Undervalued Small Caps With Insider Buying In June 2026

Caledonia Mining Corporation PLC CMCL | 0.00 |

The United States market has shown robust performance, rising 2.2% over the last week and climbing 25% in the past year, with earnings anticipated to grow by 19% annually in the coming years. In this thriving environment, identifying stocks that are potentially undervalued yet demonstrate strong fundamentals can be a strategic move for investors looking to capitalize on growth opportunities.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Betterware de MéxicoP.I. de | 9.9x | 0.8x | 44.86% | ★★★★★★ |

| Kingstone Companies | 7.5x | 1.0x | 48.29% | ★★★★★☆ |

| Ferroglobe | NA | 0.5x | 26.18% | ★★★★★☆ |

| Appian | 1930.3x | 2.2x | 33.46% | ★★★★★☆ |

| Bank of the James Financial Group | 10.2x | 2.2x | 20.02% | ★★★★☆☆ |

| Angel Oak Mortgage REIT | 13.0x | 5.9x | 26.13% | ★★★★☆☆ |

| German American Bancorp | 12.5x | 4.6x | 42.66% | ★★★☆☆☆ |

| Patria Investments | 25.9x | 4.7x | 4.74% | ★★★☆☆☆ |

| Union Bankshares | 9.4x | 2.0x | 19.52% | ★★★☆☆☆ |

| Similarweb | NA | 1.6x | 16.61% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

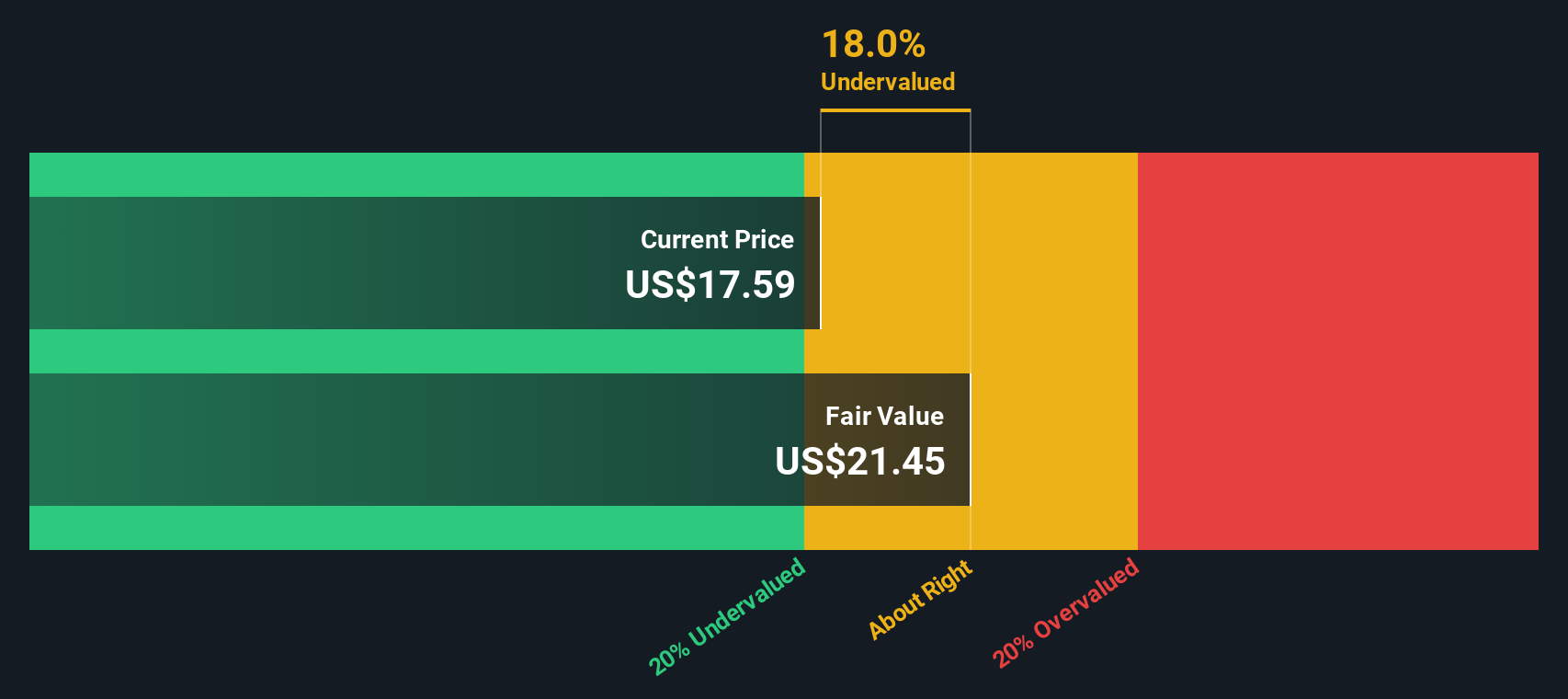

Value Line (VALU)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Value Line is a company primarily engaged in publishing investment-related information and analysis, with a market capitalization of approximately $0.56 billion.

