Uncovering 3 Undiscovered Gems in the US Market

Anbio Biotechnology NNNN | 0.00 |

Over the last 7 days, the United States market has remained flat, yet it has risen by 24% over the past year with earnings expected to grow by 17% per annum in the coming years. In this dynamic environment, identifying stocks that are not only poised for growth but also remain underappreciated can be key to uncovering potential opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 69.86% | 1.25% | -3.09% | ★★★★★★ |

| Security Federal | 18.41% | 5.46% | -0.53% | ★★★★★★ |

| Tri-County Financial Group | 54.21% | -0.70% | -10.52% | ★★★★★★ |

| Southern Michigan Bancorp | 108.80% | 7.38% | 0.84% | ★★★★★★ |

| Oakworth Capital | 51.38% | 15.89% | 14.04% | ★★★★★★ |

| Teekay | 2.14% | 10.67% | 57.58% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.26% | 11.00% | ★★★★★★ |

| NameSilo Technologies | 3.13% | 14.25% | 15.06% | ★★★★★☆ |

| Union Bankshares | 406.25% | 1.42% | -7.24% | ★★★★☆☆ |

| High Templar Tech | 13.55% | -66.76% | -26.62% | ★★★★☆☆ |

We'll examine a selection from our screener results.

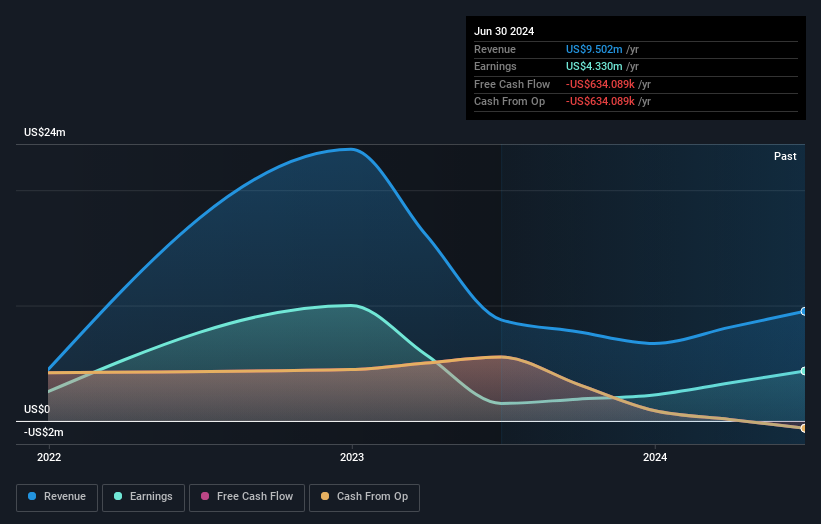

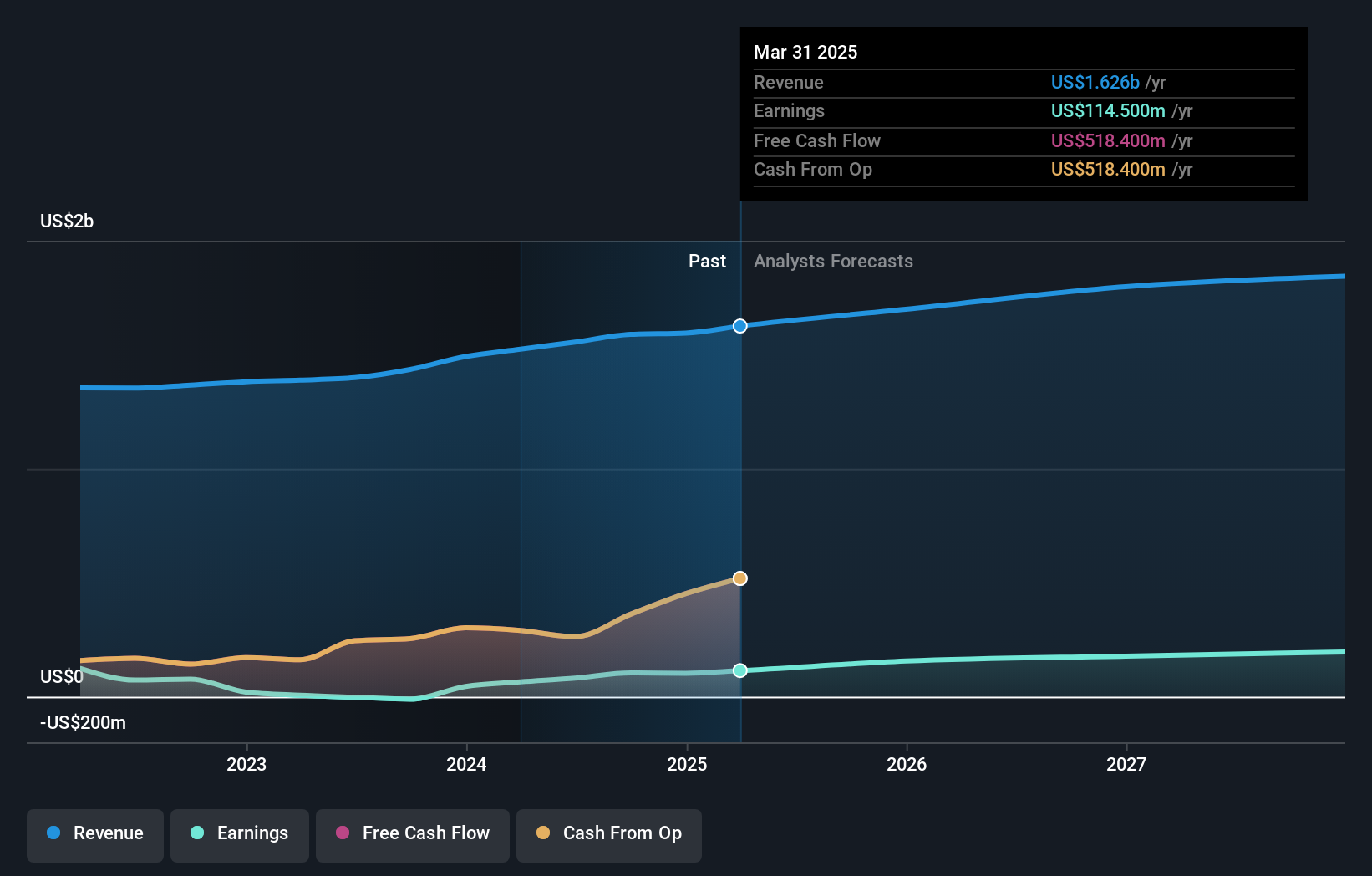

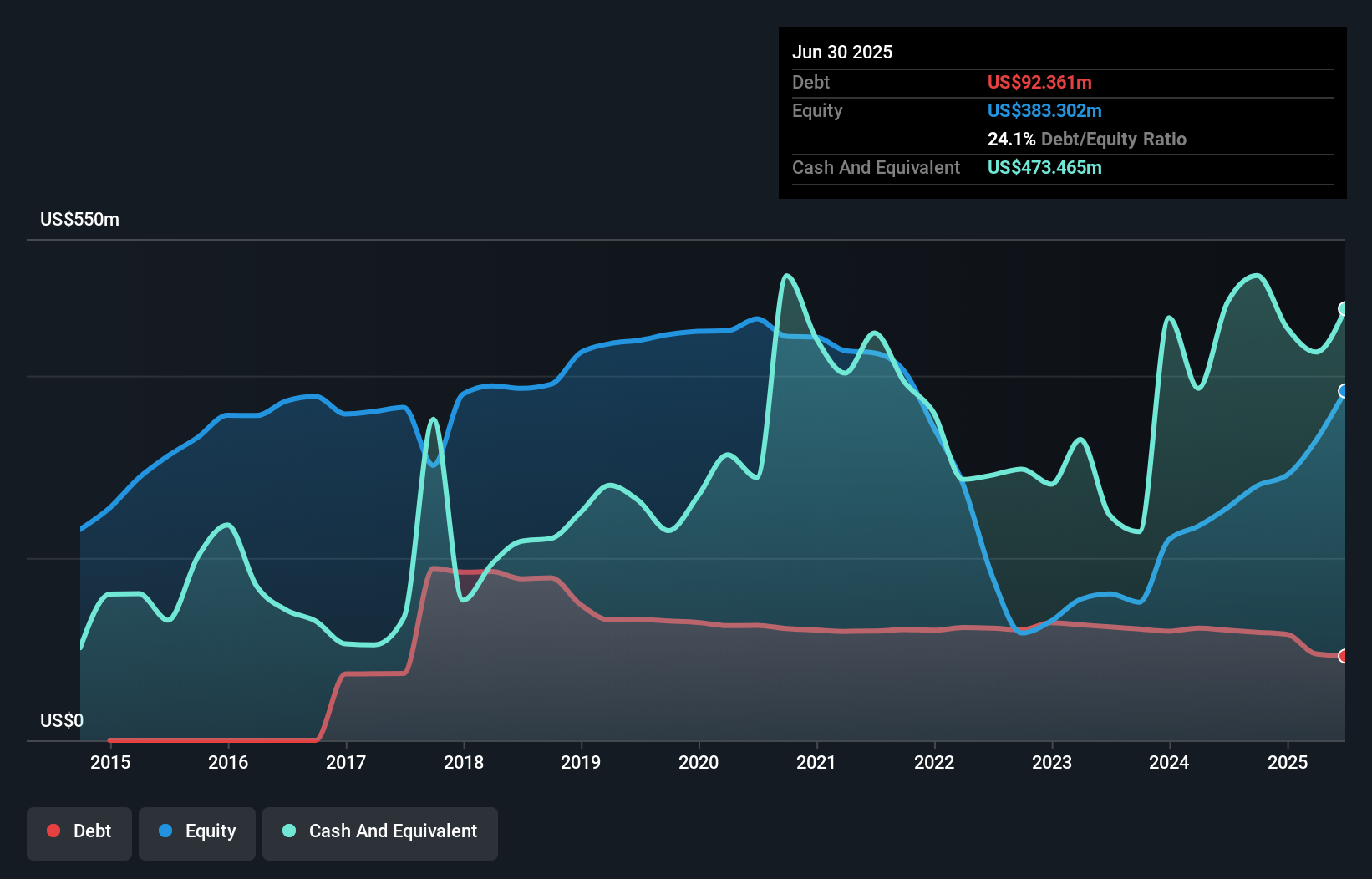

Anbio Biotechnology (NNNN)

Simply Wall St Value Rating: ★★★★★★

Overview: Anbio Biotechnology is a company that specializes in providing in vitro diagnostics (IVD) products globally, with a market capitalization of approximately $1.18 billion.

