Undervalued Small Caps With Insider Action Across Regions In February 2026

Herbalife Nutrition Ltd. HLF | 13.89 | -3.47% |

In January 2026, the U.S. stock market saw mixed performances with the S&P 500 and Dow Jones Industrial Average posting gains despite a sluggish end to the month, while small-cap indices like the S&P 600 experienced varying pressures from economic indicators such as interest rates and commodity price fluctuations. In this environment, identifying promising small-cap stocks often involves looking for those with strong fundamentals and potential growth catalysts that can navigate broader market uncertainties.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Peoples Bancorp | 10.7x | 2.7x | 43.55% | ★★★★★☆ |

| First United | 10.0x | 3.0x | 44.21% | ★★★★★☆ |

| Wolverine World Wide | 16.7x | 0.8x | 34.81% | ★★★★★☆ |

| UMH Properties | 204.9x | 5.2x | 47.04% | ★★★★☆☆ |

| Community Bancorp | 10.2x | 3.6x | 36.67% | ★★★★☆☆ |

| New Peoples Bankshares | 9.7x | 2.2x | 39.59% | ★★★☆☆☆ |

| Union Bankshares | 10.1x | 2.2x | 19.79% | ★★★☆☆☆ |

| Angel Oak Mortgage REIT | 12.8x | 6.4x | 37.06% | ★★★☆☆☆ |

| Dave & Buster's Entertainment | 2169.8x | 0.3x | -8196.19% | ★★★☆☆☆ |

| Vestis | NA | 0.3x | -8.18% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

