Undiscovered Gems in Global Markets to Explore This June 2026

FOURTH MILLING 2286.SA | 0.00 |

As global markets navigate a landscape marked by heightened inflation pressures and geopolitical tensions, small-cap stocks have emerged as leaders, with the Russell 2000 Index gaining significant ground. This backdrop of cautious optimism and shifting market dynamics presents an opportunity to explore lesser-known stocks that may offer unique growth potential. In such an environment, a good stock often exhibits resilience in volatile conditions, strong fundamentals, and the ability to capitalize on emerging trends or sectors that are gaining traction amid broader market shifts.

Top 10 Undiscovered Gems With Strong Fundamentals Globally

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| CNMC Goldmine Holdings | 0.84% | 32.52% | 78.36% | ★★★★★★ |

| Transcend Information | NA | 4.45% | 25.56% | ★★★★★★ |

| Nippon Carbide Industries | 16.74% | 1.99% | -4.81% | ★★★★★★ |

| GROUPE SFPI(EMMQF.US) | 18.02% | 4.25% | -29.76% | ★★★★★★ |

| Zhejiang Jolly PharmaceuticalLTD | 21.31% | 17.83% | 29.70% | ★★★★★☆ |

| Magnate Technology | 77.36% | 10.92% | 35.95% | ★★★★★☆ |

| Fourth Milling | NA | 8.33% | 16.85% | ★★★★★☆ |

| Decora | 17.26% | 9.44% | 7.12% | ★★★★★☆ |

| Sing Investments & Finance | 0.15% | 7.06% | 8.65% | ★★★★☆☆ |

| Shengda ResourcesLtd | 54.08% | 7.99% | 3.75% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Storskogen Group (OM:STOR B)

Simply Wall St Value Rating: ★★★★★★

Overview: Storskogen Group AB (publ) owns and develops small and medium-sized businesses across trade, industry, and services sectors, with a market capitalization of approximately SEK15.13 billion.

Operations: Storskogen Group generates revenue primarily from its trade, industry, and services segments, with the industry segment contributing SEK14.30 billion. The company's net profit margin is a key financial metric to consider when evaluating its profitability.

Storskogen Group, a nimble player in the acquisition of small to medium-sized businesses, has seen its earnings skyrocket by 3804% over the past year, outperforming its industry peers. The company's interest payments are well-covered with an EBIT coverage of 6x, and it trades at a significant discount of 72% below estimated fair value. Despite a one-off loss impacting recent results by SEK1.7 billion, Storskogen's strategic focus on high-margin sectors like digital healthcare positions it for potential growth. However, challenges such as currency volatility and competitive pressures could impact future performance and revenue growth projections remain modest at 3.4% annually over the next three years.

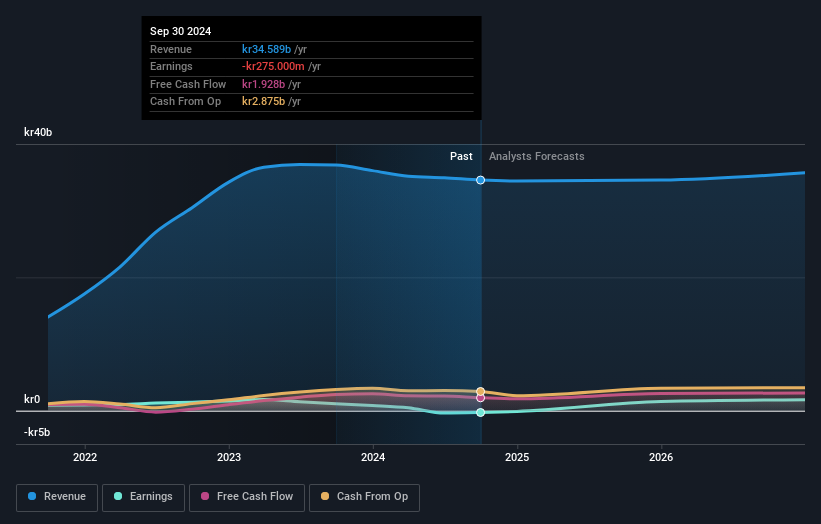

Fourth Milling (SASE:2286)

Simply Wall St Value Rating: ★★★★★☆

Overview: Fourth Milling Company is involved in the production of flour, feed, bran, and wheat derivatives both in Saudi Arabia and internationally, with a market capitalization of SAR2.31 billion.

Operations: The company generates revenue primarily from its food processing segment, amounting to SAR669.52 million.

Fourth Milling, a relatively small player in the food industry, has shown promising financial health with earnings growing by 15% over the past year, outpacing the industry's negative growth of -16.6%. The company operates debt-free, which enhances its financial stability and reduces risks associated with interest payments. Trading at nearly 38% below its estimated fair value suggests potential for market appreciation. Recent quarterly results showed sales of SAR 175 million and net income of SAR 53 million, indicating steady performance compared to last year. With a forecasted revenue growth rate of over 6% annually, Fourth Milling seems poised for continued expansion in its sector.

