Ultra Clean Holdings (UCTT) Could Be 21% Overvalued As Growth Hopes Stay Strong

Ultra Clean Holdings, Inc. UCTT | 0.00 |

Index changes put Ultra Clean Holdings in focus

Ultra Clean Holdings (UCTT) is back on investors' radar after being dropped from several Russell value indexes, a technical reshuffle that contrasts with the stock's very strong recent price performance and earnings growth projections.

Ultra Clean Holdings has been volatile around the index reshuffle, with the share price down 9.12% on the day at US$129.59, yet still showing a year to date share price return of 374.34% and a 1 year total shareholder return of 418.98%. This points to powerful but recently cooling momentum.

If you are looking beyond Ultra Clean Holdings for other semiconductor related opportunities, this could be a good moment to scan the market via 53 AI infrastructure stocks

With Ultra Clean Holdings now excluded from several value indexes but trading near an all time high after a very large 1 year gain, the key question is whether investors are overlooking additional upside or whether the market already reflects expectations for future growth.

Most Popular Narrative: 20.7% Overvalued

With Ultra Clean Holdings last closing at $129.59 against a narrative fair value of $107.40, investors are weighing a rich share price against an earnings rebuild story that is heavily model driven.

Analysts expect earnings to reach $266.3 million (and earnings per share of $5.68) by about June 2029, up from -$194.1 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $565.7 million in earnings, and the most bearish expecting $108.9 million.

Curious what sits behind that earnings swing? The revenue build, margin reset and valuation multiple all have to line up. The full narrative connects those moving parts.

Result: Fair Value of $107.40 (OVERVALUED)

However, Ultra Clean Holdings still faces pressure from its reliance on a few large customers, as well as ongoing tariff and supply chain costs that could challenge the upbeat earnings narrative.

Another View on Ultra Clean Holdings valuation

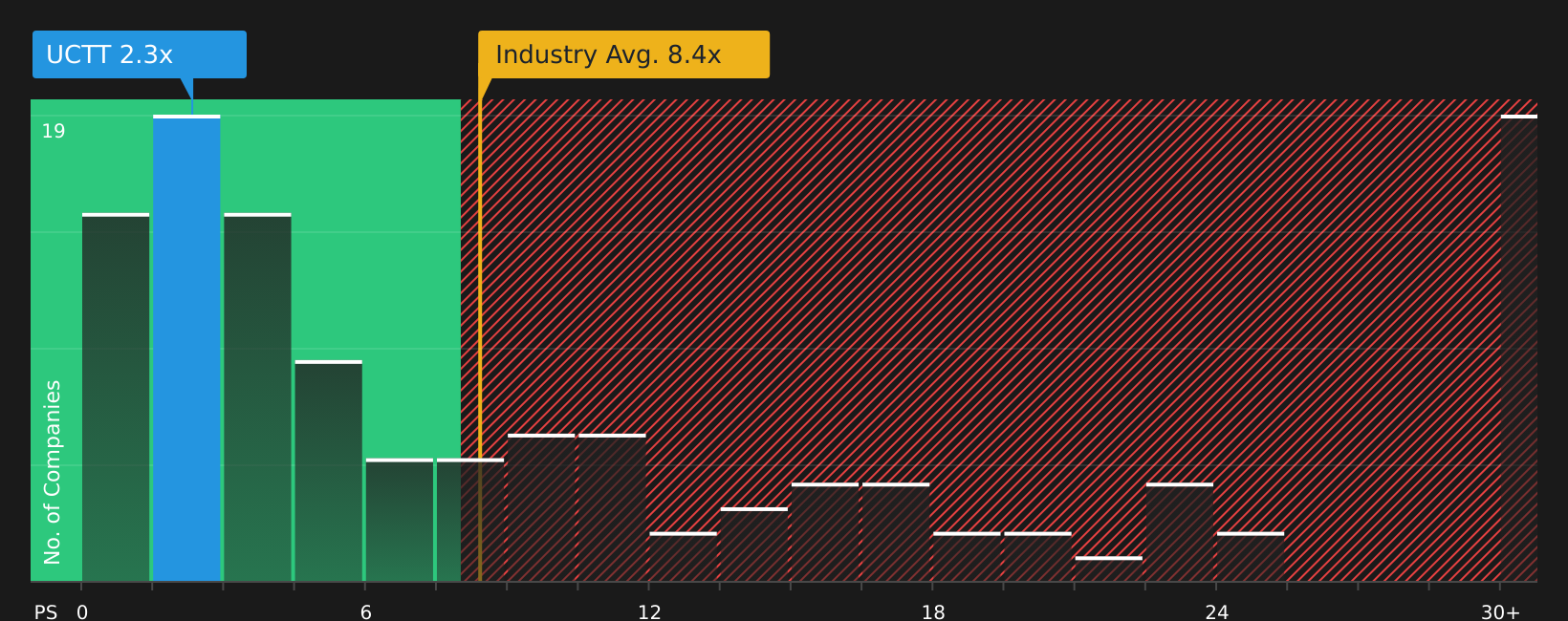

The fair value narrative pegs Ultra Clean Holdings at $107.40, about 20.7% below the current $129.59 share price, yet the stock screens as good value on a simple P/S check. At 2.8x sales versus 9.2x for the US semiconductor industry and 16.4x for peers, and below a 3.8x fair ratio estimate, the gap suggests investors are either overpaying for near term momentum or underpaying for long term earnings repair. Which side of that trade do you think you are on?

For a closer look at what the numbers imply for valuation risk, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

After reviewing Ultra Clean Holdings' strong recent returns alongside the ongoing valuation debate, this could be a good time to act decisively and examine the numbers yourself using 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Ultra Clean Holdings?

If Ultra Clean Holdings has sharpened your focus, do not stop here. Use the Simply Wall St Screener to line up fresh ideas before the next opportunity moves on.

- Target potential mispricings by scanning 41 high quality undervalued stocks that may offer stronger fundamentals relative to their current share prices.

- Prioritise resilience with solid balance sheet and fundamentals stocks screener (47 results) built around companies that pair financial strength with underlying business stability.

- Get ahead of the crowd by reviewing the screener containing 19 high quality undiscovered gems before they attract wider market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.