UGI (UGI) Valuation Check After EBIT Growth LPG Portfolio Rationalization And Moody’s Outlook Upgrade

UGI Corporation UGI | 36.77 | +1.94% |

UGI (UGI) is back in focus after reporting first quarter results that included a 5% year over year EBIT increase, the completion of its LPG portfolio rationalization, and a Moody’s outlook upgrade for AmeriGas.

Despite the recent EBIT progress and LPG portfolio clean up, UGI’s share price has been under some pressure in the short term, with a 1 day share price return of a 2% decline and a 7 day share price return of a 7.6% decline, while the 90 day share price return of 7.2% and 1 year total shareholder return of 22.7% suggest momentum has been building over a longer horizon.

If UGI’s latest moves have you rethinking where growth could come from next, this is a good moment to widen your search with 24 power grid technology and infrastructure stocks tied to future energy infrastructure themes.

With earnings per share lower than last year but EBIT up 5% and the stock trading below the average analyst price target, is UGI quietly undervalued right now, or is the market already pricing in future growth?

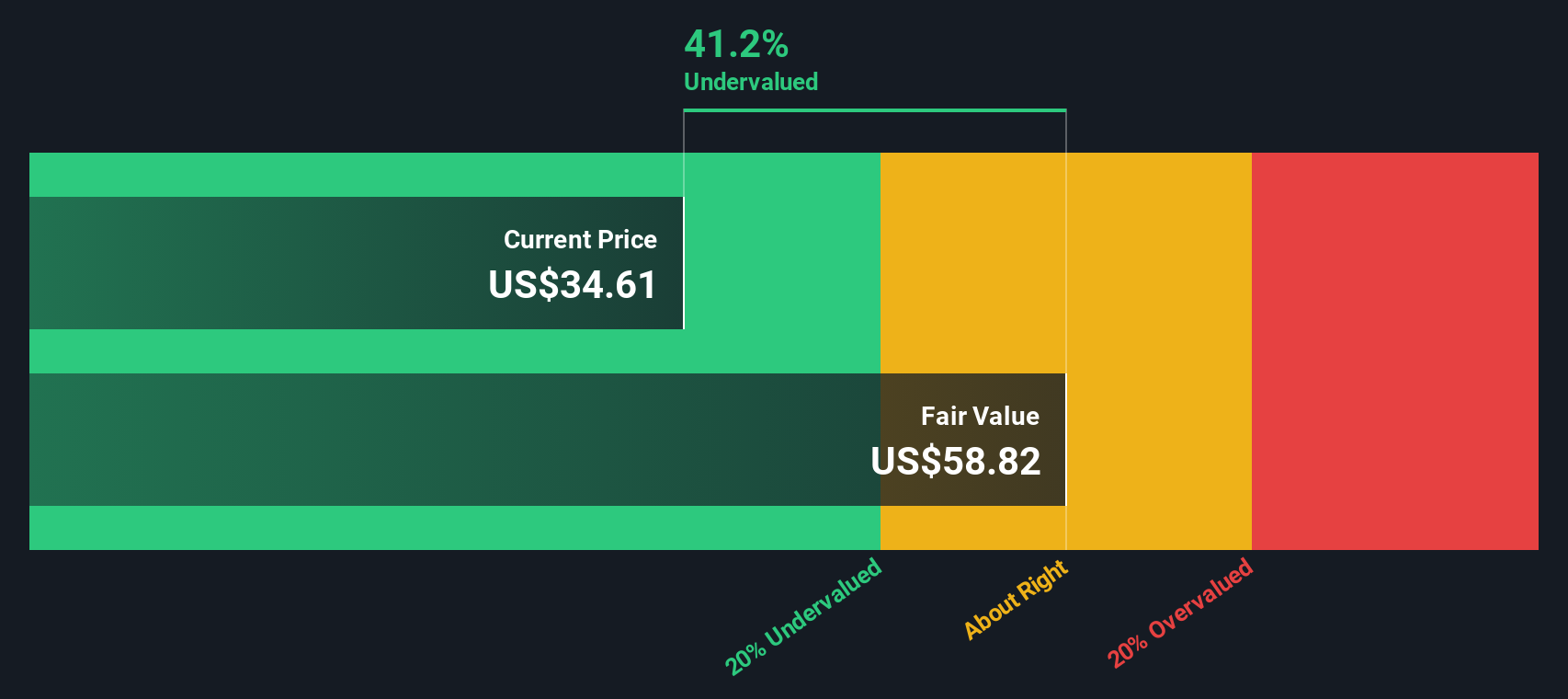

Most Popular Narrative: 16.7% Undervalued

UGI's most followed narrative pegs fair value at $44.50 per share, comfortably above the last close at $37.09. This frames a clear valuation gap for investors to assess.

Divestiture of non-core, low-margin LPG assets and redeployment of proceeds into higher-return, regulated utility and energy services businesses enable greater financial flexibility, prudent deleveraging, and improved overall earnings quality.

Curious how a regulated utility story supports that higher price tag? The narrative leans heavily on steadier margins, measured revenue growth and a future earnings multiple that does not stretch typical sector expectations. The tension between slower top line assumptions and firmer profitability is where the valuation really takes shape.

Result: Fair Value of $44.50 (UNDERVALUED)

However, steady margin plans face real pushback if LPG demand keeps eroding in Europe, or if regulators clamp down on returns and future rate cases.

Another View: Cash Flows Tell a Different Story

While the popular narrative points to a fair value of $44.50 per share, our DCF model lands in a very different place. On that basis, UGI at $37.09 is trading above an estimated future cash flow value of $17.51, which screens as overvalued rather than undervalued. For you, the key question is which set of assumptions feels more realistic.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out UGI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own UGI Narrative

If you think the consensus story misses something, or you simply prefer to test the numbers yourself, you can build a custom view in minutes, starting with Do it your way

A great starting point for your UGI research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If UGI has sharpened your thinking but not fully sealed your next move, now is the time to broaden your watchlist with focused, data driven ideas.

- Target potential value opportunities by checking out our 52 high quality undervalued stocks that may offer stronger fundamentals at prices that still look reasonable.

- Strengthen your income profile by reviewing 14 dividend fortresses, built around companies with higher yields that might help support more consistent cash returns.

- Protect your downside by scanning 84 resilient stocks with low risk scores, highlighting businesses with lower risk scores that could help balance out bolder positions in your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.