Ultragenyx Lawsuits And Restructuring Put UX111 Gene Therapy In Focus

Ultragenyx Pharmaceutical, Inc. RARE | 24.57 24.35 | +3.98% -0.90% Pre |

- Ultragenyx Pharmaceutical (NasdaqGS:RARE) is facing multiple shareholder class action lawsuits tied to allegations of misleading disclosures about Phase III clinical trial data.

- The lawsuits follow the company’s announcement of failed Phase III trials alongside a broad restructuring plan that includes layoffs.

- At the same time, Ultragenyx reported positive long term data for its investigational gene therapy UX111 and advanced regulatory submissions.

Ultragenyx focuses on therapies for rare and ultra rare diseases, an area where clinical outcomes and regulatory decisions can have a major impact on a company’s prospects. When late stage trials do not meet expectations, it can reshape how investors view both the product pipeline and the business model, especially when this is paired with restructuring and workforce cuts.

For you as an investor, the combination of lawsuits, trial setbacks, and encouraging UX111 data creates a more complex mix of risks and potential opportunities around NasdaqGS:RARE. Future updates on the legal process, operational changes, and regulatory feedback on UX111 may play a key role in how the company’s profile evolves from here.

Stay updated on the most important news stories for Ultragenyx Pharmaceutical by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Ultragenyx Pharmaceutical.

For Ultragenyx, this cluster of events pulls the focus squarely onto execution. On one side, you have shareholder class actions questioning past disclosures around the setrusumab Phase III trials, which can consume management time and add uncertainty around governance and communication quality. On the other, the company is cutting about 10% of its workforce and reallocating spend to what it calls its largest value drivers, while still reporting higher revenues for 2025 and guiding to further revenue growth in 2026. That combination signals a business model that is being refocused on fewer, higher priority programs such as UX111 and other late stage assets. The positive long term UX111 data and resubmitted FDA filing suggest Ultragenyx is still leaning into gene therapy, a space shared with players like Biomarin and Sarepta, where clinical data quality and regulator trust are crucial. For you, the key issue is whether cost reductions, product launches and regulatory progress can offset the financial drag from ongoing losses and any overhang from legal proceedings.

How This Fits Into The Ultragenyx Pharmaceutical Narrative

- The restructuring plan and continued investment in UX111 align with the narrative that late stage gene therapy readouts and product launches could support a path to profitability and a more diversified revenue base.

- The class action lawsuits and failed Phase III setrusumab trials challenge earlier confidence in the pipeline and highlight the execution and regulatory risks that the narrative already flags as potential threats to future earnings.

- The concentration of multiple lawsuits and workforce reductions at the same time as management reiterates a 2027 profitability goal may not be fully reflected in prior expectations about how smooth that path could be.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Ultragenyx Pharmaceutical to help decide what it's worth to you.

