Undervalued Small Caps With Insider Buying To Consider For Your Portfolio

FirstSun Capital Bancorp FSUN | 38.28 | -0.10% |

The United States market has experienced a robust performance, climbing 3.4% in the last week and an impressive 30% over the past year, with earnings projected to grow by 16% annually. In this dynamic environment, identifying stocks that combine attractive valuations with insider buying can be a strategic approach for investors looking to enhance their portfolios.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Enovis | NA | 0.6x | 44.48% | ★★★★★★ |

| PCB Bancorp | 9.4x | 3.1x | 21.42% | ★★★★★☆ |

| FirstSun Capital Bancorp | 10.8x | 2.7x | 46.06% | ★★★★★☆ |

| Financial Institutions | 9.2x | 2.9x | 40.83% | ★★★★★☆ |

| Tennant | 31.6x | 1.2x | 42.33% | ★★★☆☆☆ |

| Southside Bancshares | 14.3x | 4.2x | 49.60% | ★★★☆☆☆ |

| German American Bancorp | 14.8x | 4.9x | 43.66% | ★★★☆☆☆ |

| New Peoples Bankshares | 9.5x | 2.3x | 25.14% | ★★★☆☆☆ |

| Bank of the James Financial Group | 11.5x | 2.1x | 42.71% | ★★★☆☆☆ |

| Douglas Emmett | 105.7x | 1.6x | 44.34% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

Distribution Solutions Group (DSGR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Distribution Solutions Group operates as a provider of value-added distribution solutions across various sectors, with a market capitalization of $1.85 billion.

Operations: Lawson, Testequity, Gexpro Services, and the Canada Branch Division contribute significantly to revenue streams. The company has experienced fluctuations in its net income margin, with a notable shift from -1.23% in Q1 2024 to 0.06% in Q1 2025. Operating expenses consistently impact financial performance, with general and administrative expenses being a major component.

PE: 153.3x

Distribution Solutions Group, a smaller player in the U.S. market, shows potential for growth with earnings forecasted to increase by 64.61% annually. Despite high volatility and reliance on external borrowing, insider confidence is evident as Robert Zamarripa purchased 14,000 shares worth US$297,220 between October and December 2025. The company reported a net income of US$8.35 million for 2025 compared to a loss the previous year and completed a share repurchase of US$34.61 million since April 2019, indicating strategic financial maneuvers amidst industry challenges.

