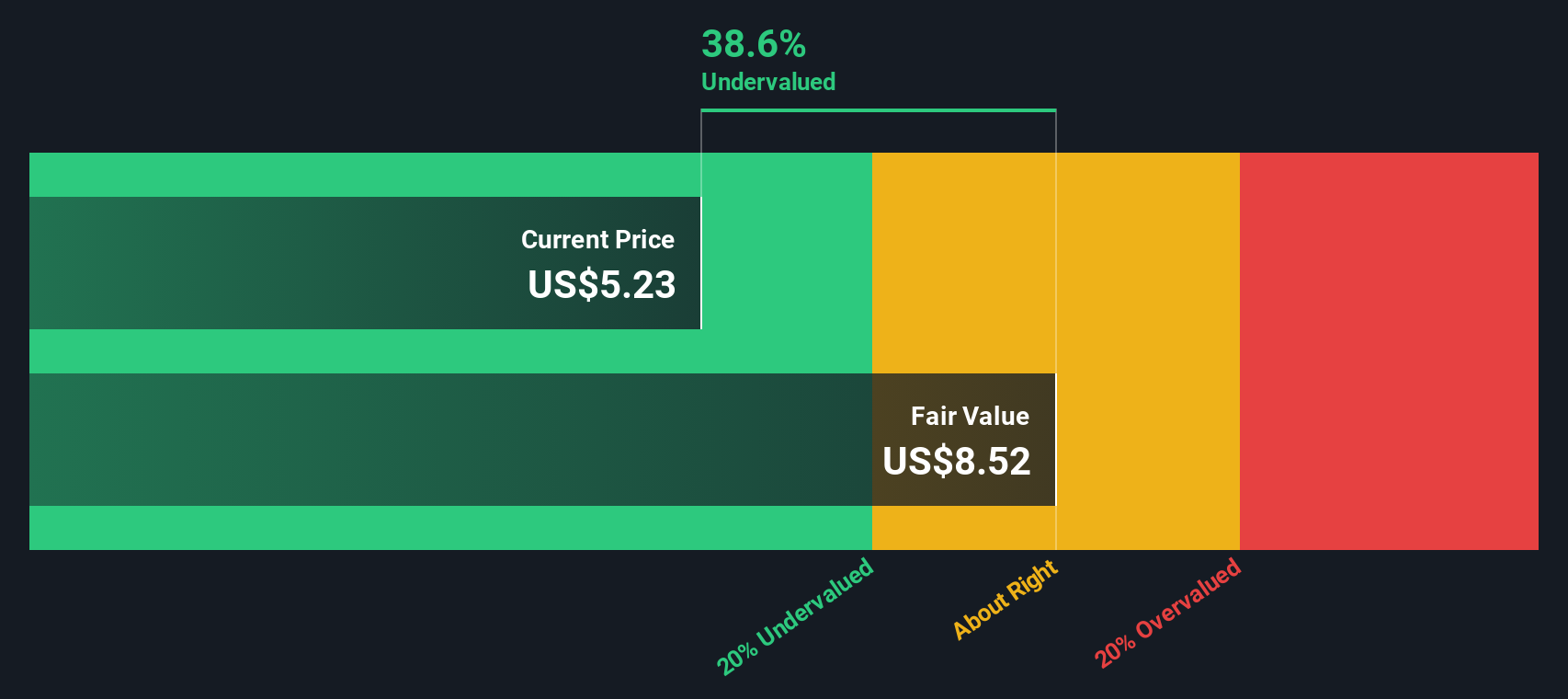

Industrial Logistics Properties Trust (ILPT)

Simply Wall St Value Rating: ★★★★★☆

Overview: Industrial Logistics Properties Trust focuses on the ownership and leasing of industrial and logistics properties, with a market capitalization of approximately $0.53 billion.

Operations: The primary revenue stream is derived from ownership and leasing of properties, generating $453.36 million. The company has experienced fluctuations in its net income margin, with a recent figure at -11.94%. Operating expenses, including depreciation and amortization, significantly impact financial results. Gross profit margin recently stood at 85.98%, indicating efficient cost management relative to revenue generation.

PE: -11.1x

Industrial Logistics Properties Trust, a small U.S. real estate investment trust, recently executed two major leases totaling 2.7 million square feet, boosting occupancy to 98%. This strategic move addresses key vacancies and enhances portfolio value. Despite reporting a net loss of US$9.43 million in Q1 2026, down from US$21.53 million the previous year, insider confidence is evident with recent share purchases by executives. The company’s reliance on external borrowing poses risks but also potential for growth through strategic asset utilization in locations like Hawaii and Indiana.

