Undervalued Small Caps With Insider Buying To Watch In May 2026

InMode Ltd. INMD | 0.00 |

Over the last 7 days, the United States market has remained flat, yet it has shown a robust 25% rise over the past 12 months with earnings forecasted to grow by 17% annually. In this environment, identifying stocks that are potentially undervalued and have insider buying can be an effective strategy for investors looking to capitalize on growth opportunities.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| PCB Bancorp | 8.5x | 2.9x | 20.77% | ★★★★★☆ |

| First United | 9.4x | 2.7x | 48.26% | ★★★★★☆ |

| Financial Institutions | 8.7x | 2.8x | 33.25% | ★★★★★☆ |

| First Bancorp | 8.7x | 3.3x | 32.57% | ★★★★☆☆ |

| New Peoples Bankshares | 8.9x | 2.3x | 36.87% | ★★★★☆☆ |

| Ultralife | NA | 0.5x | 21.61% | ★★★★☆☆ |

| Bank of Marin Bancorp | NA | 11.6x | 35.00% | ★★★☆☆☆ |

| Bank of the James Financial Group | 9.5x | 2.1x | 40.33% | ★★★☆☆☆ |

| Aldeyra Therapeutics | NA | NA | 47.12% | ★★★☆☆☆ |

| Angel Studios | NA | 1.4x | -45.58% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Organogenesis Holdings (ORGO)

Simply Wall St Value Rating: ★★★★★☆

Overview: Organogenesis Holdings is a company specializing in regenerative medicine, focusing on the development and commercialization of products for wound care and surgical biologics, with a market capitalization of approximately $0.35 billion.

Operations: The company generates revenue primarily from its regenerative medicine segment, which reached $514.70 million recently. The cost of goods sold (COGS) for the same period was $134.39 million, resulting in a gross profit margin of 73.89%. Operating expenses include significant allocations to research and development (R&D), with recent figures at $49.06 million, alongside general and administrative expenses amounting to $308.70 million.

PE: -23.9x

Organogenesis Holdings, a small company in the U.S., has faced challenges with declining revenue and profitability. For Q1 2026, they reported a net loss of US$53.16 million on sales of US$36.25 million, contrasting sharply with last year’s figures. Despite financial hurdles, the company shows potential through its recent FDA submission for ReNu, targeting knee osteoarthritis—a market affecting millions in America. This strategic move could position them well for future growth amidst current struggles.