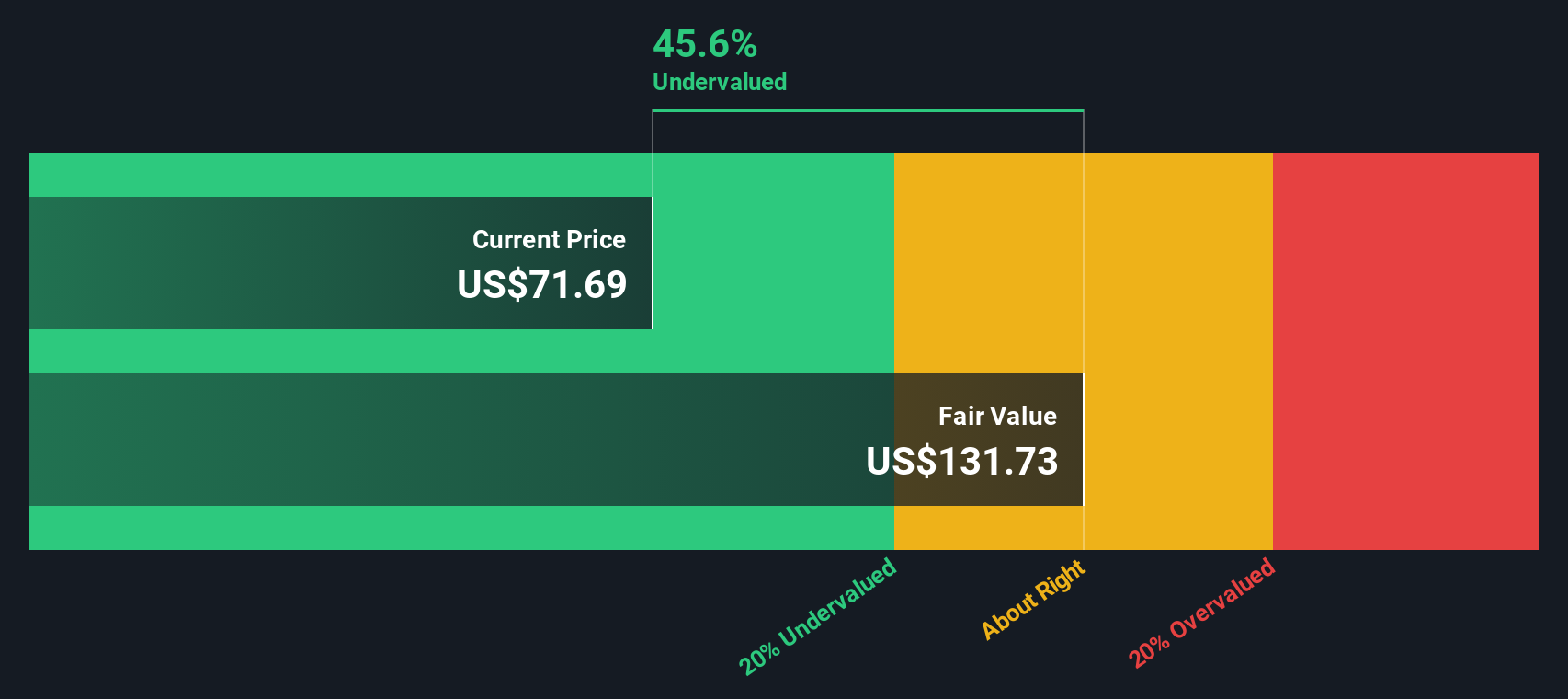

Tompkins Financial (TMP)

Simply Wall St Value Rating: ★★★★★☆

Overview: Tompkins Financial is a financial services company providing banking, insurance, and wealth management services with a market cap of approximately $1.02 billion.

Operations: Tompkins Financial's revenue is generated entirely from its gross profit, which consistently matches its reported revenue figures. The company has experienced fluctuations in net income margin, with a notable high of 37.02% and a recent low of 3.29%. Operating expenses are significant, with general and administrative expenses forming the largest portion, reaching up to $155.96 million in recent periods.

PE: 7.1x

Tompkins Financial, a smaller company in the U.S. market, recently showcased strong financial performance with fourth-quarter net income soaring to US$96.25 million from last year's US$19.66 million and basic earnings per share at US$6.74 up from US$1.38. Insider confidence is evident as they purchased shares between October and December 2025, while the company completed a buyback of 22,339 shares for US$1.6 million during this period. However, future earnings are projected to decline by an average of 18.5% annually over the next three years, presenting potential challenges ahead despite recent successes.

