Undervalued Small Caps With Insider Activity In February 2026

Wolverine World Wide, Inc. WWW | 15.95 | -2.63% |

As February 2026 unfolds, the U.S. stock market is experiencing a surge with major indices like the Dow Jones and S&P 500 starting the month on a high note, driven by positive economic indicators such as expanding factory activity and new trade agreements. In this dynamic environment, small-cap stocks present intriguing opportunities for investors seeking value; particularly those that show signs of insider activity which can often indicate confidence in their future prospects amidst broader market optimism.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Cooper-Standard Holdings | 17.1x | 0.2x | 44.47% | ★★★★★★ |

| Peoples Bancorp | 10.8x | 2.7x | 43.46% | ★★★★★☆ |

| First United | 10.3x | 3.1x | 42.45% | ★★★★★☆ |

| Trinity Capital | 8.7x | 4.6x | 38.22% | ★★★★★☆ |

| CF Bankshares | 12.5x | 3.9x | 20.32% | ★★★★☆☆ |

| Wolverine World Wide | 17.1x | 0.8x | 38.16% | ★★★★☆☆ |

| New Peoples Bankshares | 9.7x | 2.2x | 39.59% | ★★★☆☆☆ |

| Union Bankshares | 10.1x | 2.2x | 19.94% | ★★★☆☆☆ |

| Angel Oak Mortgage REIT | 12.9x | 6.5x | 36.71% | ★★★☆☆☆ |

| Vestis | NA | 0.3x | -10.67% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

Mid Penn Bancorp (MPB)

Simply Wall St Value Rating: ★★☆☆☆☆

Overview: Mid Penn Bancorp operates as a financial institution providing banking and financial services to individuals, businesses, and institutional clients with a market capitalization of approximately $0.39 billion.

Operations: Mid Penn Bancorp generates revenue of $208.87 million primarily from banking and financial services to individuals, businesses, and institutional clients. The company's gross profit margin consistently stands at 100%, indicating that all reported revenue is retained as gross profit. Operating expenses are significant, with general and administrative expenses being a major component of these costs. Net income margin shows variability but has reached up to 32.78% in certain periods, reflecting the proportion of revenue converted into net income after operating expenses are accounted for.

PE: 15.6x

Mid Penn Bancorp, a smaller U.S. financial institution, has shown insider confidence with recent share purchases. The company reported strong fourth-quarter results, with net interest income rising to US$54.75 million and net income reaching US$19.45 million compared to the previous year. Despite challenges like recent auditor changes and minor charge-offs of US$466,000, they declared a regular dividend of US$0.22 and a special dividend of US$0.05 per share for February 2026 payouts, reflecting shareholder value commitment amidst growth prospects forecasted at 30.8% annually in earnings.

Amerant Bancorp (AMTB)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Amerant Bancorp operates as a bank holding company providing a range of financial services, with a focus on banking operations, and has a market capitalization of approximately $0.76 billion.

Operations: The company's revenue primarily stems from its banking operations, with a recent figure of $394.19 million. Over the observed periods, it has consistently reported a gross profit margin of 100%. Operating expenses have shown variability, with general and administrative expenses being a significant component, reaching $242.05 million in the latest period. Net income margins have fluctuated significantly over time, indicating varying levels of profitability amidst changing operating conditions.

PE: 16.9x

Amerant Bancorp, a smaller player in the U.S. banking sector, has shown signs of potential value with its recent financial performance. For 2025, net interest income rose to US$360.69 million from US$325.96 million the previous year, while net income rebounded to US$52.42 million from a loss of US$15.75 million in 2024. Insider confidence is evident as executives have been purchasing shares over recent months, indicating belief in future growth prospects despite challenges like a high bad loans ratio of 2.6%. The company completed significant share repurchases totaling 5.93% for US$45.49 million by the end of December 2025 and announced another buyback program up to US$40 million valid until December 31, 2026, reflecting strategic capital management amid ongoing leadership changes and operational shifts.

