Under Armour (UAA): A Fresh Look at Valuation After Recent Share Price Moves

Under Armour, Inc. Class A UAA | 5.54 | -3.74% |

Under Armour (UAA) shares have seen mixed returns recently, falling around 1% over the past day but ticking up over the past week. The company’s stock still sits well below where it started the year, which highlights ongoing investor caution.

Under Armour’s latest share price, hovering at $4.81, reflects the continued impact of a tough year. Its 90-day share price return of -34.65% and 12-month total shareholder return of -44.26% make clear that momentum has been fading, despite some recent positive session moves. Investors appear cautious, weighing short-term volatility against an ongoing struggle to regain long-term traction.

If Under Armour’s story has you thinking bigger, it’s the perfect time to broaden your search and discover fast growing stocks with high insider ownership

The question now is whether Under Armour’s current valuation signals an opportunity for investors to buy in at a discount, or if the challenges ahead are already fully reflected in the stock price.

Most Popular Narrative: 22% Undervalued

Under Armour's most widely followed narrative on fair value highlights a significant gap compared to the recent closing price of $4.81, suggesting possible upside. However, this valuation is influenced by substantial business transformation efforts and evolving forecasts that inform analyst consensus.

The ongoing transformation to a brand-first strategy, with a focus on premiumization, more selective SKU assortments, and enhanced brand storytelling, positions Under Armour to increase average selling prices, improve full-price sell-through, and reduce reliance on discounting. These efforts are expected to have a positive impact on net margins and long-term earnings growth.

Want to see what really drives this bullish valuation? The fair value relies on ambitious growth targets, margin recovery, and a profit outlook that may surprise some investors. For those interested in the specific financial factors behind this narrative’s positive case, the full story contains the essential details investors are discussing.

Result: Fair Value of $6.17 (UNDERVALUED)

However, persistent margin pressures from tariffs and weak demand in key regions could quickly undermine the optimistic outlook for Under Armour’s recovery.

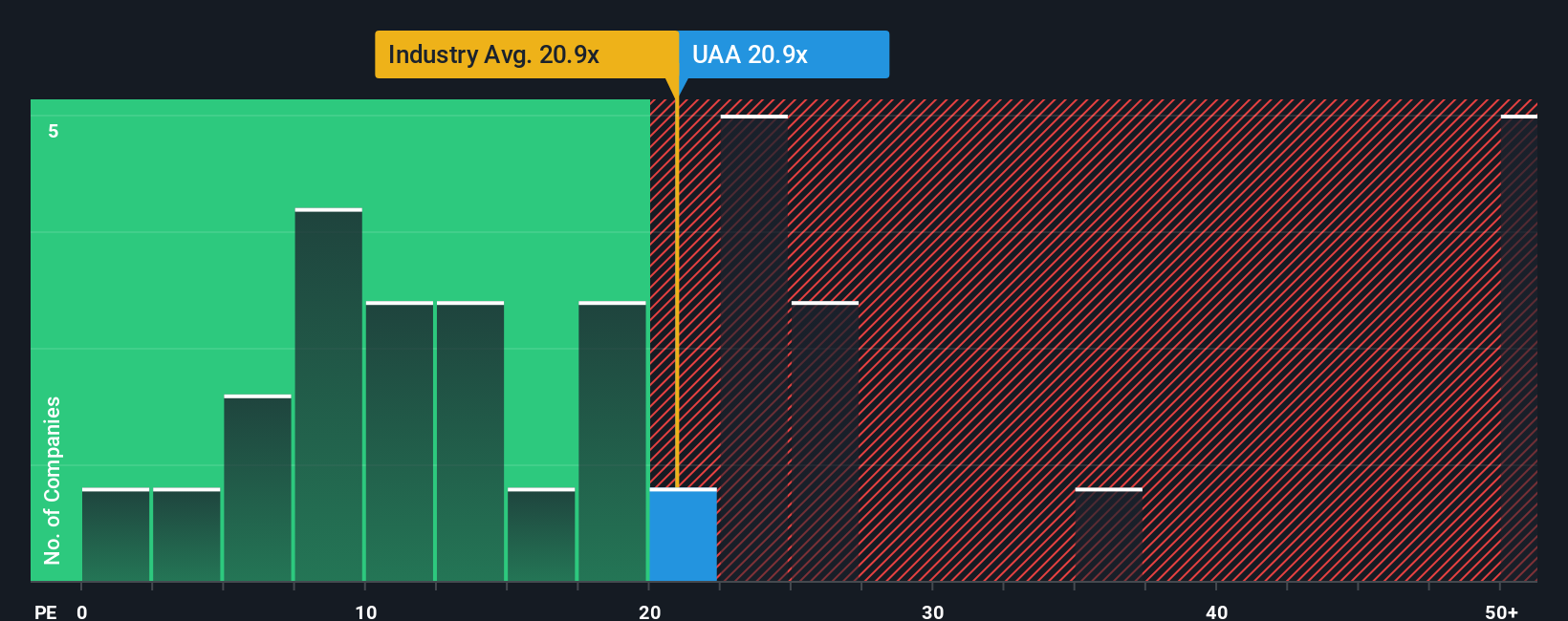

Another View: Market Ratio Perspective

Looking at Under Armour through the lens of its price-to-earnings ratio tells a different story. The company trades at 20.3x earnings, making it more expensive than both the US Luxury industry average of 19.7x and the peer group average of 15.1x. This compares with a fair ratio of 25.5x, the level the market could shift toward if sentiment improves. For investors, is this a sign of overvaluation, or could market sentiment catch up to justify the higher price?

Build Your Own Under Armour Narrative

If you’d rather trust your own research or want to see the numbers firsthand, you can craft a custom view in just a few minutes. Do it your way

A great starting point for your Under Armour research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t settle for just one opportunity when you can access a world of smart investment ideas at your fingertips. Make your next move with confidence; missing out could mean missing the next big winner.

- Capture untapped potential by checking out these 881 undervalued stocks based on cash flows that are trading below their intrinsic worth before the crowd catches on.

- Boost your portfolio’s earning power by targeting steady income opportunities; scan these 17 dividend stocks with yields > 3% offering yields above 3%.

- Capitalize on transformational technology trends and get ahead of the curve by looking into these 27 AI penny stocks shaping the future of artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.