Operations: The company generates revenue primarily through its publishing segment, with recent figures showing $33.83 million. The cost of goods sold is $6.04 million, leading to a gross profit margin of 82.15%. Operating expenses include general and administrative costs amounting to $19.22 million and sales & marketing expenses at $3.73 million, impacting the overall profitability structure.

PE: 14.8x

Value Line, a smaller company in the U.S. market, is attracting attention for its potential value despite recent challenges. Although earnings have declined by 2.5% annually over the last five years, insider confidence is evident with share purchases from November 2025 to January 2026 totaling US$0.65 million for 17,438 shares. The company recently increased its dividend by 7.7%, marking the twelfth consecutive annual rise, and reported improved net income of US$18.05 million for nine months ending January 31, 2026 compared to US$16.74 million previously—indicating resilience amidst funding reliant on external borrowing rather than customer deposits.

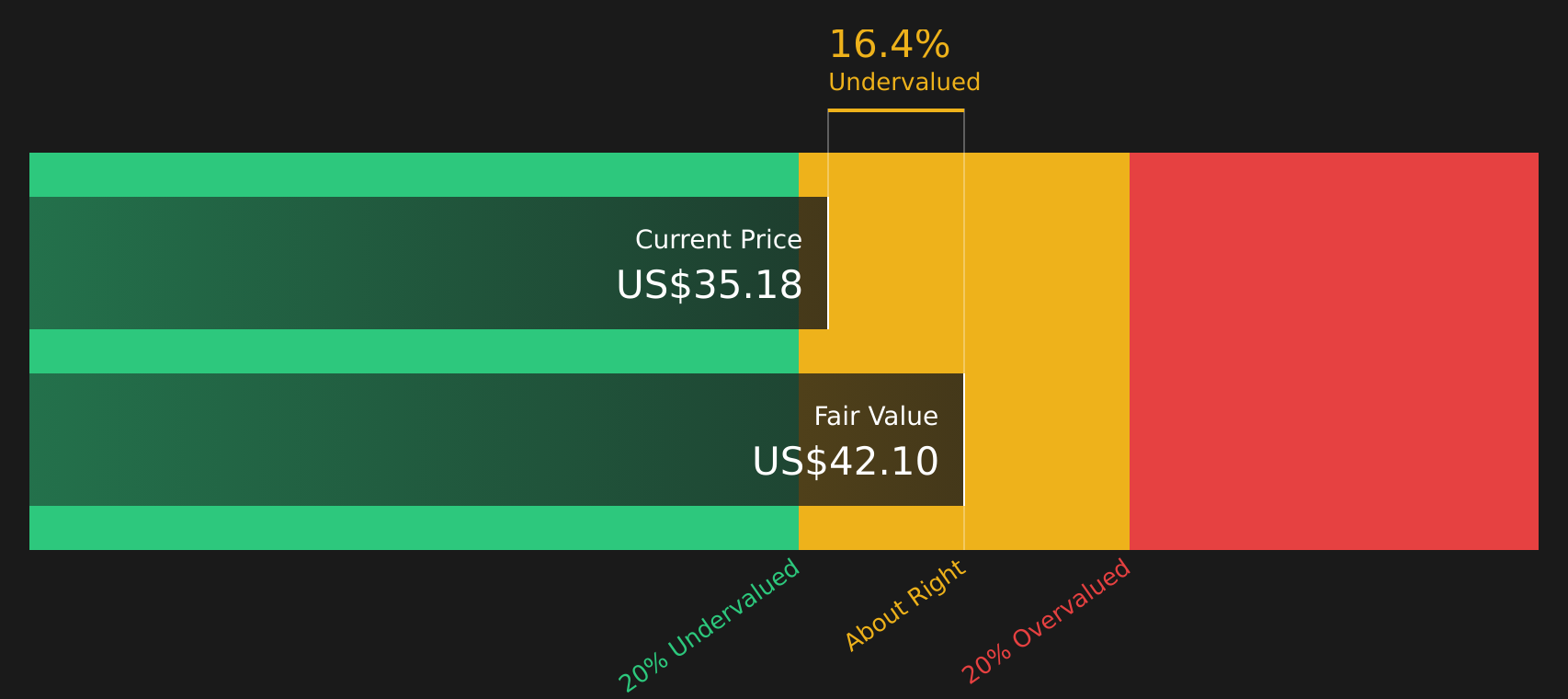

Caledonia Mining (CMCL)

Simply Wall St Value Rating: ★★★★★★

Overview: Caledonia Mining is a gold mining company primarily focused on its Blanket Mine in Zimbabwe, with a market cap of approximately $0.14 billion.

Operations: Caledonia Mining's primary revenue stream is derived from its operations, with a significant portion of costs attributed to COGS and operating expenses. The company has experienced fluctuations in its net income margin, which reached as high as 62.12% in Q3 2019 but also saw negative margins like -6.87% in Q3 2023. Over recent periods, the gross profit margin was observed at levels such as 60.18% in Q4 2025 and 60.47% by Q1 2026, indicating variations over time.