The Risks and Rewards Investors Should Consider

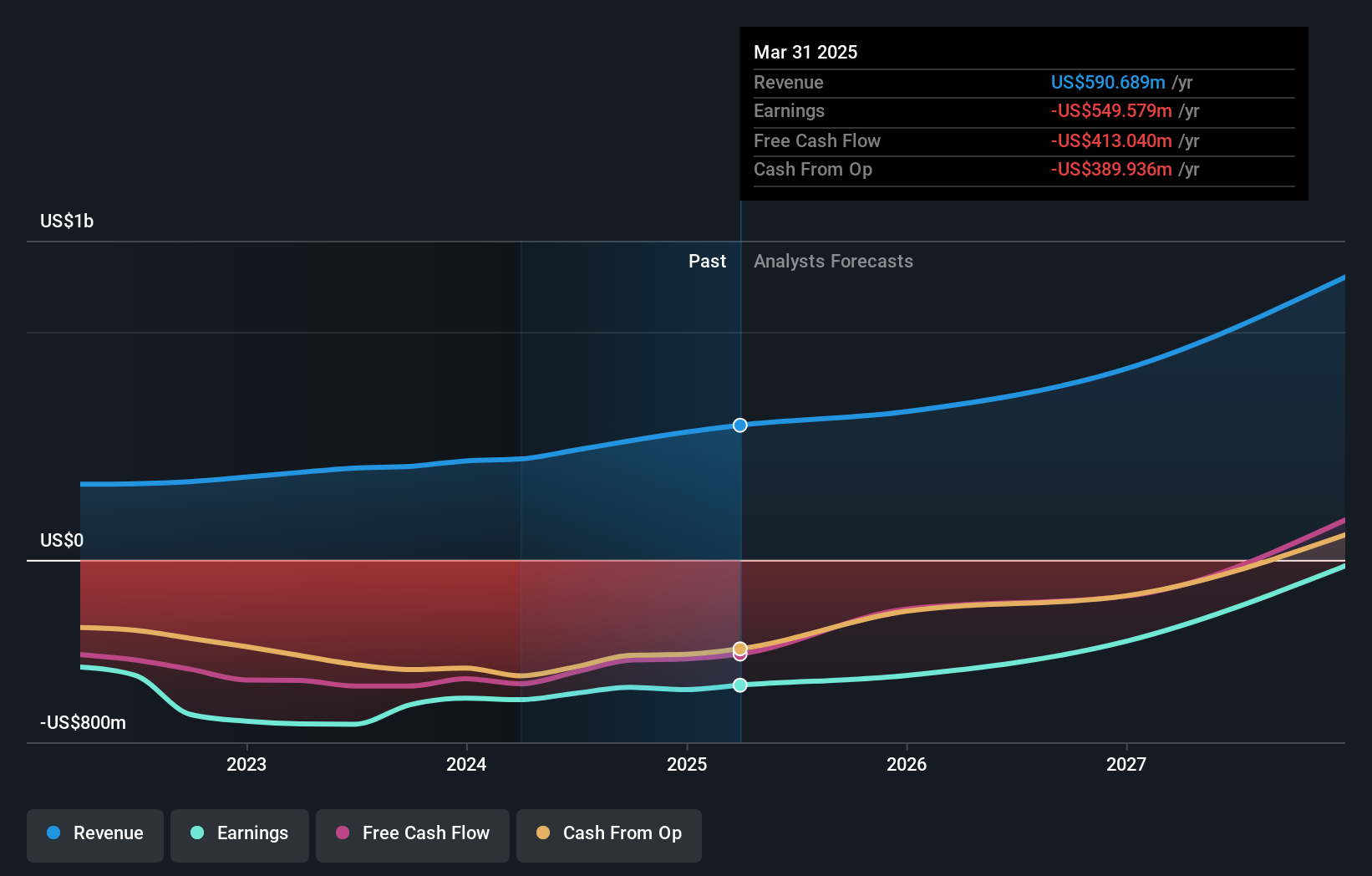

- ⚠️ Ongoing net losses of US$129 million in Q4 2025 and US$575 million for the full year keep funding needs and potential dilution on the table if revenue growth or cost controls fall short.

- ⚠️ Multiple shareholder class actions tied to the setrusumab trials add legal and reputational risk, and could distract management at a time when regulatory execution on UX111 and other programs is critical.

- 🎁 Revenue reached US$673 million for 2025, with management guiding to US$730 million to US$760 million for 2026, which, if achieved, would support the view that the existing commercial portfolio can carry more of the financial load.

- 🎁 Positive long term UX111 data and the resubmitted FDA application provide a potential new gene therapy revenue stream if approved, which could help support Ultragenyx’s focus on rare disease treatments alongside competitors such as Biomarin and Vertex.

What To Watch Going Forward

From here, it is worth watching three things in particular. First, how the class action lawsuits progress and whether any new disclosures emerge that change your view of management’s judgment. Second, whether Ultragenyx sticks to its expense reduction plans while still supporting key programs like UX111, DTX401 and GTX-102, and how that shows up in quarterly loss trends. Third, regulatory milestones for UX111, including the FDA review through the expected 2026 decision window, as well as any updates to 2026 revenue guidance. Taken together, these will help you judge whether the company is moving closer to its stated profitability target while managing its legal and clinical risks.

To ensure you're always in the loop on how the latest news impacts the investment narrative for Ultragenyx Pharmaceutical, head to the community page for Ultragenyx Pharmaceutical to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.