Top Undervalued Small Caps With Insider Buying In July 2026

Energy Recovery, Inc. ERII | 0.00 |

Over the last 7 days, the United States market has risen by 1.6% and in the past year, it has climbed an impressive 19%, with earnings forecasted to grow by 18% annually. In such a thriving environment, identifying small-cap stocks that are potentially undervalued and exhibit insider buying can be a strategic approach for investors looking to capitalize on these growth trends.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Onterris | 170.8x | 0.9x | 27.55% | ★★★★★☆ |

| Appian | 2024.0x | 2.3x | 34.31% | ★★★★★☆ |

| Industrial Logistics Properties Trust | NA | 1.3x | 37.99% | ★★★★★☆ |

| Bank of Marin Bancorp | NA | 12.9x | 27.78% | ★★★★☆☆ |

| Kingstone Companies | 9.4x | 1.3x | 35.73% | ★★★★☆☆ |

| Modiv Industrial | NA | 3.9x | 48.44% | ★★★★☆☆ |

| Angel Studios | NA | 1.7x | 21.18% | ★★★★☆☆ |

| German American Bancorp | 13.2x | 4.8x | 39.31% | ★★★☆☆☆ |

| First Bancorp | 10.9x | 4.1x | 18.17% | ★★★☆☆☆ |

| Patria Investments | 24.8x | 4.5x | 7.76% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

Hudson Technologies (HDSN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Hudson Technologies is a company that specializes in refrigerant services and solutions, with operations focusing on the wholesale of miscellaneous products, and has a market capitalization of approximately $0.5 billion.

Operations: The company's revenue is driven by its wholesale segment, with recent figures showing $251.42 million. The cost of goods sold (COGS) has been significant, impacting the gross profit margin which was 24.61% in the latest period. Operating expenses also play a substantial role in financial outcomes, influencing net income margins over time.

PE: 17.7x

Hudson Technologies, a smaller company in the U.S., shows potential as an undervalued investment. Recently, insider confidence was demonstrated through share purchases. The company maintains a bridge contract with the U.S. Defense Logistics Agency until November 2026, ensuring service continuity despite a bid protest on its 2025 award. First-quarter sales increased to US$60 million from US$55 million last year, although net income fell to US$0.33 million from US$2.76 million previously. Hudson's strategic buyback of 416,480 shares for $2.49 million reflects management's belief in its long-term value proposition amidst evolving market dynamics and firming HFC prices expected to boost second-quarter revenue between $73-76 million.

