Uncovering Middle East's Hidden Gems Including Gulf Medical Projects Company (PJSC) And Two More Small Caps

Alamar 6014.SA | 41.60 | -0.48% |

As Gulf markets show resilience with most indices gaining ahead of earnings, the Middle East continues to capture investor interest, particularly in small-cap stocks. With Dubai's main share index reaching its strongest level in almost two decades and a cautious sentiment prevailing due to oil price volatility, now is an opportune moment to explore lesser-known opportunities such as Gulf Medical Projects Company (PJSC) and other promising small caps that may benefit from strong fundamentals and growth expectations.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sure Global Tech | NA | 10.11% | 15.42% | ★★★★★★ |

| Baazeem Trading | 10.02% | -1.27% | -1.66% | ★★★★★★ |

| Qassim Cement | NA | 4.02% | -11.40% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | 3.26% | 17.17% | 23.30% | ★★★★★★ |

| MOBI Industry | 13.81% | 5.67% | 19.69% | ★★★★★★ |

| Najran Cement | 14.49% | -4.20% | -30.16% | ★★★★★★ |

| Amanat Holdings PJSC | 10.86% | 27.51% | -0.92% | ★★★★★☆ |

| Etihad GO Telecom | 0.85% | 38.36% | 57.78% | ★★★★★☆ |

| Space42 | 17.28% | 37.30% | 24.29% | ★★★★★☆ |

| Ajman Bank PJSC | 53.89% | 16.11% | 18.02% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

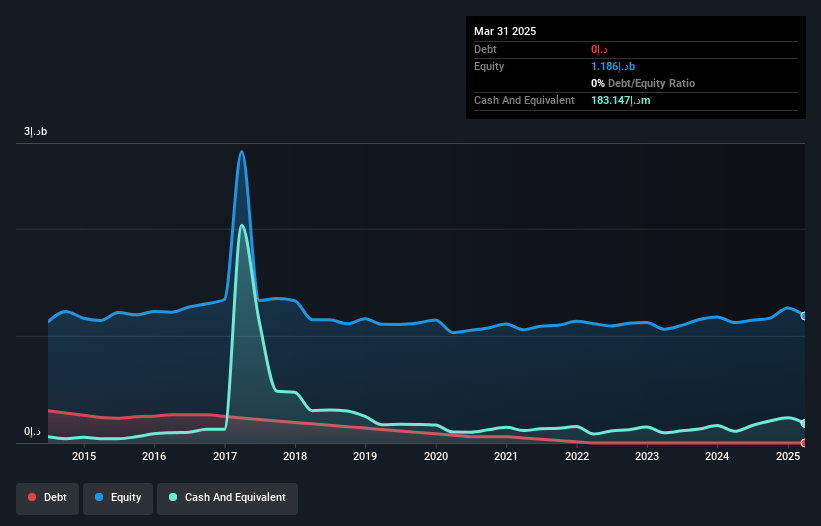

Gulf Medical Projects Company (PJSC) (ADX:GMPC)

Simply Wall St Value Rating: ★★★★★★

Overview: Gulf Medical Projects Company (PJSC) operates hospitals in the United Arab Emirates and has a market capitalization of AED1.36 billion.

Operations: Gulf Medical Projects Company derives its revenue primarily from health services, contributing AED742.09 million, with investments adding AED59.18 million. The company's financial performance is significantly driven by its health services segment, which forms the bulk of its income stream.

Gulf Medical Projects Company, a nimble player in the healthcare sector, has demonstrated robust growth with earnings surging by 71.6% over the past year, significantly outpacing the industry's 4.2%. The company is trading at a compelling value, approximately 55.7% below its estimated fair value. Despite a notable AED28.6 million one-off gain impacting recent financial results, GMPC remains debt-free and continues to generate positive free cash flow. Recent performance highlights include Q3 sales of AED188 million and net income of AED20.86 million, reflecting strong operational momentum compared to last year's figures.