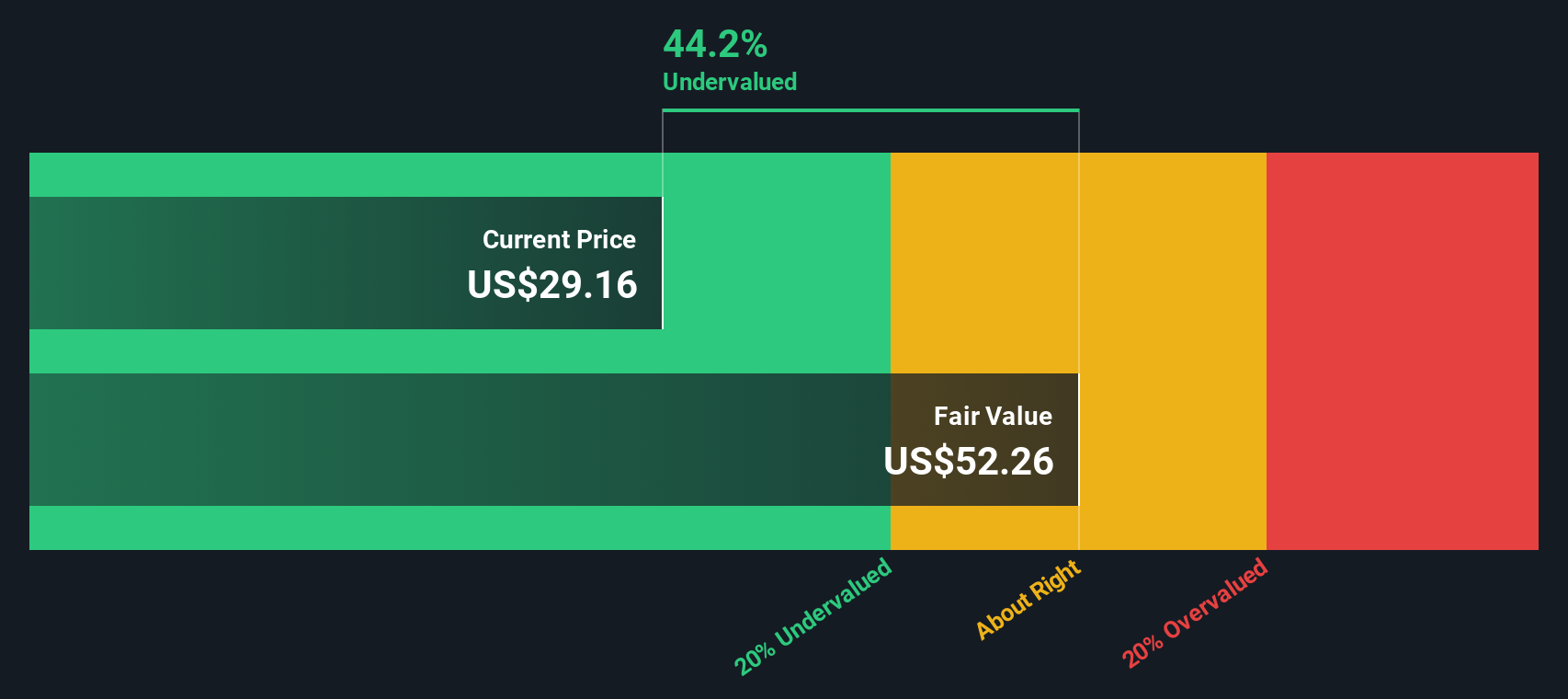

Wolverine World Wide (WWW)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Wolverine World Wide is a global footwear and apparel company that operates through segments including its Work Group and Active Group, with a market capitalization of approximately $1.95 billion.

Operations: The company's revenue is primarily driven by its Active Group, contributing significantly to the total, with Work Group also playing a notable role. Over recent periods, the gross profit margin has shown an increasing trend, reaching 46.58% in late 2025. Operating expenses have been substantial but are offset by reductions in non-operating expenses over time.

PE: 17.1x

Wolverine World Wide, a smaller player in the market, presents an intriguing opportunity with its shares perceived as undervalued. Insider confidence is evident as Independent Director DeMonty Price acquired 35,000 shares for US$535,500 in late 2025. Despite challenges like reliance on external debt and limited operating cash flow coverage, the company forecasts earnings growth of 18% annually. Recent leadership changes bring industry veterans to steer brands like Merrell and Saucony towards growth. Revenue projections for 2025 suggest modest gains with a focus on expanding key brands despite some segments facing declines.

Taking Advantage

- Unlock more gems! Our Undervalued US Small Caps With Insider Buying screener has unearthed 77 more companies for you to explore.Click here to unveil our expertly curated list of 80 Undervalued US Small Caps With Insider Buying.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.