Tripadvisor (TRIP) Valuation Check After Mixed Q1 2026 Results And Wider Net Loss

TripAdvisor, Inc. TRIP | 0.00 |

Tripadvisor (TRIP) is back in focus after first quarter 2026 earnings showed revenue of US$382.4 million, a wider net loss, and mixed segment trends shaped by geopolitical disruptions and destination specific issues.

Tripadvisor's recent Q1 loss and softer Hotels performance appear to be weighing on sentiment, with a 4.5% 1 month share price return not offsetting a 23.3% year to date share price decline and a 24.8% 1 year total shareholder return loss. This suggests momentum has been fading despite progress in Experiences and TheFork.

If Tripadvisor's recent volatility has you rethinking your watchlist, this could be a good moment to scan for travel and experience platforms within broader consumer and tech themes through 18 top founder-led companies

With Tripadvisor trading at US$11.23, carrying an intrinsic value estimate at a sizeable discount and sitting below analyst targets, the central question is whether this weakness offers an entry point or if the market already reflects its future growth.

Most Popular Narrative: 21.9% Undervalued

Tripadvisor's most followed narrative points to a fair value of $14.38 per share compared with the last close at $11.23, highlighting a sizeable valuation gap that is based on long term growth assumptions and cash flow projections.

Tripadvisor's focus on scaling its experiences marketplace (Viator and TheFork) takes advantage of global consumer shifts toward experiential travel, as rising international leisure travel from the expanding middle class and a preference for unique experiences are both enlarging the company's addressable market and supporting sustainable, above-industry growth rates, positively impacting long-term revenue and gross profit.

Want to see what sits behind that growth story and fair value gap? The narrative emphasizes expectations for future earnings strength, richer margins and a higher quality revenue mix. The key assumptions are all quantified, but only if you read on.

Result: Fair Value of $14.38 (UNDERVALUED)

However, this depends on Tripadvisor easing traffic pressures in its core Hotels and Other segment, while also avoiding further margin strain from lower margin Experiences growth and heavier marketing spend.

Another View: Earnings Multiple Sends a Different Signal

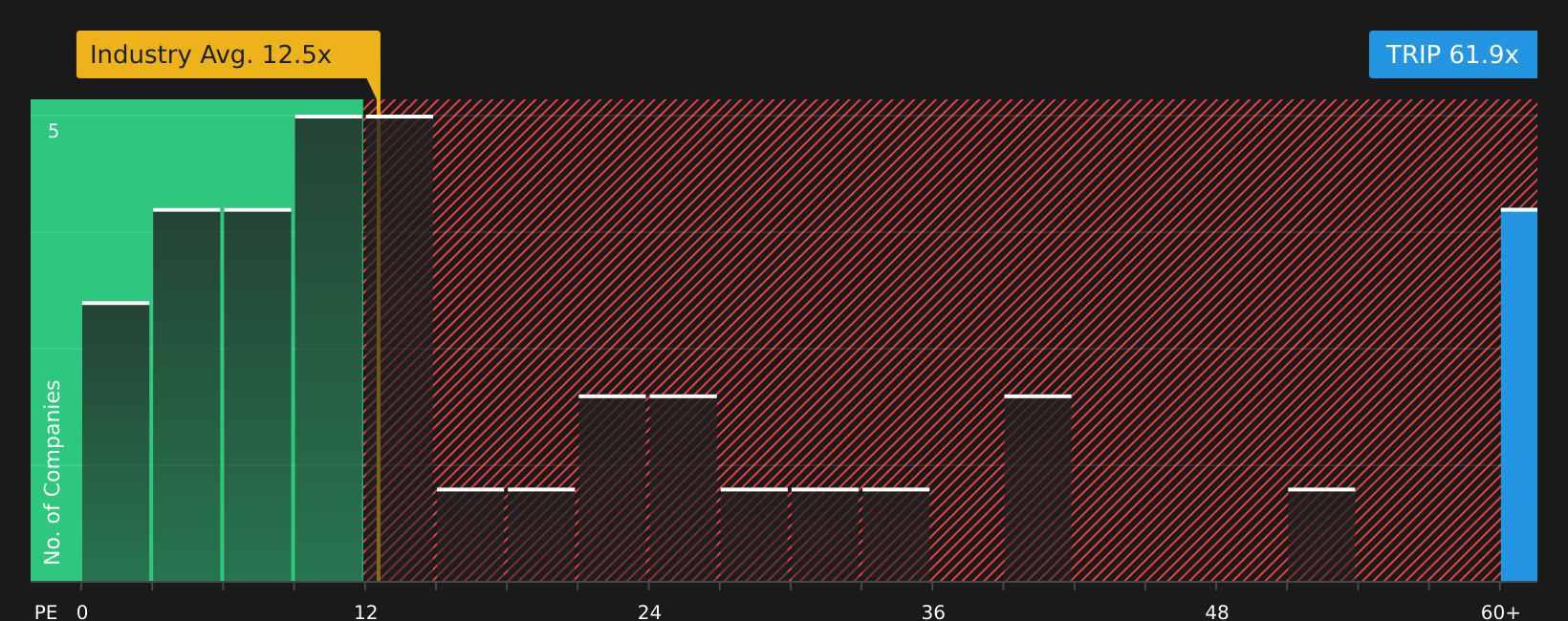

The discounted cash flow work points to Tripadvisor trading well below an estimated fair value, yet the P/E ratio tells a more cautious story. At 69.3x earnings, the stock sits well above the US Interactive Media and Services average of 20.1x, the peer average of 16.4x and a fair ratio of 27.4x. That gap suggests investors are already paying up heavily for future earnings. This raises the question of whether the discount to fair value is a bargain or a warning sign about valuation risk.

For a closer look at how this earnings multiple compares with peers and where the fair ratio suggests the market could move, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly split between valuation upside and rich earnings multiples, it makes sense to review the numbers independently and move quickly to shape your own stance using 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If Tripadvisor has you reassessing your next move, do not stop here. Broaden your watchlist now so you are not late to the next opportunity.

- Target potential mispricings by scanning 51 high quality undervalued stocks and see which stocks currently trade below their assessed worth.

- Prioritise resilience by using the solid balance sheet and fundamentals stocks screener (44 results) for companies that pair financial strength with fundamentals that may handle tougher conditions.

- Spot future standouts early through the screener containing 23 high quality undiscovered gems and keep an eye on quality businesses that many investors may still be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.