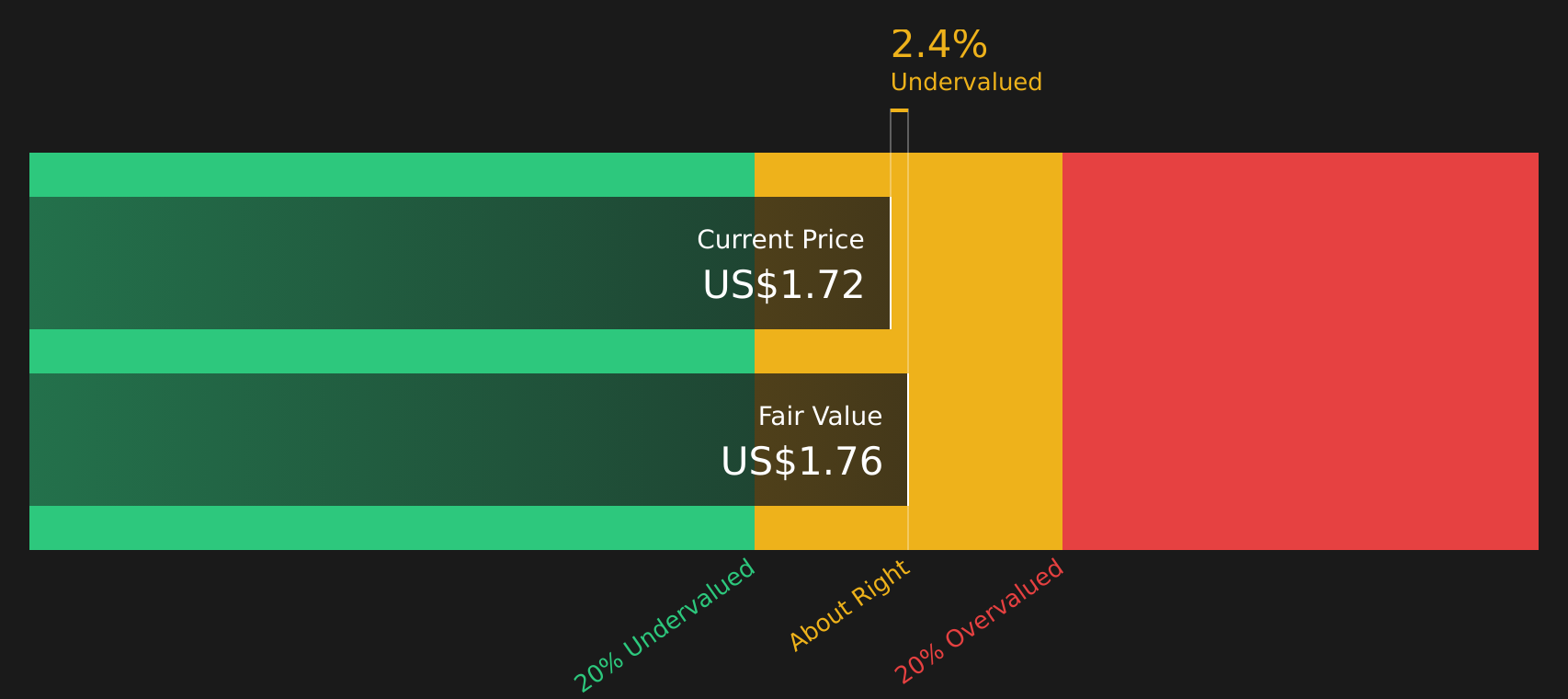

Service Properties Trust (SVC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Service Properties Trust operates primarily through its hotel and net lease segments, with a market cap of approximately $1.26 billion.

Operations: The company's revenue is derived from its hotel and net lease segments, with a significant portion coming from hotels. The gross profit margin has shown variability, reaching as high as 47.36% in Q3 2020 before declining to 30.20% by Q3 2025. Operating expenses, including depreciation and amortization, contribute significantly to the cost structure, impacting overall profitability.

PE: -4.4x

Service Properties Trust, a smaller company in the market, recently saw insider confidence with President Christopher Bilotto purchasing 100,000 shares for US$120,000. Despite reporting a net loss of US$151.18 million in Q1 2026 and experiencing shareholder dilution from a recent US$500 million equity offering, this move signals potential optimism about future prospects. The company's revenue declined to US$364.45 million compared to last year’s figures; however, its participation at the Nareit REITweek Investor Conference may attract renewed investor interest.

Taking Advantage

- Click here to access our complete index of 69 Undervalued US Small Caps With Insider Buying.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.