Undervalued Small Caps With Insider Buying Opportunities In May 2026

Arbor Realty Trust Inc ABR | 0.00 |

In the last week, the United States market has stayed flat, but it has shown a robust 29% rise over the past 12 months with earnings forecasted to grow by 16% annually. In this environment, identifying small-cap stocks that are potentially undervalued and exhibit insider buying can offer intriguing opportunities for investors looking to capitalize on growth prospects.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Financial Institutions | 8.7x | 2.8x | 49.61% | ★★★★★☆ |

| Ferroglobe | NA | 0.6x | 45.31% | ★★★★★☆ |

| 1st Source | 11.1x | 4.2x | 42.00% | ★★★★☆☆ |

| Aldeyra Therapeutics | NA | NA | 49.64% | ★★★★☆☆ |

| Metropolitan Bank Holding | 12.7x | 3.6x | 42.32% | ★★★☆☆☆ |

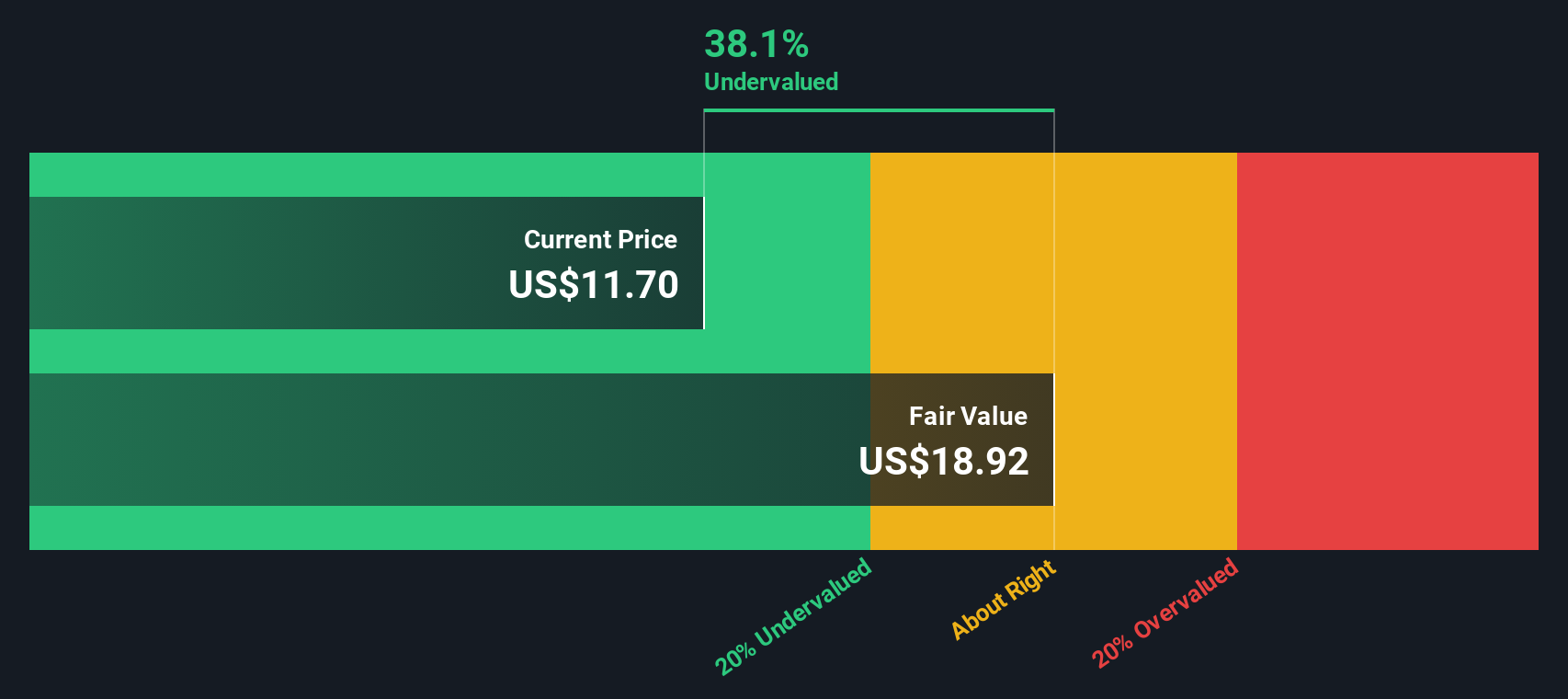

| Tennant | 34.1x | 1.2x | 38.10% | ★★★☆☆☆ |

| German American Bancorp | 12.0x | 4.4x | 46.07% | ★★★☆☆☆ |

| Eagle Financial Services | 10.6x | 2.5x | 32.40% | ★★★☆☆☆ |

| Union Bankshares | 10.3x | 2.1x | 22.81% | ★★★☆☆☆ |

| New Peoples Bankshares | 9.4x | 2.2x | 25.73% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

TriMas (TRS)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: TriMas is a diversified manufacturer of engineered products serving various industries, with a market capitalization of approximately $1.25 billion.

Operations: TriMas generates revenue primarily through its sales, with recent quarterly figures showing revenue of $973.84 million and $1.01 billion. The company's cost structure includes significant expenses such as the cost of goods sold (COGS), which was $753.85 million in one quarter, and operating expenses, including general and administrative costs that reached up to $138.95 million in another period. Gross profit margin has shown variation over time, with a recent figure reported at 23.10%. Net income has fluctuated significantly, reflecting various non-operating expenses impacting profitability across different periods.

PE: 19.3x

TriMas, a smaller company in the U.S., has shown mixed financial signals. Recent Q1 2026 earnings reported sales of US$168.28 million, up from US$152.46 million last year, yet net income soared to US$800.83 million due to significant one-off items impacting results. The company's confidence is evident with insider purchases and a completed share repurchase plan totaling 22.81% of shares for US$285.69 million by end-2025, signaling potential value recognition despite high-risk external borrowing reliance for funding needs.