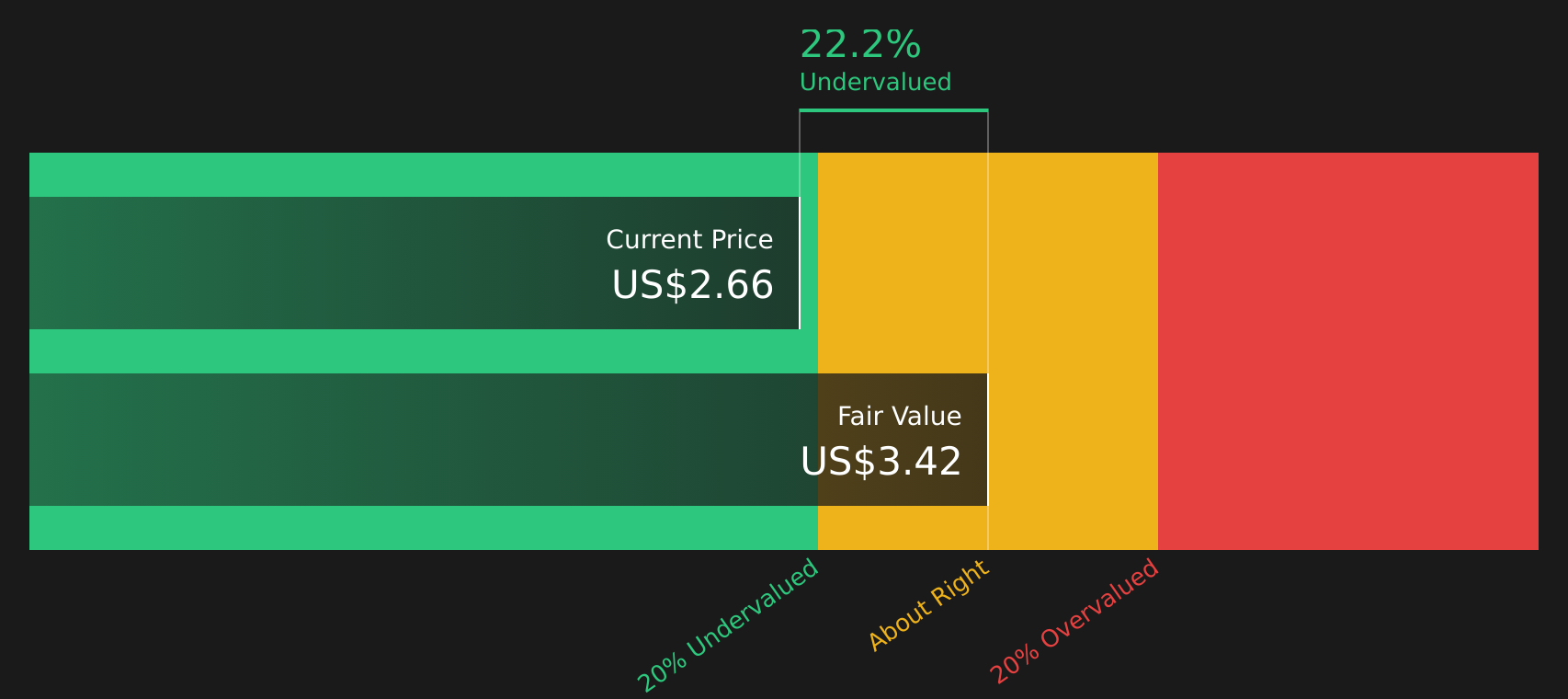

InMode (INMD)

Simply Wall St Value Rating: ★★★★★☆

Overview: InMode is a company that specializes in developing and manufacturing minimally invasive aesthetic medical devices, with a market capitalization of approximately $2.10 billion.

Operations: The primary revenue stream is from surgical and medical equipment, amounting to $374.64 million. The company's gross profit margin was 77.84% as of March 31, 2026, with significant operating expenses primarily driven by sales and marketing efforts totaling $183.78 million and R&D expenses of $13.97 million in the same period.

PE: 10.2x

InMode, a smaller U.S. company, has been navigating challenges with declining profit margins and earnings forecasted to drop by 0.6% annually over the next three years. Despite this, they reported Q1 2026 sales of US$82.02 million, up from last year's US$77.87 million, though net income fell to US$11.56 million from US$18.2 million a year ago. Recent management changes include Dr. Hadar Ron as Interim Chair and a CFO transition with Yair Malca stepping down but staying on as a consultant for six months to ensure stability during this period of change and strategic realignment through their share repurchase program targeting 10% of outstanding shares using available cash resources while maintaining revenue guidance between $365-$375M for 2026 reflecting potential growth amidst current challenges faced internally within leadership roles transitioning smoothly despite external borrowing risks associated primarily due lack customer deposits impacting funding sources overall positioning them uniquely among peers in industry context today May14th2026

Hudson Pacific Properties (HPP)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Hudson Pacific Properties is a real estate investment trust focusing on office and studio properties, with a market cap of $1.09 billion.

Operations: The company generates revenue primarily from its office and studio segments, with the office segment contributing significantly more. Over recent periods, there has been a noticeable decline in gross profit margin, which stood at 0.49% as of March 2026. Operating expenses have consistently included significant depreciation and amortization costs, impacting overall profitability.

PE: -1.1x

Hudson Pacific Properties, a smaller player in the U.S. market, recently reported a Q1 2026 net loss of US$48.04 million, an improvement from last year's US$69.52 million loss. Despite this progress and efforts to cut costs by up to US$27 million annually through strategic downsizing of Quixote subsidiaries, profitability remains elusive with no forecasted turnaround in three years. Insider confidence is notable with recent share purchases indicating potential long-term faith in the company's recovery strategy amidst volatile share prices.

Taking Advantage

- Get an in-depth perspective on all 68 Undervalued US Small Caps With Insider Buying by using our screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.