Operations: Anbio generates revenue primarily from its Surgical & Medical Equipment segment, amounting to $8.65 million. The company's financials reflect a focus on this core segment, contributing significantly to its overall market presence.

Anbio Biotechnology, a small player in the biotech sector, has shown impressive earnings growth of 169.9% over the past year, outpacing the industry's 43%. With no debt for five years and strong net income of US$6.4 million in 2025 compared to US$2.37 million in 2024, financial stability seems robust. Despite a decline in earnings by an average of 3.4% annually over five years, recent performance indicates potential upside. A special shareholders meeting on May 15 aims to amend company bylaws and enhance share capital structure, signaling strategic shifts that could impact future growth dynamics positively or negatively.

Horace Mann Educators (HMN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Horace Mann Educators Corporation operates as an insurance holding company in the United States, with a market capitalization of approximately $1.82 billion.

Operations: The company generates revenue through its primary segments: Property & Casualty ($877 million), Life & Retirement ($552.50 million), and Supplemental & Group Benefits ($305.70 million).

Horace Mann Educators, focusing on the educator community, has shown promising growth with a 44% earnings increase over the past year, outpacing the insurance industry's 36%. The company trades at a price-to-earnings ratio of 11x, which is favorable compared to the US market's 18.4x. With its interest payments well-covered by EBIT at 6.5 times and a satisfactory net debt to equity ratio of 33.8%, it demonstrates financial stability. Recent share buybacks amounted to $6.84 million for nearly 154,000 shares, reflecting strategic capital management despite insider selling in recent months.

Heritage Insurance Holdings (HRTG)

Simply Wall St Value Rating: ★★★★★☆

Overview: Heritage Insurance Holdings, Inc. operates through its subsidiaries to offer personal and commercial residential insurance products, with a market capitalization of approximately $690.92 million.

Operations: The company generates revenue primarily from residential property insurance, amounting to $848.47 million.

Heritage Insurance Holdings has demonstrated impressive financial resilience, with a debt to equity ratio cut from 28% to 14.9% over the last five years, indicating reduced leverage. The firm’s earnings skyrocketed by 159% in the past year, significantly outpacing the insurance industry's average growth of 36%. Despite trading at nearly 80% below its estimated fair value, Heritage's net income for Q1 rose to $36.48 million from $30.47 million a year prior, and it repurchased shares worth $3 million recently. However, future earnings are expected to decline annually by an average of 21%, posing potential challenges ahead.

Key Takeaways

- Reveal the 340 hidden gems among our US Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.