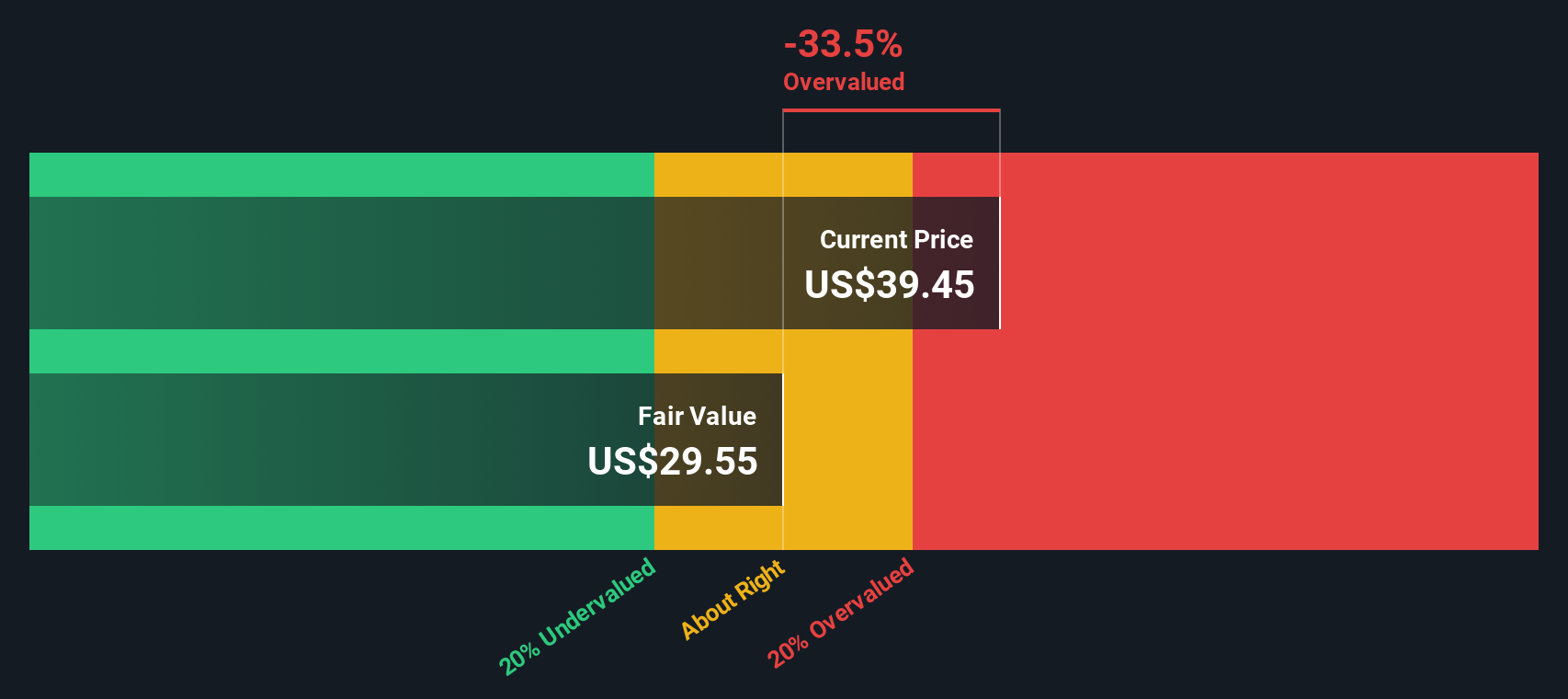

Arbor Realty Trust (ABR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Arbor Realty Trust is a real estate investment trust that specializes in originating and servicing loans for multifamily, single-family rental, and commercial real estate markets with a market cap of approximately $2.56 billion.

Operations: The company's revenue is primarily derived from its Agency Business and Structured Business segments. The gross profit margin has shown a notable trend, reaching 92.28% in September 2023. Operating expenses, including general and administrative costs, significantly impact the overall financial performance, with recent figures showing an increase to $257.50 million by September 2025.

PE: 14.1x

Arbor Realty Trust, a small US real estate investment trust, showcases potential value with insider confidence evident from recent share purchases. Despite a dip in net income to US$148.8 million for 2025 from the previous year and impairment charges of US$20.5 million, Arbor's strategic moves like a US$762.6 million securitization aim to bolster its financial footing. The appointment of experienced executives further strengthens its operational capabilities, hinting at promising future growth in the commercial real estate sector.

FMC (FMC)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: FMC is a global agricultural sciences company that provides innovative solutions for crop protection, plant health, and professional pest control, with a market cap of approximately $12.60 billion.

Operations: FMC's revenue is primarily derived from its sales, with recent figures showing a decline to $3.43 billion as of March 2026. The company's cost structure includes significant expenses such as COGS, which was $2.33 billion in the same period, and operating expenses totaling $942.2 million. Notably, FMC's net income margin has experienced volatility, reaching -71.52% by March 2026 due to substantial non-operating expenses amounting to $2.62 billion during this timeframe.

PE: -0.8x

FMC, a company in the specialty chemicals industry, recently faced financial challenges with a net loss of US$281 million for Q1 2026. Despite this, insider confidence is evident as Independent Director Michael Barry purchased shares worth approximately US$250,000 in February 2026. This move suggests potential value recognition amidst ongoing strategic initiatives like debt restructuring and product innovation. With regulatory approval for Isoflex active in the EU and plans for further launches by 2027, FMC aims to enhance its growth trajectory while exploring strategic options to bolster shareholder value.

Turning Ideas Into Actions

- Unlock more gems! Our Undervalued US Small Caps With Insider Buying screener has unearthed 56 more companies for you to explore.Click here to unveil our expertly curated list of 59 Undervalued US Small Caps With Insider Buying.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.