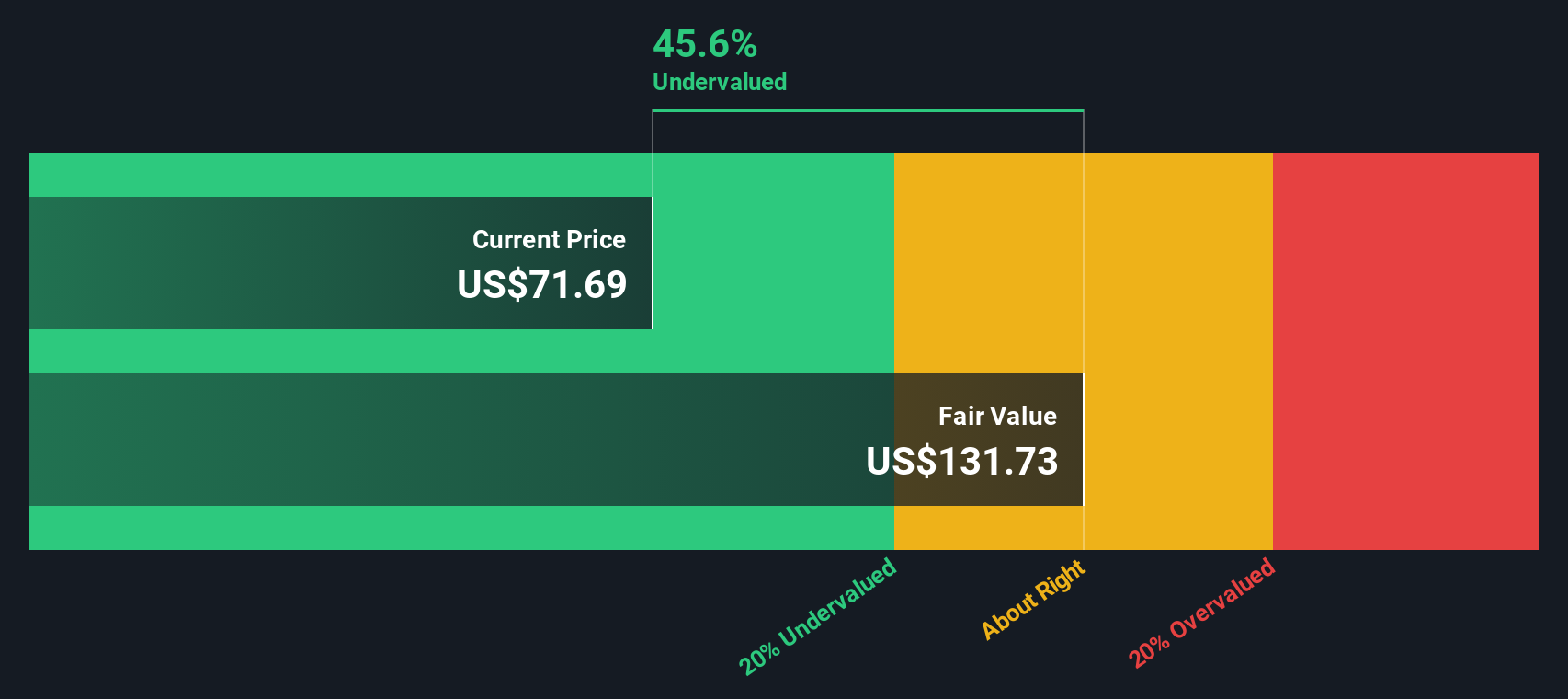

Energy Recovery (ERII)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Energy Recovery specializes in designing and manufacturing energy recovery devices for industrial fluid flow applications, with a market cap of approximately $1.57 billion.

Operations: The company generates revenue primarily from its Segment Adjustment, with a minor contribution from Emerging Technologies. Over recent periods, the gross profit margin has shown variability, reaching 64.27% in early 2026. Operating expenses are significant and include costs for sales & marketing and R&D, impacting net income margins which have fluctuated over time.

PE: 22.1x

Energy Recovery, a US company, is gaining traction with recent additions to multiple Russell Value Indexes as of June 27, 2026. The firm reported Q1 sales of US$9.71 million but faced a net loss of US$12.25 million and a goodwill impairment loss of US$1.66 million in the same period. Insider confidence is evident from share repurchases totaling 960,303 shares for US$10.66 million by March 31, 2026. Recent contracts in India for energy-efficient wastewater projects highlight their innovative edge in industrial water treatment solutions amidst leadership changes with Alex Buehler stepping in as interim CEO on May 28, 2026.

Tompkins Financial (TMP)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Tompkins Financial is a diversified financial services company offering banking and wealth management services, with a market cap of approximately $1.01 billion.

Operations: Tompkins Financial generates revenue primarily through its banking and wealth management services, with the banking segment contributing significantly more. The company has consistently reported a gross profit margin of 100%, indicating that all reported revenues translate directly into gross profit. Operating expenses are a major cost component, with general and administrative expenses being the largest contributor within this category. Net income margins have varied over time, reaching as high as 37.02% in certain periods but also experiencing lower margins in others.

PE: 8.1x

Tompkins Financial, a smaller player in the financial sector, recently reported strong first-quarter earnings with net income rising to US$26.07 million from US$19.68 million last year, despite being dropped from the Russell 2000 Dynamic Index in June 2026. The company repurchased 46,070 shares for US$3.46 million by March 31, indicating strategic confidence amidst forecasted earnings declines of 20.2% annually over the next three years. With a stable dividend of US$0.67 per share declared for May, it maintains shareholder interest while navigating industry challenges and leadership changes like Phillip M. Quintana's appointment as Executive Vice President in April 2026.

Taking Advantage

- Click here to access our complete index of 59 Undervalued US Small Caps With Insider Buying.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.