TransUnion (TRU) Following Mixed Results Has Its Valuation Back In Focus

TransUnion TRU | 0.00 |

Why TransUnion Stock Is Back In Focus After Mixed Quarterly Results

TransUnion (TRU) is in the spotlight after its latest quarterly report, where revenue surpassed expectations but guidance pointed to softer earnings next quarter. The update highlights both solid data demand and ongoing regulatory and cybersecurity headwinds.

TransUnion's latest update appears to have shifted sentiment in the short term, with the stock posting a 7 day share price return of 9.20% and a 30 day share price return of 11.49%. However, the 1 year total shareholder return is down 14.52%, which points to improving near term momentum after a weaker longer term experience for holders.

If earnings news has you reassessing opportunities in data and technology, it may be worth broadening your watchlist with 19 top founder-led companies

The recent jump in TransUnion shares could signal that investors are reassessing the strength of its data business rather than just reacting to headlines. The next step is to evaluate whether the current valuation reflects that shift in sentiment.

Most Popular Narrative: 12.6% Undervalued

TransUnion's most followed valuation narrative pegs fair value at $90.10 per share, above the last close of $78.78, which raises clear questions about what is driving that gap.

Strategic innovation investments, including AI, machine learning, and the roll-out of the global cloud-native OneTru platform, are driving efficiency, faster product launches, better cross-sell opportunities, and improved customer retention, positioning TransUnion to grow earnings with higher operating leverage and net margins as technology transformation costs subside post-2025.

Read the complete narrative. Read the complete narrative.

Want to see why this narrative still supports a higher price tag for TransUnion? The entire framework hangs on compounding revenue, firmer margins, and a richer earnings multiple working together.

The narrative blends analyst expectations for steadier earnings growth, modest margin expansion and a higher future P/E into a discounted cash flow style view, using an 8.18% discount rate to translate those forecasts back to today's terms. At its core, the valuation assumes TransUnion can grow its $4.7b revenue base, lift profitability from current levels and justify a future earnings multiple that sits above the current industry benchmark, while also factoring in planned share count reductions.

Result: Fair Value of $90.10 (UNDERVALUED)

However, the TransUnion narrative still depends on data privacy and cybersecurity risks remaining contained, as well as competition not driving deeper price or margin pressure over time.

Another View On TransUnion’s Valuation

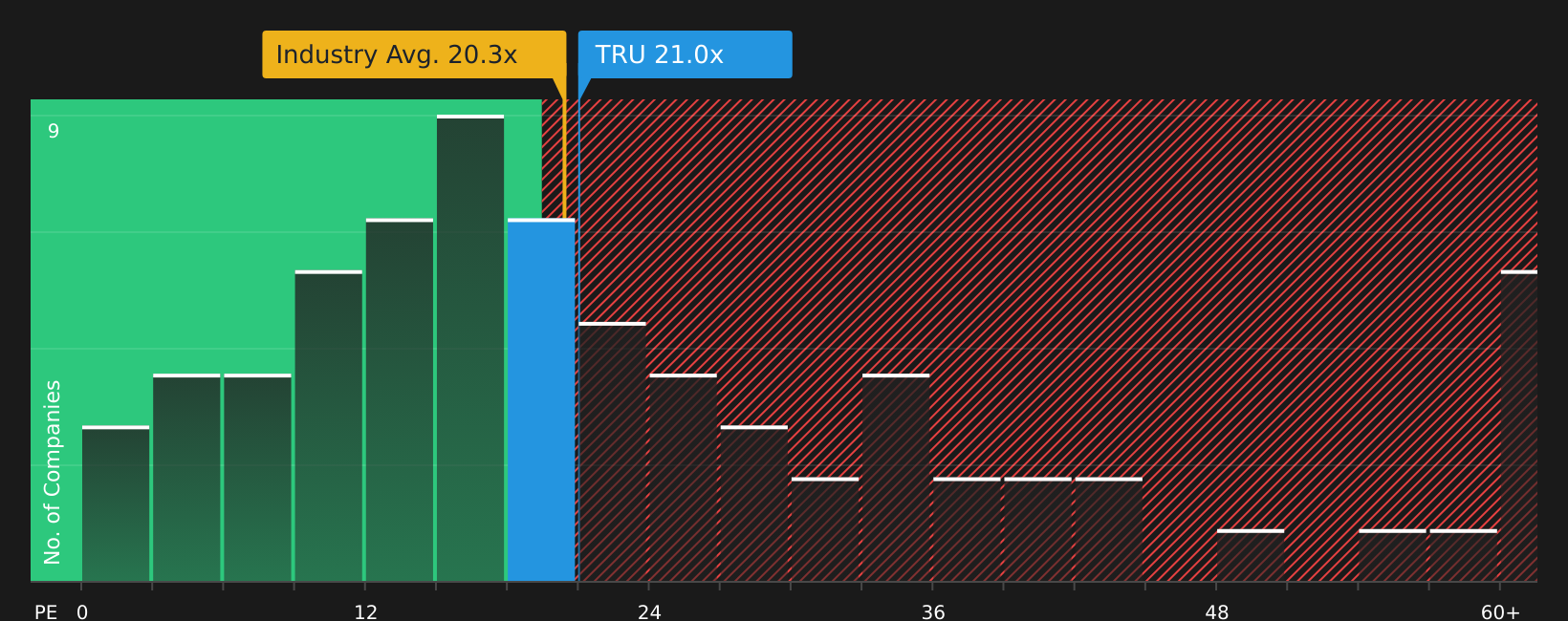

The popular narrative around TransUnion leans on detailed cash flow forecasts, but the current share price also reflects how the market values its earnings today. On that score, TRU trades on a P/E of 21.6x versus a fair ratio of 20.7x, only slightly richer than where the market could move toward.

The same P/E is just above the US Professional Services industry at 21.1x, yet sits well below the peer average of 32x. This leaves investors weighing whether that middle ground points to limited upside or a margin of safety if sentiment improves.

Before leaning too heavily on any single number, it is worth asking which scenario feels more realistic to you, and what would need to change in TransUnion’s story for that view to play out.

Next Steps

With sentiment on TransUnion clearly mixed, use this as a prompt to act quickly, review the underlying data, and weigh up the 3 key rewards and 2 important warning signs.

Looking For More Investment Ideas Beyond TransUnion?

Do not stop your research with TransUnion; widen your opportunity set with data driven stock ideas tailored to different risk levels, income needs, and growth preferences.

- Target potential bargains by scanning companies that look mispriced on both quality and value using the 45 high quality undervalued stocks.

- Strengthen your income stream by focusing on companies that pair higher dividend yields with resilient profiles through the 9 dividend fortresses.

- Reduce portfolio stress by concentrating on businesses that score well on financial resilience with the 74 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.