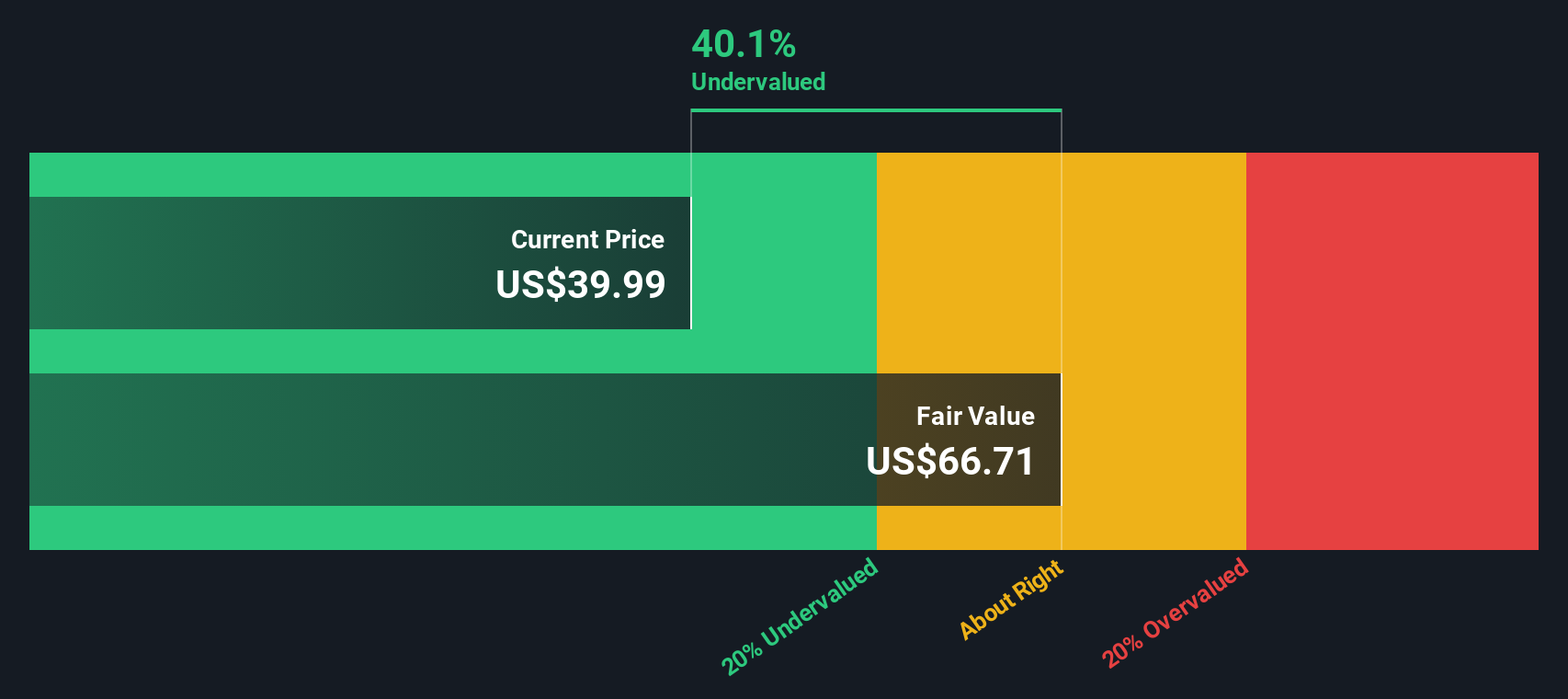

FirstSun Capital Bancorp (FSUN)

Simply Wall St Value Rating: ★★★★★☆

Overview: FirstSun Capital Bancorp operates primarily in the banking sector with additional activities in corporate and mortgage operations, and has a market cap of $1.2 billion.

Operations: The company's revenue primarily stems from its Banking and Mortgage Operations segments, contributing $322.60 million and $76.56 million, respectively. Operating expenses are significant, with General & Administrative Expenses consistently being the largest component, reaching up to $210.07 million in recent periods. The net income margin has shown variability over time but reached 29.32% in mid-2023 before adjusting to 24.81% by the end of 2025.

PE: 10.8x

FirstSun Capital Bancorp, a small company in the financial sector, shows potential for growth with earnings projected to increase by 43.63% annually. Despite recent removals from several Russell indices as of March 31, 2026, insider confidence is evident through share purchases. The board's restructuring on April 1, 2026, including new directors from First Foundation Inc., suggests strategic realignment post-merger. With US$97.94 million net income reported for 2025 and an expanding board of directors, FirstSun aims to navigate its evolving market landscape effectively.

Home Bancorp (HBCP)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Home Bancorp operates as a bank holding company providing a range of banking services and products, with a market cap of approximately $0.28 billion.

Operations: The company's primary revenue stream is from its banking operations, with a reported revenue of $148.66 million. Operating expenses are significant, with general and administrative expenses accounting for the largest portion at $76.29 million. The net income margin has shown variability, reaching 30.99% in recent periods, indicating how much of its revenue is retained as profit after all expenses are accounted for.

PE: 11.1x

Home Bancorp's recent earnings report for Q4 2025 shows a promising financial trajectory, with net interest income rising to US$34.05 million and net income reaching US$11.41 million, both up from the previous year. Insider confidence is evident as they increased their holdings in recent months, reflecting potential optimism about future performance. Despite low loan charge-offs of US$165,000 and steady dividends at $0.31 per share, the company maintains a cautious stance with a low allowance for bad loans at 97%.

Make It Happen

- Unlock more gems! Our Undervalued US Small Caps With Insider Buying screener has unearthed 55 more companies for you to explore.Click here to unveil our expertly curated list of 58 Undervalued US Small Caps With Insider Buying.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.