Undervalued Small Caps With Insider Action To Explore In February 2026

Wendy's Company WEN | 6.88 | -0.29% |

As February 2026 begins, the U.S. stock market has kicked off the month with a strong performance, highlighted by significant gains in major indices such as the Dow Jones Industrial Average and S&P 500. Amidst this positive momentum, small-cap stocks are drawing attention due to their potential for growth and unique opportunities presented by current economic conditions. In this environment, identifying promising investments often involves looking at companies with solid fundamentals and potential catalysts like insider action that could drive future performance.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Peoples Bancorp | 11.1x | 2.8x | 42.50% | ★★★★★☆ |

| Bank of the James Financial Group | 10.6x | 2.0x | 47.21% | ★★★★☆☆ |

| Wolverine World Wide | 17.0x | 0.8x | 41.55% | ★★★★☆☆ |

| Union Bankshares | 10.2x | 2.2x | 20.84% | ★★★★☆☆ |

| Auburn National Bancorporation | 12.2x | 2.7x | 22.06% | ★★★☆☆☆ |

| J&J Snack Foods | 26.2x | 1.0x | 33.36% | ★★★☆☆☆ |

| New Peoples Bankshares | 9.1x | 2.1x | 43.28% | ★★★☆☆☆ |

| Community Bancorp | 10.7x | 3.8x | 36.03% | ★★★☆☆☆ |

| Angel Oak Mortgage REIT | 12.5x | 6.3x | 39.73% | ★★★☆☆☆ |

| Vestis | NA | 0.3x | -7.24% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

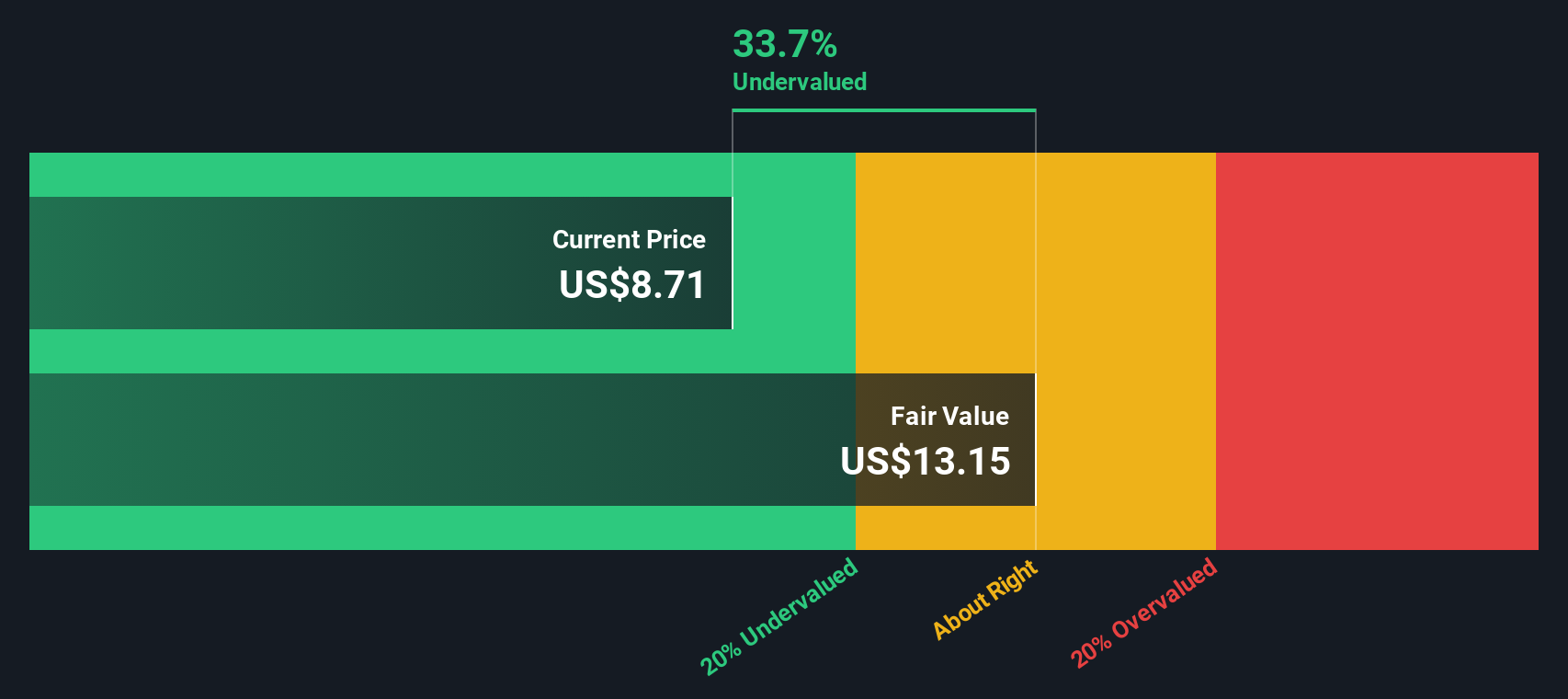

Karat Packaging (KRT)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Karat Packaging is engaged in the manufacturing and supply of a broad portfolio of single-use products, with a market capitalization of approximately $0.36 billion.

Operations: The company's revenue primarily comes from the manufacturing and supply of single-use products, with recent figures reaching $453.78 million. Over time, the gross profit margin has shown an upward trend, peaking at 39.18% in June 2025 before slightly decreasing to 38.04% by September 2025. Operating expenses have consistently increased, impacting net income margins which reached a high of 8.22% in September 2023 but later adjusted to around 6.67%.

