Undervalued Small Caps With Insider Buying Across Regions

Similarweb Ltd. SMWB | 0.00 |

The United States market has experienced a flat week, yet it has shown a robust 27% increase over the past year, with earnings anticipated to grow by 17% annually in the coming years. In this context of growth and stability, identifying stocks that are currently undervalued can offer potential opportunities for investors seeking to capitalize on insider confidence and regional strengths.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| AVITA Medical | NA | 1.9x | 46.06% | ★★★★★☆ |

| Similarweb | NA | 1.1x | 46.16% | ★★★★★☆ |

| Appian | 1753.6x | 2.0x | 40.11% | ★★★★★☆ |

| First Bancorp | 8.9x | 3.4x | 31.19% | ★★★★☆☆ |

| PCB Bancorp | 8.7x | 3.0x | 18.07% | ★★★★☆☆ |

| Union Bankshares | 9.2x | 1.9x | 21.53% | ★★★★☆☆ |

| Angel Studios | NA | 1.3x | -36.57% | ★★★★☆☆ |

| German American Bancorp | 12.0x | 4.4x | 44.69% | ★★★☆☆☆ |

| Bank of Marin Bancorp | NA | 11.9x | 33.35% | ★★★☆☆☆ |

| Ultralife | NA | 0.6x | 17.16% | ★★★☆☆☆ |

Let's review some notable picks from our screened stocks.

Mesa Laboratories (MLAB)

Simply Wall St Value Rating: ★★★★★☆

Overview: Mesa Laboratories operates in the fields of clinical genomics, calibration solutions, biopharmaceutical development, and sterilization and disinfection control with a market cap of approximately $1.04 billion.

Operations: Mesa Laboratories generates revenue primarily from four segments: Sterilization and Disinfection Control ($97.18 million), Calibration Solutions ($53.25 million), Biopharmaceutical Development ($52.40 million), and Clinical Genomics ($44.72 million). The company has experienced fluctuations in its net income margin, with recent periods showing negative margins, such as -1.05% in December 2024, before returning to positive at 1.51% by December 2025. Operating expenses have been a significant component of costs, with General & Administrative Expenses consistently being the largest expense within this category across multiple periods.

PE: 161.4x

Mesa Labs, a small company in the United States, is undergoing significant changes with the appointment of Dr. Siddhartha Kadia as CEO and President, bringing over 20 years of experience in life sciences. Insider confidence is evident with Shiraz Ladiwala purchasing 3,500 shares for US$252,805. However, financial challenges persist as interest payments aren't well-covered by earnings and liabilities are entirely funded through external borrowing. Earnings are projected to grow by 30% annually.

Shoe Carnival (SCVL)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Shoe Carnival is a leading footwear retailer in the United States, offering a wide variety of shoes for men, women, and children through its network of stores and online platform with a market capitalization of approximately $0.58 billion.

Operations: Shoe Carnival's revenue primarily comes from sales, with a recent peak of $1.33 billion in early 2022. The company's gross profit margin increased to 39.60% during this period but later showed a downward trend, reaching 36.57% by early 2026. Operating expenses have consistently been a significant part of the cost structure, impacting net income levels over time.

PE: 9.1x

Shoe Carnival, a company in the retail sector, recently reported a first-quarter net loss of US$5.63 million, contrasting with last year's net income of US$9.34 million. Despite this setback and declining sales over the past five years, insider confidence remains evident with recent share purchases by executives in March 2026. The company is undergoing strategic changes, including a proposed name change to Shoe Station Group and plans for store rebanners to drive future growth amidst challenging market conditions.

