Travelers (TRV) Stock May Be 50% Below Fair Value After AI Launch

Travelers Companies, Inc. TRV | 0.00 |

Travelers Companies stock has climbed 138.8% over the past five years, yet the latest Excess Returns intrinsic value estimate suggests the shares may still sit well below what the underlying cash flows imply, even as traditional earnings multiples look closer to fair value.

- Over five years, Travelers Companies has returned 138.8%, a run that puts extra focus on whether the current valuation still leaves a margin of safety.

- On the upside, recent earnings growth, underwriting discipline and AI driven efficiency projects can support expectations for durable profitability. On the other hand, exposure to catastrophe losses and the execution risk around new technology may weigh on how investors price that cash flow.

- Travelers Companies currently screens as attractively priced on the broader checks, with the valuation framework indicating the stock looks inexpensive in 5 of 6 measures here.

The issue now is whether the share price already reflects that stronger profitability story or if the intrinsic value estimate still points to meaningful upside from here.

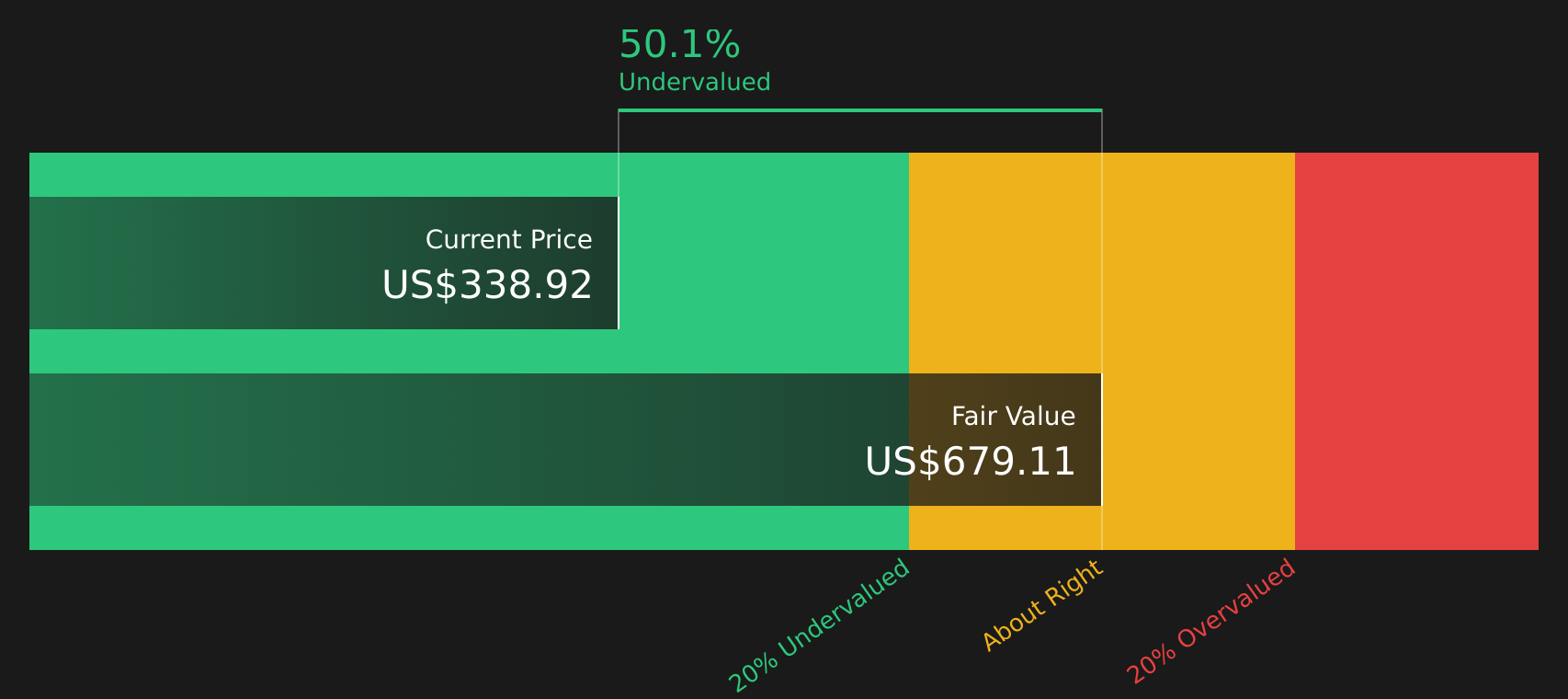

Does Travelers Companies Look Undervalued on Excess Returns?

The Excess Returns model looks at how efficiently Travelers Companies turns its equity base into earnings, then compares that to the cost of equity to estimate what the stock could be worth. For Travelers Companies, the inputs are quite strong, with a stable earnings estimate of $30.45 per share on a book value base of $150.45 per share and an average return on equity of 17.13%.

Against a cost of equity of $12.64 per share, the model estimates an excess return of $17.82 per share and a stable book value of $177.78 per share. Taken together, these translate into an intrinsic value estimate of $677 per share. Relative to the current share price, that implies the stock is 49.9% undervalued. The recent launch of TravelersLLM and other AI initiatives helps explain why the model is comfortable assuming that current return on equity levels can support that valuation.

On this Excess Returns view, Travelers Companies stock currently screens as undervalued relative to what its projected profitability on equity would justify.

