Twist Bioscience (TWST) Valuation After Q1 Beat And Raised 2026 Outlook

Twist Bioscience TWST | 57.41 57.41 | +13.95% 0.00% Pre |

Twist Bioscience (TWST) shares have been in focus after the company paired better than expected Q1 revenue of US$103.7 million with a higher full year 2026 sales outlook and reiterated adjusted EBITDA breakeven ambitions.

The stronger Q1 update and raised 2026 sales outlook have arrived alongside a sharp shift in sentiment, with a 30 day share price return of 40.13% and a 90 day share price return of 57.10% at a last close of US$48.12. That short term momentum contrasts with a 1 year total shareholder return decline of 10.32% and a 5 year total shareholder return decline of 71.15%, although the 3 year total shareholder return rise of 83.66% shows how quickly expectations for Twist Bioscience can change when investors focus on growth potential and execution risks.

If Twist’s recent move has you thinking about where growth stories might emerge next, it could be worth lining up other healthcare stocks that match your own view on risk and reward.

With Twist now trading close to the average analyst price target and riding a sharp short term rally, the key question is whether recent guidance and growth traction still leave upside on the table or if the market is already pricing in future gains.

Most Popular Narrative: 35.1% Overvalued

With Twist Bioscience’s fair value in the leading narrative sitting at $35.63 against a last close of $48.12, the story hinges on how far future growth and margins can stretch to justify that gap.

Significant improvements in gross margin (now above 50%) through volume leverage, process improvements, and increased vertical integration signal ongoing margin expansion and a clear near term path toward adjusted EBITDA breakeven, indicating robust future earnings potential.

Curious what kind of revenue curve, margin uplift and future earnings multiple are baked into that view, and how they connect to the current analyst target spread? The full narrative lays out the chain of assumptions behind that $35.63 mark and the premium growth profile it implies.

Result: Fair Value of $35.63 (OVERVALUED)

However, there is still a chance that customer concentration in NGS and the ongoing EBITDA losses will force Twist to raise capital and reset growth expectations.

Another View: Revenue Multiple Sends a Different Signal

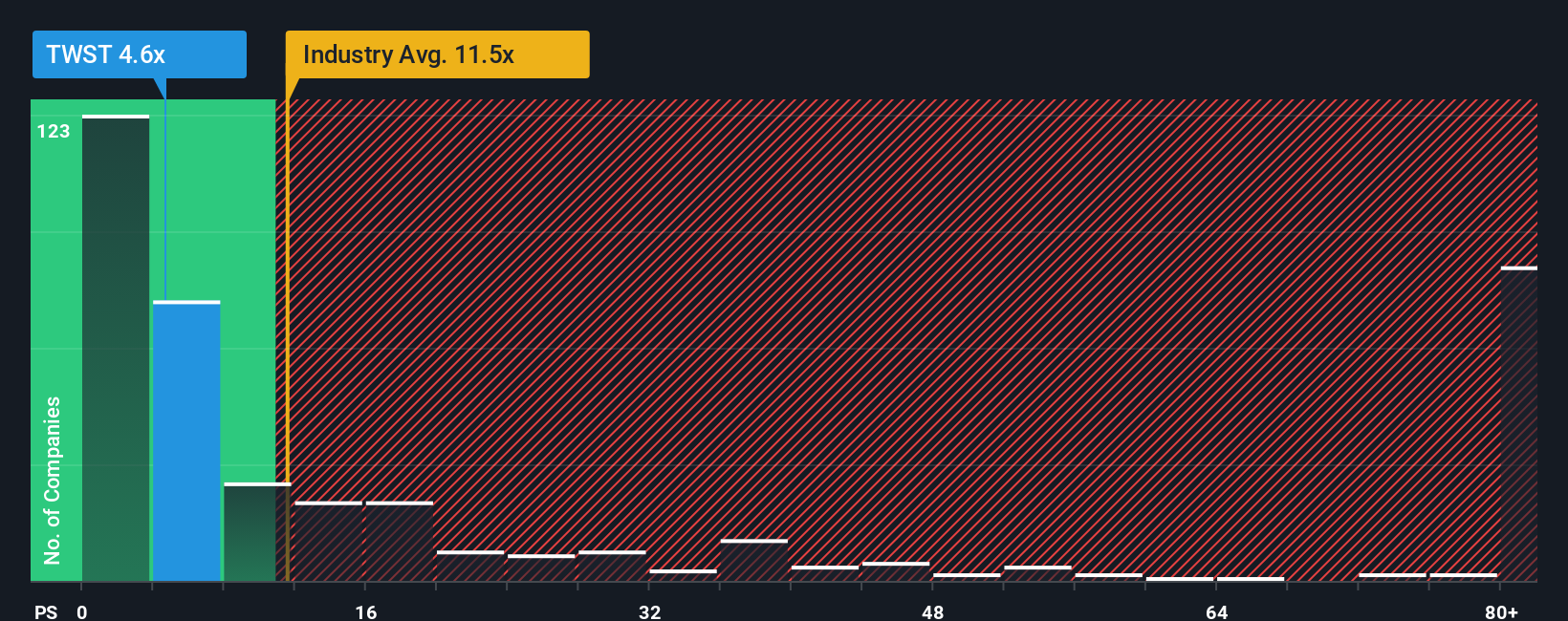

That 35.1% overvalued fair value sits awkwardly next to Twist’s current P/S ratio of 7.5x, which is lower than both the US Biotechs industry average of 12x and a peer average of 17.4x, but higher than the fair ratio of 4.3x that the market could move toward. So which signal do you trust?

Build Your Own Twist Bioscience Narrative

If you see the data differently or prefer to test your own assumptions, you can build a full Twist Bioscience story in minutes, Do it your way.

A great starting point for your Twist Bioscience research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready to hunt for your next idea?

If Twist has sparked your interest, do not stop here. Put Simply Wall St’s screeners to work and line up your next three investing ideas.

- Spot potential mispricings by checking out these 866 undervalued stocks based on cash flows that may offer stronger cash flow support for their share prices.

- Ride the AI trend more selectively by scanning these 30 AI penny stocks that link artificial intelligence themes with business models you understand.

- Add an income angle by reviewing these 11 dividend stocks with yields > 3% that combine higher yields with the financial profiles you prefer.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.