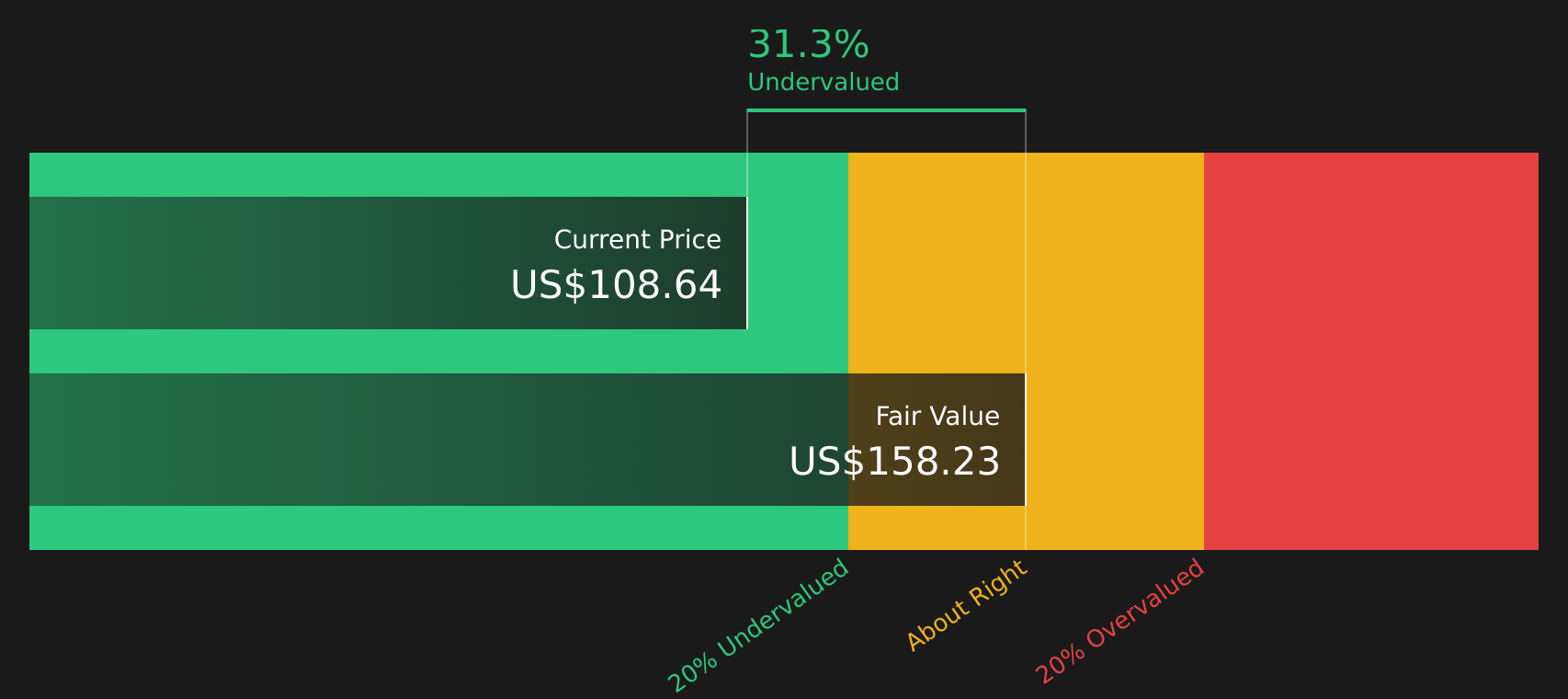

Similarweb (SMWB)

Simply Wall St Value Rating: ★★★★★☆

Overview: Similarweb is a digital intelligence company that provides web analytics services to businesses, with a market cap of approximately $0.57 billion.

Operations: The company generates revenue primarily through its offerings, with a recent gross profit margin of 79.61%. Significant expenses include sales and marketing, which reached $122.43 million, and research and development costs at $73.91 million for the latest period ending in March 2026. Operating expenses have consistently exceeded gross profit, impacting net income figures over time.

PE: -11.0x

Similarweb, a player in the digital intelligence space, has shown promise with its recent earnings guidance increase for 2026, projecting revenue between US$307 million and US$315 million. The first quarter saw sales of US$73.88 million, up from the previous year. While facing a net loss of US$6.36 million, it marks an improvement from prior figures. Their strategic collaborations with AI platforms like Manus enhance data capabilities and market presence. As they transition leadership by mid-2027, growth prospects remain tied to evolving digital trends and AI integration strategies.

Taking Advantage

- Navigate through the entire inventory of 74 Undervalued US Small Caps With Insider Buying here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.