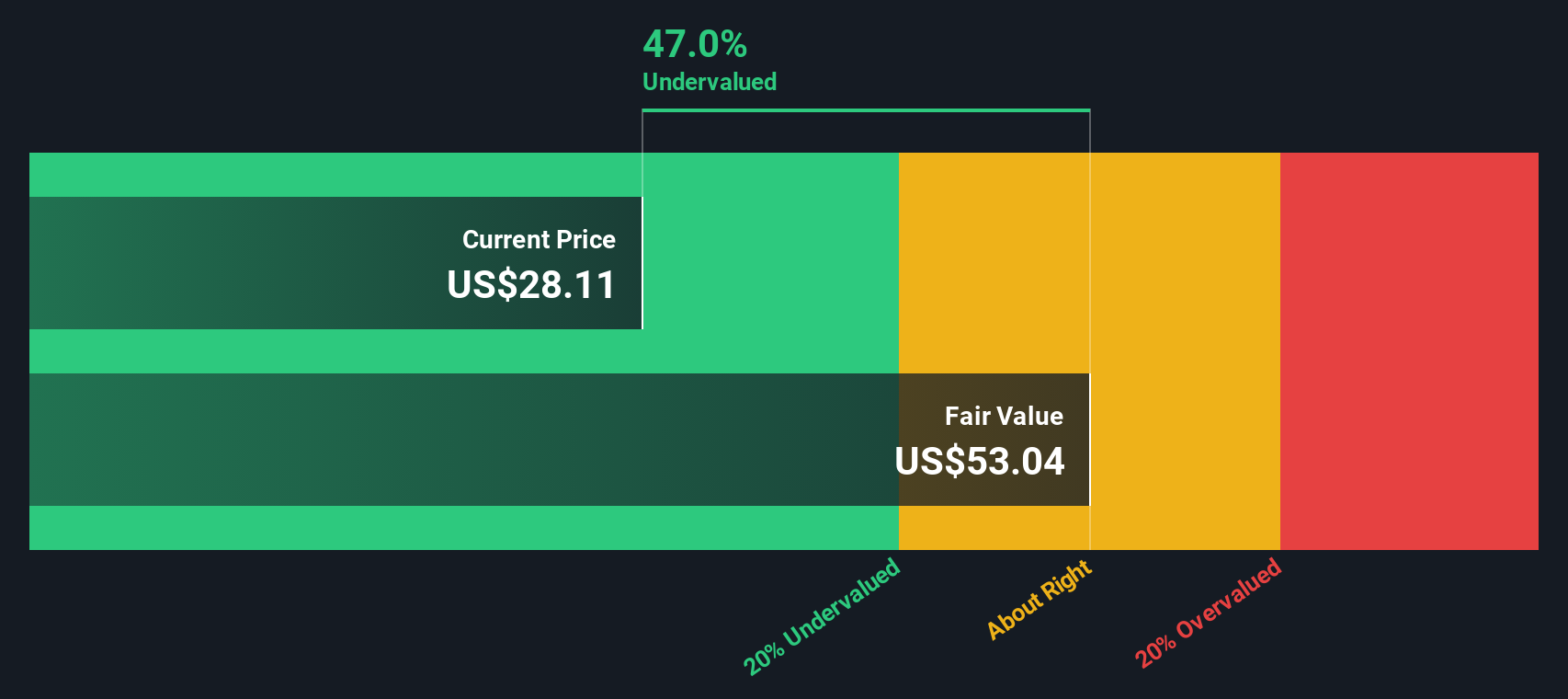

Byline Bancorp (BY)

Simply Wall St Value Rating: ★★★★★☆

Overview: Byline Bancorp operates as a bank holding company providing a range of banking products and services, with a market capitalization of approximately $0.81 billion.

Operations: Byline Bancorp generates revenue primarily from its banking operations, with a recent figure of $409.98 million. Operating expenses are significant, including general and administrative costs of $204.14 million for the latest period. The company's net income margin has shown variability, reaching 31.72% in the most recent quarter while maintaining a gross profit margin at 100% over multiple periods.

PE: 11.2x

Byline Bancorp, a small cap financial institution, showcases its potential through recent financial performance and strategic actions. The company reported a rise in net interest income to US$101.26 million for Q4 2025 from US$88.52 million the previous year, alongside increased net income of US$34.52 million. A dividend hike of 20% reflects confidence in future earnings, while insider confidence is evident with share repurchases totaling US$23.73 million by December 2025 under their buyback program initiated in late 2024. Earnings are projected to grow at an annual rate of 5%, suggesting continued value for investors seeking growth opportunities within this sector.

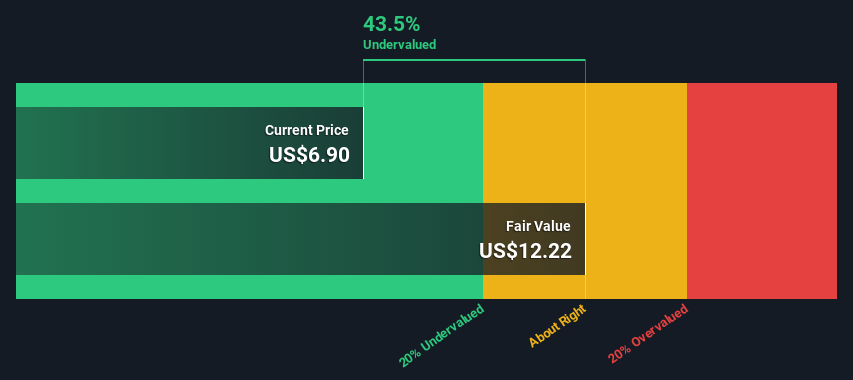

Herbalife (HLF)

Simply Wall St Value Rating: ★★★★★☆

Overview: Herbalife is a global nutrition company that develops and sells dietary supplements and personal care products, with a market presence across various countries including significant operations in the United States, China, India, and Mexico.

Operations: Herbalife generates revenue primarily from regions like India and the United States, with significant contributions also coming from Mexico and China. The company's cost of goods sold (COGS) has been a major expense, influencing its gross profit margin, which was 44.38% in the latest period. Operating expenses have consistently included substantial general and administrative costs. Over recent periods, net income margins have shown variability but were at 6.46% in the most recent quarter available for analysis.

PE: 5.6x

Herbalife, a smaller company in the United States, faces challenges with external borrowing as its sole funding source. Despite this, insider confidence is evident with purchases made from November 2025 to January 2026. Their Liftoff energy line expansion taps into the growing US$41.4 billion energy drink market by 2033, leveraging their network of over 10,000 nutrition clubs. Recent earnings showed mixed results: third-quarter sales rose to US$1.27 billion while net income slightly dipped to US$43 million compared to last year.

Taking Advantage

- Get an in-depth perspective on all 84 Undervalued US Small Caps With Insider Buying by using our screener here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.