UGI (UGI) Could Be 18% Below Fair Value On Reset Loan Terms

UGI Corporation UGI | 0.00 |

Why UGI's New Loan Terms Matter For Investors

UGI (UGI) is back on investor radar after its subsidiary, UGI Energy Services, amended a term loan credit facility, resetting interest margins that will influence the company’s future borrowing costs and refinancing plans.

The Fourth Amendment sets the Applicable Rate at 2.00% per annum for SOFR loans and 1.00% per annum for base rate loans under the existing term loan. For UGI stockholders, the key question is how these revised financing terms might affect overall interest expense and flexibility in managing upcoming debt needs.

At a share price of $35.59, UGI has seen its short term share price momentum soften, with a 30 day share price return of 2.56% set against a 90 day share price decline of 7.27%. Over a 3 year period, the total shareholder return of 54.71% contrasts with a slight 5 year total shareholder return decline of 2.18%, suggesting earlier gains have moderated even as the latest loan amendment refocuses attention on financing terms.

If you are weighing how UGI fits alongside other opportunities in the energy and infrastructure space, it can help to see what else is moving. Use this as a springboard to check out 35 power grid technology and infrastructure stocks

UGI trades about 22% below the average analyst price target after a period of softer share performance and fresh loan terms that reset borrowing costs. Is the discount a cushion against risk, or a signal the market remains cautious?

Most Popular Narrative: 17.9% Undervalued

UGI's most followed narrative pegs fair value at $43.33 per share, above the last close at $35.59. This puts a spotlight on what is driving that gap.

Anticipated implementation of new, higher utility rates in Pennsylvania, pending regulatory approval, will provide substantial incremental revenue beginning in fiscal 2026, supporting continued investment in grid resiliency and modernization.

Want to see what sits behind that Pennsylvania focus for UGI? The narrative leans heavily on future revenue, margin lift and a re rated earnings multiple. The valuation hinges on how those moving parts line up over time.

Result: Fair Value of $43.33 (UNDERVALUED)

However, UGI investors still need to watch for pressure points, including ongoing customer attrition at AmeriGas and potential regulatory setbacks in Pennsylvania that could weaken this undervaluation story.

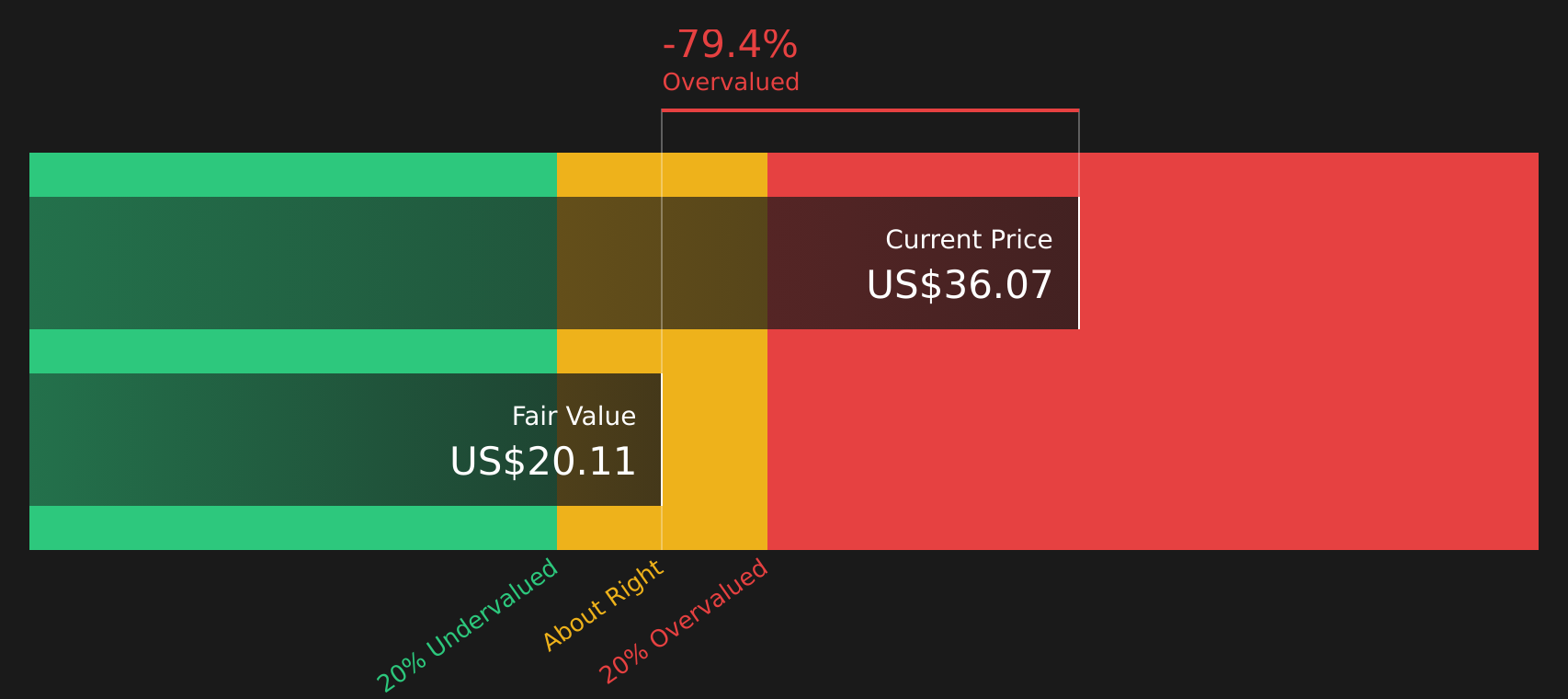

Another View: SWS DCF Flags Overvaluation

While the consensus narrative has UGI at a fair value of $43.33 and frames the stock as 17.9% undervalued, the Simply Wall St DCF model points in the opposite direction. On that cash flow based view, UGI at $35.59 is trading well above an estimated value of $20.11, which implies investors are paying a premium for future cash flows.

When one method points to upside and another signals overvaluation, it puts the focus squarely on your own assumptions about UGI's long term growth, margins and capital needs. Which set of expectations do you think is closer to reality, and what would change your mind?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out UGI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around UGI, do the current risks and rewards feel balanced enough for you? If you want to move quickly from headline impressions to your own evidence based view, start by weighing the 5 key rewards and 2 important warning signs

Looking for more investment ideas beyond UGI?

Do not stop your research with UGI. Broaden your watchlist using focused stock ideas sourced from the Simply Wall St screener tools.

- Target potential upside by scanning companies that combine quality fundamentals with attractive pricing through the 44 high quality undervalued stocks.

- Strengthen your income stream by zeroing in on companies offering higher yields with the 9 dividend fortresses.

- Prioritise capital preservation by reviewing companies with lower risk profiles using the 72 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.