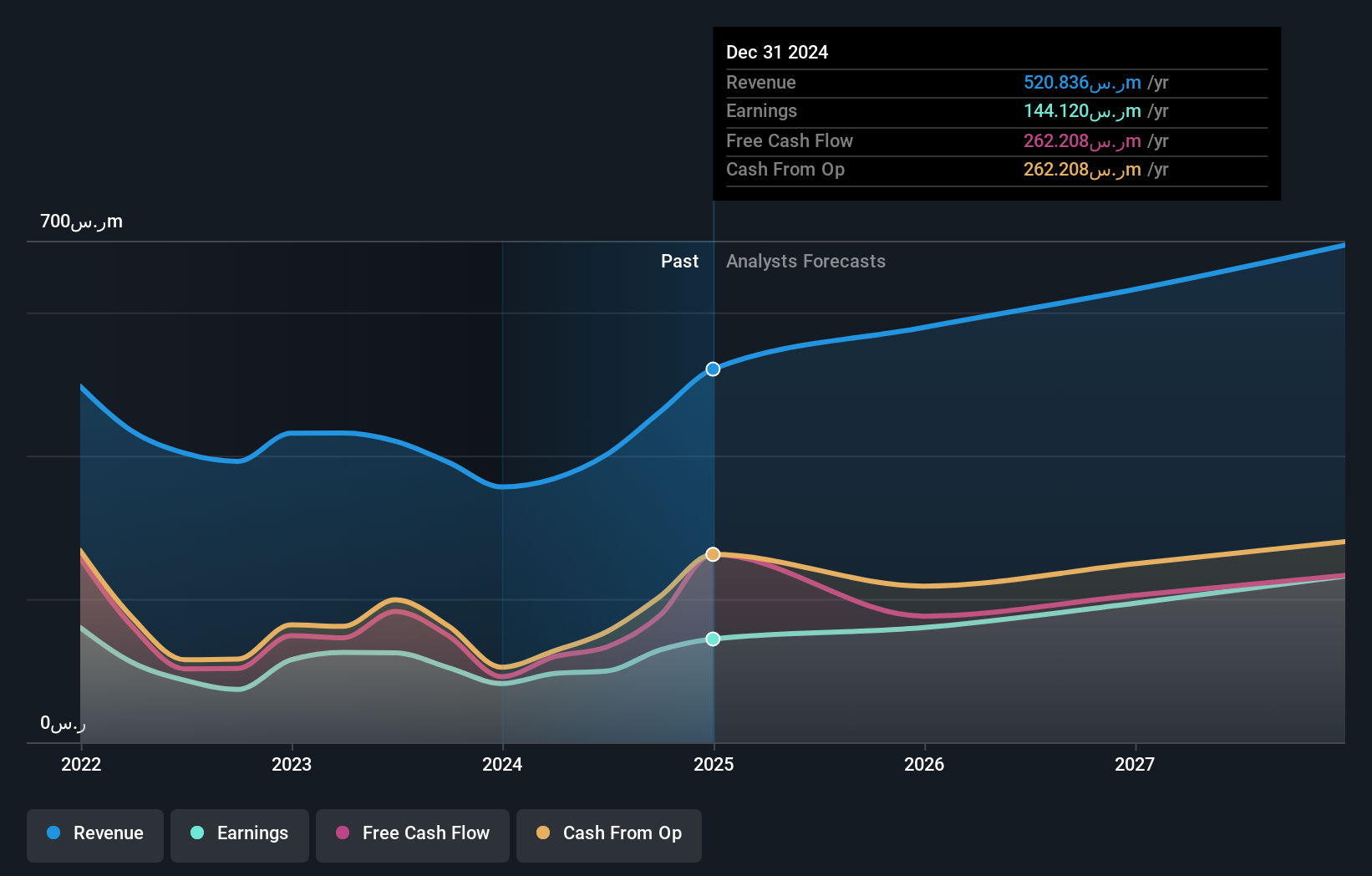

City Cement (SASE:3003)

Simply Wall St Value Rating: ★★★★★★

Overview: City Cement Company, along with its subsidiaries, is engaged in the manufacturing and sale of cement within Saudi Arabia, with a market capitalization of SAR1.87 billion.

Operations: The company generates revenue primarily from the sale of cement in Saudi Arabia. Its financial performance includes a market capitalization of SAR1.87 billion.

City Cement, a smaller player in the Middle East cement industry, is currently trading at 62.8% below its estimated fair value, suggesting potential undervaluation. The company boasts high-quality earnings and remains debt-free, eliminating concerns over interest payments. Over the past year, City Cement's earnings grew by 7%, outpacing the Basic Materials industry's -4.2% performance. However, recent results show a mixed picture: third-quarter sales dropped to SAR 96.49 million from SAR 130.11 million last year, while net income fell to SAR 8.75 million from SAR 33.66 million in the same period last year despite positive free cash flow trends continuing this quarter.

