Twilio (TWLO) Q4 EPS Loss Challenges Profitability‑Focused Bull Narrative

Twilio, Inc. Class A TWLO | 132.56 | +0.78% |

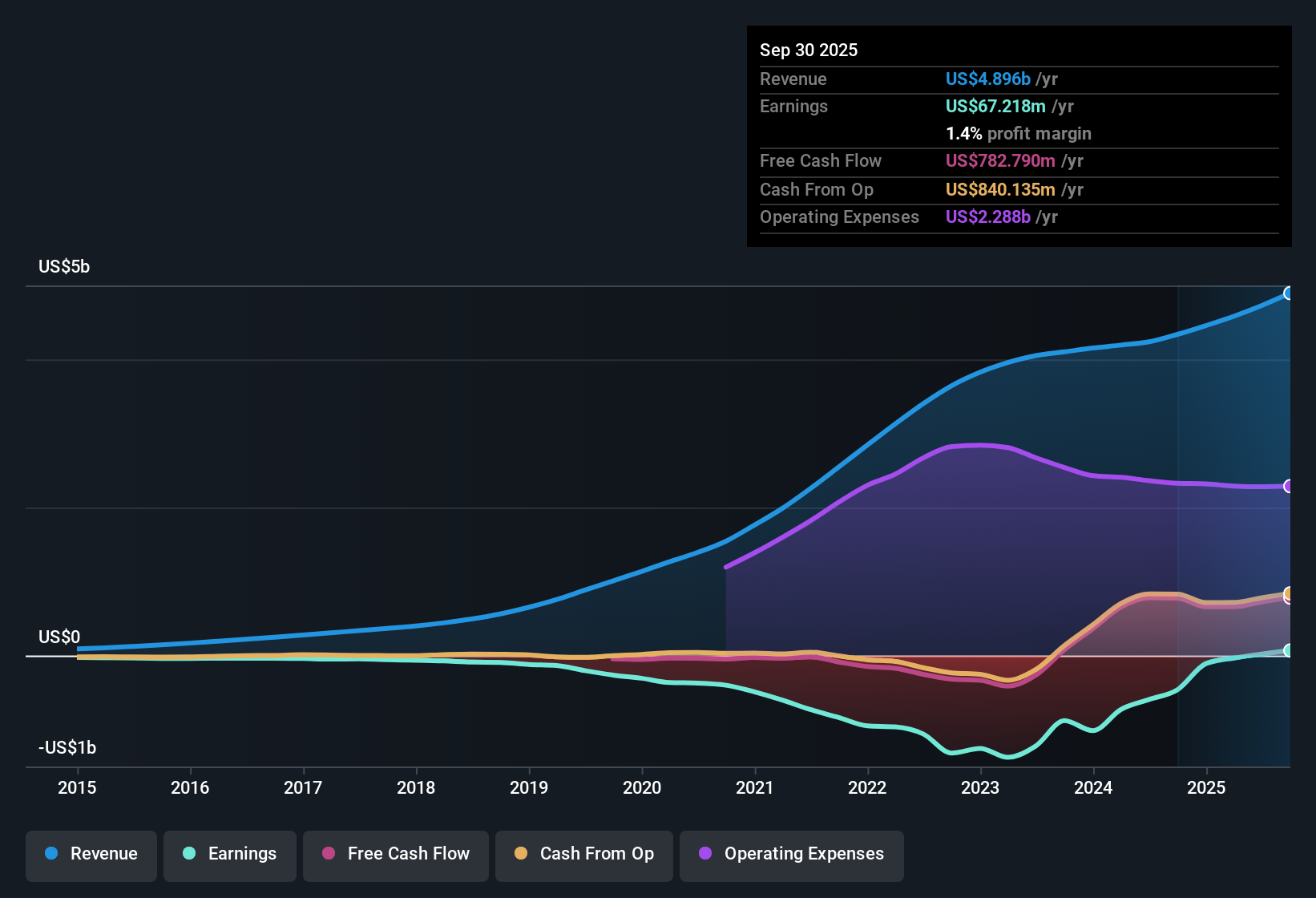

Twilio (TWLO) closed FY 2025 with fourth quarter revenue of US$1.37b and basic EPS of a US$0.30 loss, as net income excluding extra items came in at a loss of US$45.85m. Across the year, the company has seen quarterly revenue move from US$1.17b in Q1 to US$1.37b in Q4. Basic EPS ranged from US$0.13 in Q1 to US$0.24 in Q3, before swinging back to a loss in the final quarter. This sets up a mixed but margin-focused story for investors to unpack.

See our full analysis for Twilio.With the headline numbers on the table, the next step is to see how this earnings profile lines up with the dominant narratives around Twilio's growth, profitability and risk over the past year.

US$5.1b trailing revenue with thin profits

- Over the last twelve months to Q4 FY 2025, Twilio generated about US$5.1b in revenue and US$33.8m in net income excluding extra items, which works out to a slim profit relative to the top line.

- Consensus narrative talks about higher margin software and AI products supporting future margin improvement. However, the latest quarter shows a net income loss of US$45.9m on US$1.37b of revenue, so investors have to weigh those margin hopes against how narrow profitability currently is.

Quarterly EPS swings around new profitability

- Trailing twelve month basic EPS sits at US$0.22, but quarterly EPS moved from a profit of US$0.24 in Q3 FY 2025 to a loss of US$0.30 in Q4, and management also flagged a one off loss of US$16.9m that affected the trailing numbers.

- Bulls focus on earnings growing about 25.9% per year over the last five years and forecasts of roughly 34.3% annual earnings growth. However, the abrupt shift from Q3 profit to a Q4 loss plus that US$16.9m one off charge shows how bumpy the road to more stable EPS can be.

Valuation signals vs slower revenue growth

- At a share price of US$113, Twilio is trading below a DCF fair value of about US$152.72 and below the single allowed analyst price target of US$143.47, while its P/S of 3.4x is cheaper than the 6x peer average but richer than the broader US IT sector at 2.1x.

- Bears point out that revenue is only expected to grow around 7.6% per year compared with a 10.3% US market forecast. As a result, even with a market price below DCF fair value and below that US$143.47 target, the combination of slower expected top line growth and a P/S above the wider IT group is exactly the kind of setup they worry could cap future re rating potential.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Twilio on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? If this earnings story looks different to you, shape your own view in just a few minutes and Do it your way

A great starting point for your Twilio research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Twilio is working with thin profitability, uneven quarterly EPS and slower expected revenue growth. Together, these factors leave limited room for earnings or valuation disappointments.

If that mix of earnings swings and growth constraints feels uncomfortable, shift some attention to our 86 resilient stocks with low risk scores to quickly spot ideas where stability and risk management sit front and center.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.