Udemy (UDMY): Evaluating Valuation Following AI Course Surge and Release of Skills Trends Report

Udemy, Inc. UDMY | 4.70 | +1.62% |

If you have been tracking Udemy (UDMY) recently, the latest buzz will likely catch your attention. The company’s new 2026 Global Learning & Skills Trends Report is making waves, showcasing a remarkable surge in demand for generative AI courses on its platform and highlighting the explosion in consumption of Microsoft Copilot and GitHub Copilot content. With 11 million enrollments in these courses already, it is clear Udemy is becoming a go-to destination for enterprise upskilling in the new AI-driven workplace.

The market’s reaction has been quick, and shares jumped 2.6% on the news, extending a stretch of moderate gains over the past month. While Udemy’s stock still trails its level from a year ago, the recent uptick signals that momentum may be building as businesses ramp up investment in employee AI skills. Alongside the growth story, the company’s Board has authorized a $50 million share repurchase, signaling conviction in its future prospects and a willingness to return value to shareholders.

The question now is whether this fresh momentum and clear corporate demand for AI upskilling make Udemy a value buy, or if the market is already looking ahead and pricing in further growth.

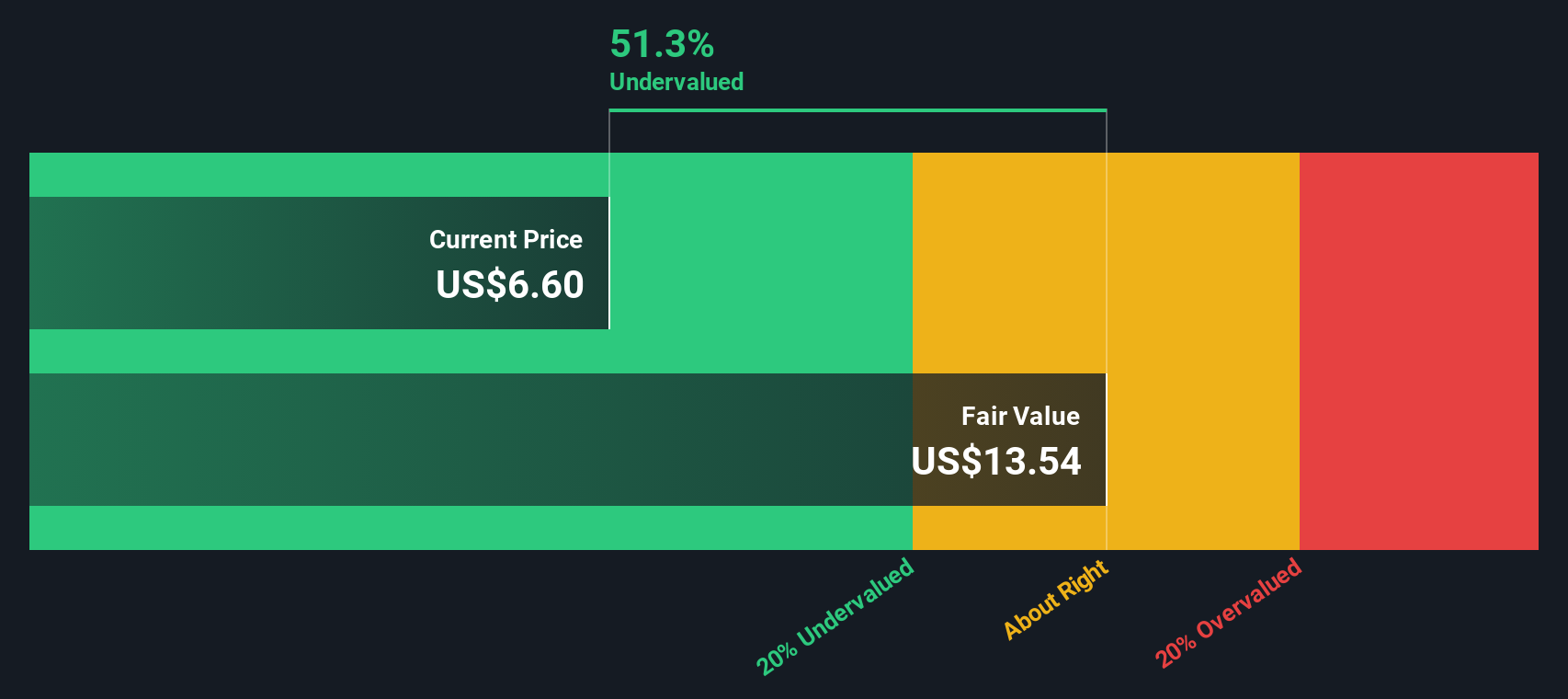

Most Popular Narrative: 28.7% Undervalued

The prevailing narrative sees Udemy as notably undervalued, suggesting significant upside potential compared to its estimated fair value.

Acceleration of global upskilling and workforce reskilling, driven by the widespread adoption of AI and rapid technological change, is increasing enterprise demand for Udemy's training solutions. As organizations seek ongoing and personalized skill development at scale, this is leading to a growing pipeline, higher contract values, and early signs of net new ARR growth, supporting future revenue acceleration.

What is fueling this bullish forecast? The secret behind this narrative is a combination of bold revenue and profit projections along with a premium profit multiple. Want to know why analysts believe Udemy could outpace current expectations? Dive deeper to see the hidden numbers and ambitious milestones that underpin this compelling valuation thesis.

Result: Fair Value of $10.17 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent weakness in Udemy’s consumer segment and ongoing challenges with contract renewals could temper optimism around its undervaluation story.

Find out about the key risks to this Udemy narrative.Another View: Our DCF Model’s Take

Stepping back from market multiples, our SWS DCF model offers a different perspective. This approach also considers Udemy undervalued, but uses future cash flow estimates. Could long-term assumptions change your outlook?

Build Your Own Udemy Narrative

Keep in mind, if you would rather dig into the numbers yourself or shape a personal view, building your own narrative takes less than three minutes. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Udemy.

Looking for More Smart Investment Opportunities?

Don’t let your strategy stop here. Expand your search to high-potential companies already catching Wall Street’s eye. Unlock ideas that go far beyond the obvious, built on the trends shaping tomorrow’s market winners. Opportunity isn’t waiting, and neither should you.

- Supercharge your portfolio with companies leading breakthroughs in quantum computing by using the quantum computing stocks screener.

- Catch early-stage innovators with strong balance sheets and explosive potential inside our selection of penny stocks with strong financials opportunities.

- Boost your income outlook with handpicked businesses offering consistent, high-yield payouts through the dividend stocks with yields > 3% screen.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.