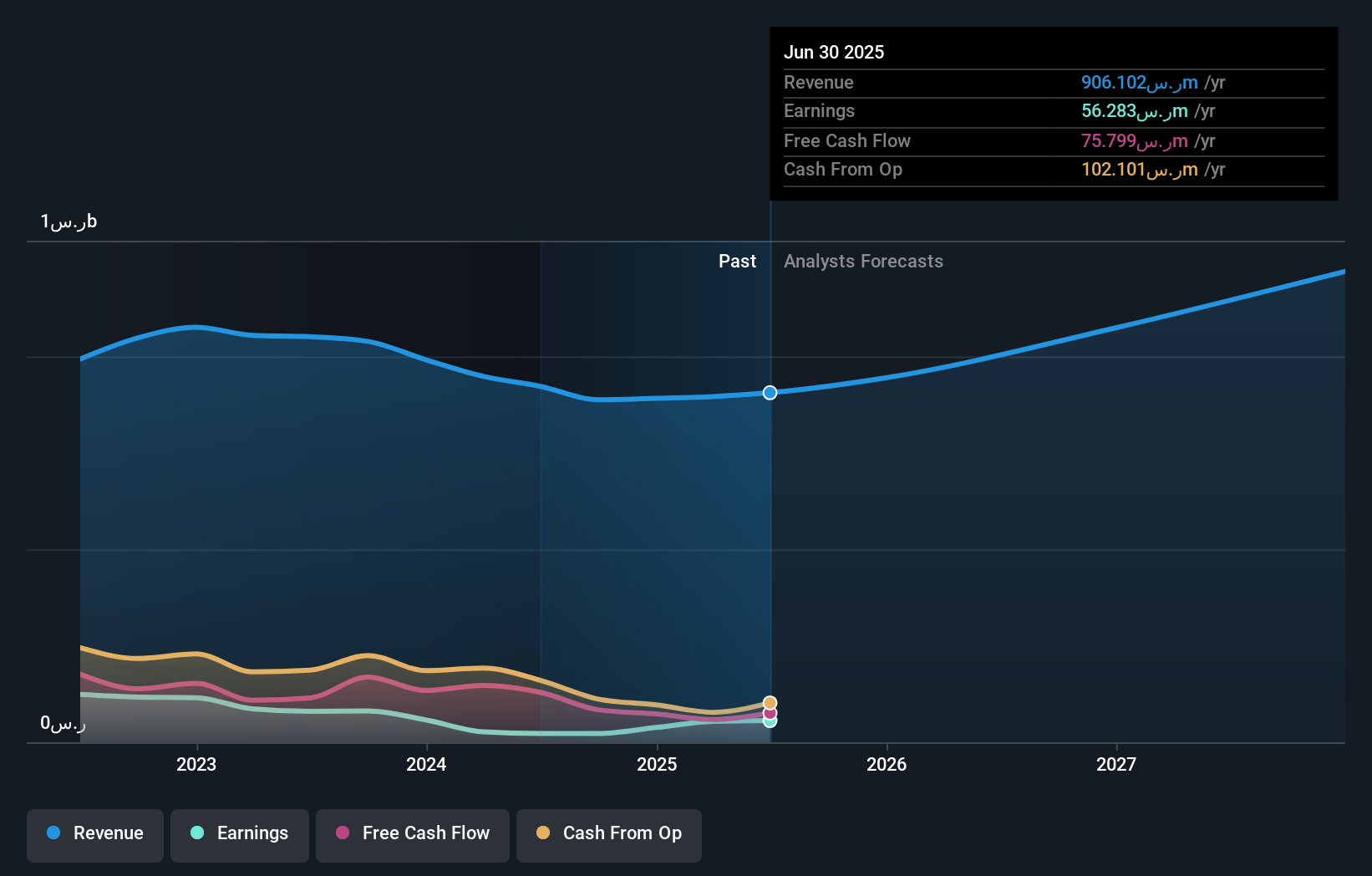

Alamar Foods (SASE:6014)

Simply Wall St Value Rating: ★★★★★☆

Overview: Alamar Foods Company, with a market cap of SAR1.08 billion, operates and manages quick service restaurants across the Middle East, North Africa, and Pakistan.

Operations: The company generates revenue primarily from its operations in the Kingdom of Saudi Arabia (SAR608.96 million) and Other GCC and Levant regions (SAR226.19 million), with additional contributions from North Africa (SAR101.22 million). Internal Revenue is reported as a negative figure, indicating potential intercompany eliminations or adjustments.

Alamar Foods, a notable player in the Middle East's hospitality sector, has demonstrated robust earnings growth of 126.5% over the past year, outpacing the industry average of 9.1%. The company's price-to-earnings ratio stands at 20.8x, slightly below the industry benchmark of 21.3x, suggesting potential value for investors. Despite a challenging five-year period with earnings declining by an average of 24.2% annually, Alamar remains profitable with well-covered interest payments (14.7x EBIT coverage). Recent financials reveal third-quarter sales increased to SAR 236.67 million from SAR 229.02 million last year; however, net income dipped to SAR 15.66 million from SAR 20.28 million previously reported due to rising operational costs and strategic investments like their Five Guys KSA acquisition discussions in early January this year.

Taking Advantage

- Delve into our full catalog of 188 Middle Eastern Undiscovered Gems With Strong Fundamentals here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.