PE: 6.6x

Caledonia Mining, a smaller company in the mining sector, is showing signs of being an attractive opportunity. Recent exploration at the Motapa property has revealed substantial gold mineralization, potentially enhancing its Bilboes project. The company's earnings for Q1 2026 increased to US$15.85 million from US$8.92 million year-over-year, with sales rising to US$66.43 million from US$56.18 million. Despite relying on external funding sources, insider confidence remains strong as insiders have been purchasing shares throughout the year, indicating potential growth prospects and value realization in their strategic projects.

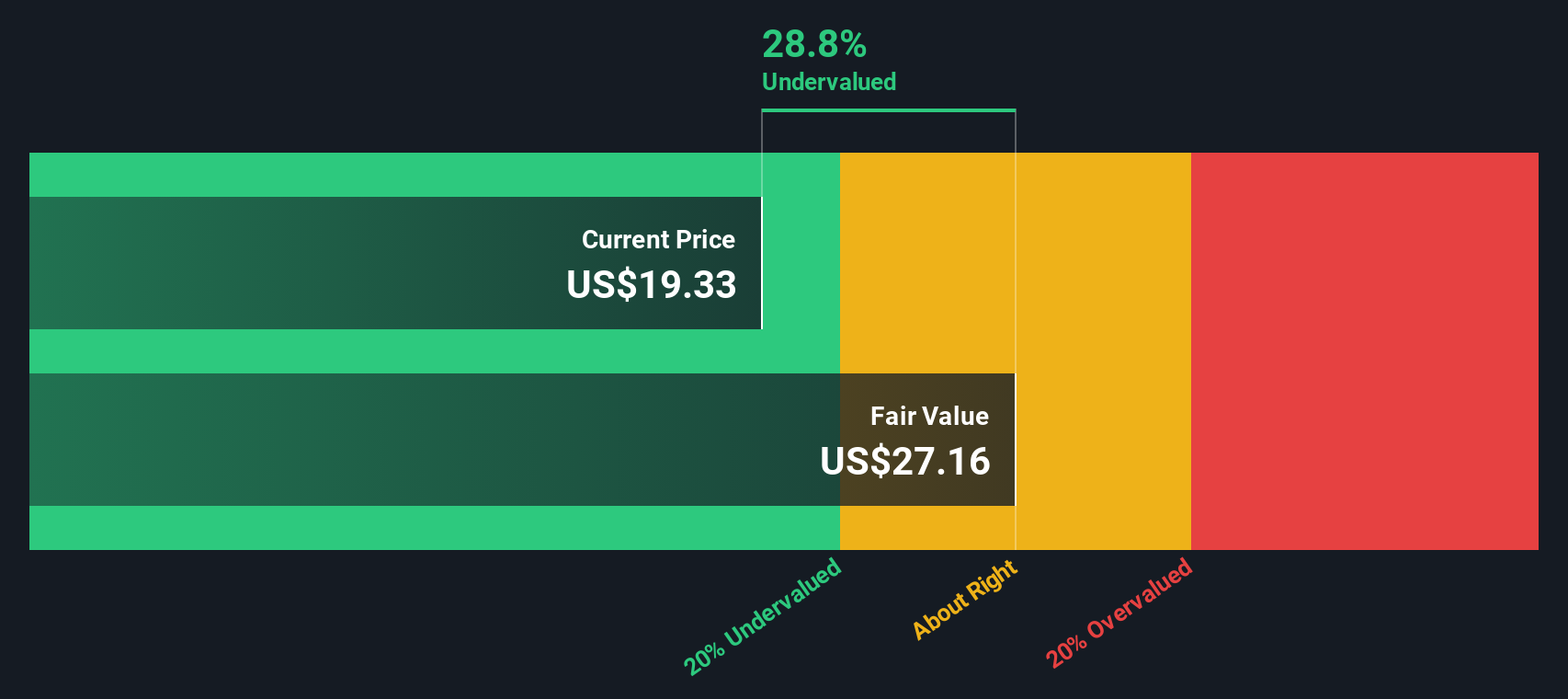

Northpointe Bancshares (NPB)

Simply Wall St Value Rating: ★★★★★☆

Overview: Northpointe Bancshares operates primarily in retail banking and mortgage warehouse services, with a market capitalization of $1.25 billion.

Operations: Northpointe Bancshares generates revenue from its Retail Banking and Mortgage Warehouse segments, with recent figures showing $167.22 million and $84.30 million respectively. The company has experienced a notable increase in net income margin, rising from 5.32% at the end of 2022 to 31.12% by mid-2026, supported by consistent gross profit margins of 100%. Operating expenses primarily consist of general and administrative costs, which have varied over time but remained a significant portion of total expenses.

PE: 7.9x

Northpointe Bancshares, a smaller player in the U.S. market, recently showcased promising financial performance with net interest income rising to US$41.27 million for Q1 2026 from US$30.39 million the previous year. Insider confidence is evident as they increased their share purchases over recent months, signaling potential optimism about future growth prospects. Despite a low allowance for bad loans at 11%, earnings are projected to grow annually by 15.89%, highlighting its potential value amidst industry peers.

Where To Now?

- Dive into all 70 of the Undervalued US Small Caps With Insider Buying we have identified here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.