Trimble (TRMB) Valuation Check After Q3 Beat And Raised 2025 Outlook

Trimble Inc. TRMB | 65.12 | +0.06% |

Why Trimble’s latest earnings and dealer news matter for shareholders

Trimble (TRMB) recently reported Q3 2025 results that were ahead of expectations, with strong revenue and record annualized recurring revenue, and raised its full year 2025 outlook under the Connect & Scale strategy.

At the same time, the company named West Side Tractor Sales Co. as the newest Trimble Technology Outlet, expanding direct access to its construction technology for John Deere earthmoving equipment users across parts of Illinois, Indiana and Michigan.

Even with the Q3 beat, higher full year outlook and the new West Side Tractor outlet highlighting interest in its construction tech, Trimble’s 30 day share price return of 17.94% and year to date share price return of 15.55% decline contrast with its 3 year total shareholder return of 18.80%. This suggests shorter term momentum has cooled while longer term holders have still seen gains overall.

If Trimble’s recent moves in construction technology have your attention, it could be a good moment to see which other infrastructure enablers are gaining interest through our 24 power grid technology and infrastructure stocks.

With Q3 results ahead of expectations, an increased 2025 outlook, and a share price that has pulled back over the past year despite a discount to some analyst estimates, you have to ask: Is Trimble undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 32.6% Undervalued

Trimble’s most followed narrative pegs fair value at about $98.08, well above the last close of $66.15, and ties that gap to specific growth and margin assumptions.

The migration from hardware-focused, CapEx models to bundled, subscription-based offerings, even in traditionally hardware-oriented segments, expands the addressable market, improves revenue visibility, and increases recurring revenue mix, driving greater predictability and enhanced long-term earnings.

Want to see what is baked into that fair value gap? This narrative leans on rising recurring revenue, fatter margins, and a future earnings base that looks very different to today. Curious which specific growth and profitability assumptions are doing the heavy lifting here, and how they tie back to Trimble’s end markets and business mix?

Result: Fair Value of $98.08 (UNDERVALUED)

However, that upside story can be knocked off course if federal spending softness persists or if faster moving rivals compress pricing power and margins.

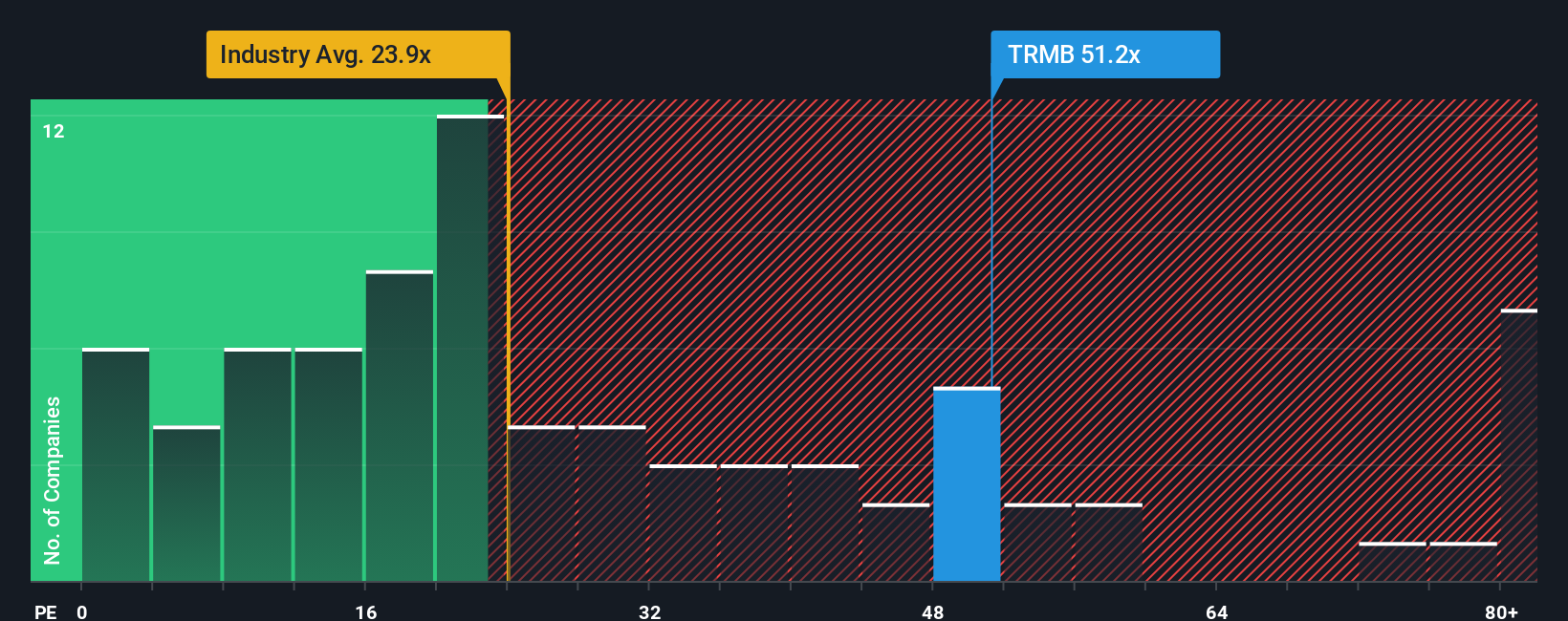

Another View: Valuation Looks Full On Earnings

The earlier narrative leans on a fair value of $98.08, yet today the stock trades on a P/E of 44x. That is richer than the peer average of 31.5x and above a fair ratio of 33.6x that our work suggests the market could move toward over time.

If the share price eventually settles closer to that 33.6x fair ratio or the 31.5x peer level, today’s entry point could carry more valuation risk than the headline discount to fair value implies. The real question for you is whether Trimble’s future earnings path justifies paying this kind of premium.

Build Your Own Trimble Narrative

If you see the data differently or prefer to stress test your own assumptions, you can build a Trimble view tailored to your thesis in minutes, starting with Do it your way.

A great starting point for your Trimble research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Trimble is on your radar, do not stop here. The next moves in your portfolio often come from ideas you almost skipped past.

- Target quality at a discount by scanning companies on our 52 high quality undervalued stocks and see which names line up with your return expectations and risk tolerance.

- Strengthen your defensive core by reviewing businesses in the solid balance sheet and fundamentals stocks screener (45 results) that pair cleaner balance sheets with fundamentals you can scrutinise in detail.

- Stay one step ahead by checking our screener containing 24 high quality undiscovered gems before the crowd pays attention to the same set of companies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.