PE: 17.0x

Karat Packaging, a small U.S. company, shows potential with forecasted annual earnings growth of 10.28%. Despite relying entirely on external borrowing for funding, they demonstrate insider confidence through recent share purchases. In the third quarter of 2025, sales rose to US$124.52 million from US$112.77 million a year ago, though net income dipped slightly to US$7.33 million from US$9.09 million previously. Looking ahead, Karat expects fourth-quarter sales to increase by up to 14%.

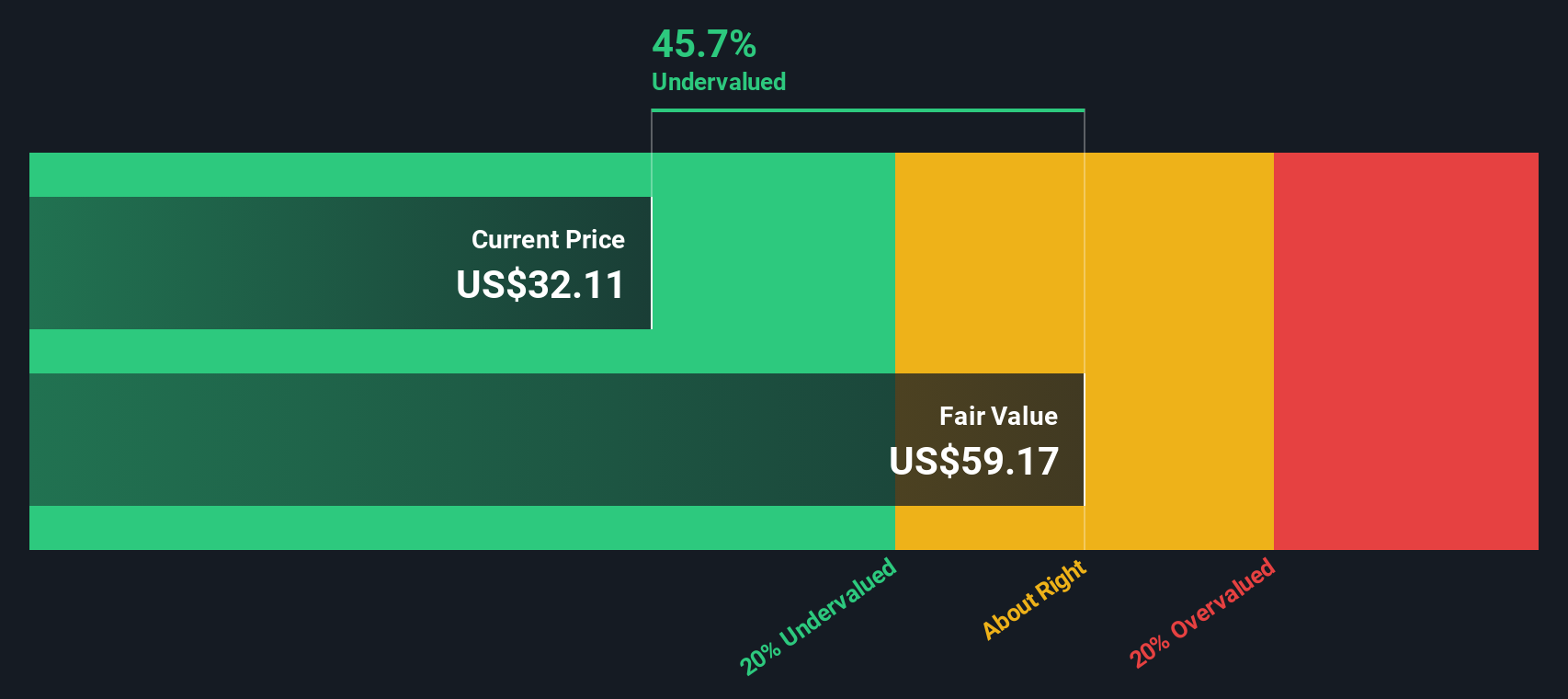

Wendy's (WEN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Wendy's operates as a global fast-food restaurant chain, focusing on hamburgers and related food products, with a market cap of approximately $4.17 billion.

Operations: The company generates revenue primarily from its U.S. operations, with significant contributions from international markets and real estate development. Over the observed periods, gross profit margin has shown a notable upward trend, reaching 49.14% by the end of 2017 before stabilizing around the mid-30s in subsequent years. Operating expenses have consistently been a substantial part of costs, with general and administrative expenses being a key component within this category.

PE: 8.2x

Wendy's, a notable player in the fast-food industry, has introduced a new Biggie Deals® value menu with price points at US$4, US$6, and US$8 to attract budget-conscious consumers. Despite external borrowing as its sole funding source posing higher risk, insider confidence is evident through share repurchases totaling 27.77 million shares for US$465.65 million since January 2023. Recent earnings showed slight declines in revenue and net income compared to last year but maintained consistent dividends of US$0.14 per share for December 2025.

Global Medical REIT (GMRE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Global Medical REIT is a real estate investment trust that focuses on acquiring and managing healthcare facilities, with a market capitalization of $0.82 billion.

Operations: The company generates revenue primarily from investing in medical properties, with recent figures reaching $144.83 million. Gross profit margins have shown a notable trend, consistently hovering around 99% in recent periods, indicating efficient cost management relative to revenue. Operating expenses and non-operating expenses are significant cost components, with general and administrative expenses being a major part of the operating costs.

PE: -148.1x

Global Medical REIT, a smaller player in the healthcare real estate sector, faces financial challenges with interest payments not well covered by earnings. Despite this, earnings are expected to grow 88% annually. Recent insider confidence is evident as management has been purchasing shares over the past year. The company declared dividends on both common and preferred stocks for late 2025 and early 2026. Leadership changes include director retirements without internal conflicts reported.

Taking Advantage

- Gain an insight into the universe of 71 Undervalued US Small Caps With Insider Buying by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.