Our Excess Returns analysis suggests Travelers Companies is undervalued by 49.9%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

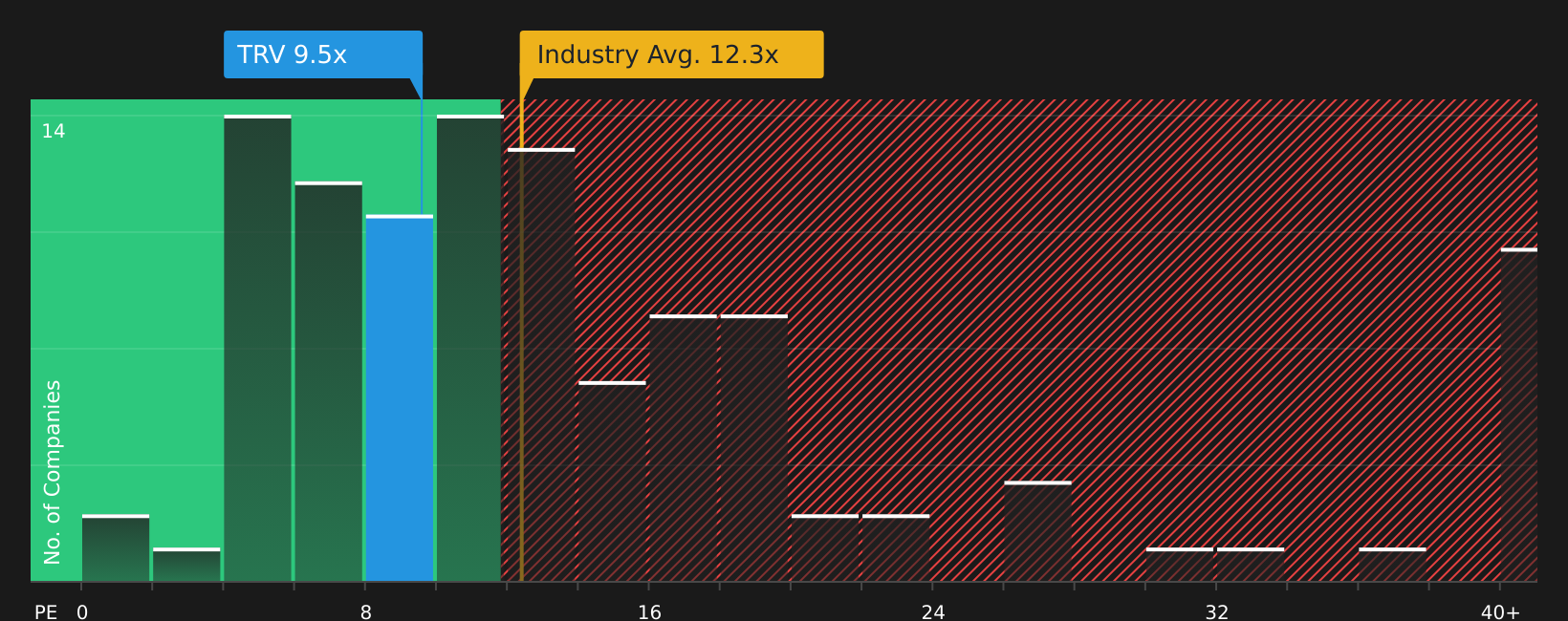

Where Does Travelers Companies Sit on Earnings?

The P/E ratio fits Travelers Companies well because earnings are a core yardstick for mature insurers. Travelers Companies currently trades on a P/E of 9.5x, very close to the peer average of 9.6x and below the broader insurance industry average of 12.3x. On Simply Wall St’s tailored “fair” P/E of 9.7x, which accounts for the company’s size, profitability profile and risk, the stock is only slightly below where this framework would typically place it.

This tight range between the current 9.5x, the peer group, and the 9.7x fair ratio suggests the market is broadly aligned with the earnings power that Travelers Companies is expected to deliver, even after the recent attention around TravelersLLM and other AI projects. The P/E does not signal a clear bargain or a stretched price; instead, it points to a stock that is roughly in line with what similar insurers trade for once differences in quality and risk are adjusted for.

On the P/E multiple, Travelers Companies stock looks priced about fairly relative to both peers and its modelled “fair” earnings valuation.

The Travelers Companies Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the valuation puzzle for Travelers Companies leaves off. They spell out which expectations for future growth, margins and earnings would need to hold for the stock to be worth meaningfully more or less than today's price. Each scenario ties a fair value to a particular set of potential catalysts and risks for Travelers Companies' business, so you can track over time which version of events appears closest to what is unfolding in the real world.

Share a narrative on Travelers Companies' stock to set out your number-driven view on how TravelersLLM, underwriting discipline and recent earnings news might shape the story from here. Track how your thesis holds up as new results come through. Your take can help other investors weigh how those drivers could affect Travelers Companies' margins, cash flows and valuation over time.

Do you think there's more to the story for Travelers Companies? Head over to our Community to see what others are saying!

The Bottom Line

For Travelers Companies, the Excess Returns intrinsic value estimate points to a sizable discount, while the P/E multiple suggests the stock is priced about in line with peers and its own earnings profile. That split reflects a core tension between what the company might earn on its equity over time and what the market is currently willing to pay for that earnings stream.

The key question from here is whether Travelers Companies can sustain its return on equity and execute on AI and underwriting projects without unexpected hits from catastrophe exposure turning the apparent discount into a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.