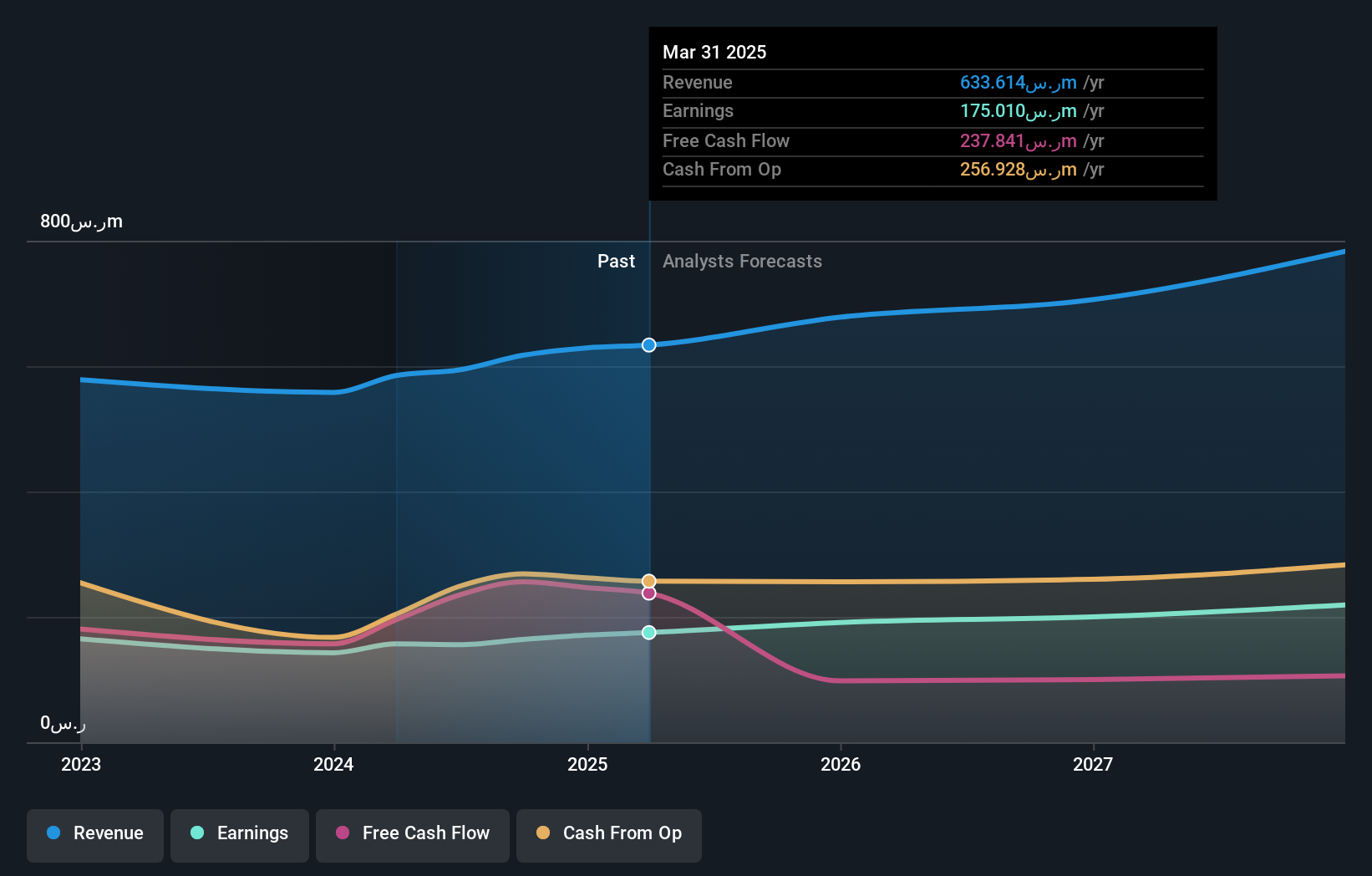

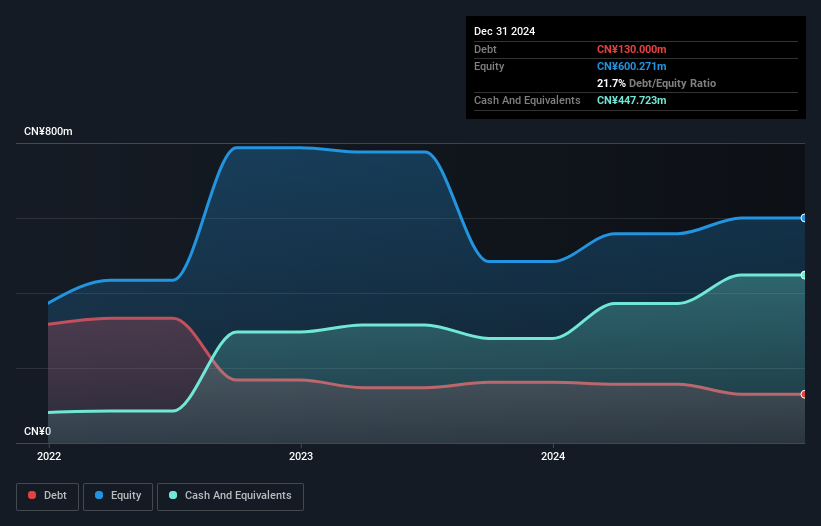

Zibuyu Group (SEHK:2420)

Simply Wall St Value Rating: ★★★★★☆

Overview: Zibuyu Group Limited is an investment holding company that functions as a cross-border e-commerce enterprise, operating in China and internationally across North America, Asia, and Europe, with a market capitalization of HK$2 billion.

Operations: The group generates revenue primarily through its online retail segment, which reported CN¥4.66 billion.

Zibuyu Group, a promising player in the retail sector, has shown impressive financial growth with earnings soaring by 78.6% over the past year, outpacing its industry peers significantly. The company reported sales of CNY 4.66 billion for 2025 compared to CNY 3.33 billion in the previous year and net income rose to CNY 269.22 million from CNY 150.78 million, reflecting robust operational performance and high-quality non-cash earnings. Trading at about 31% below fair value estimates suggests potential undervaluation, while a final dividend of HKD 0.23 per share underscores its commitment to shareholder returns amidst strong cash flow positivity.

Taking Advantage

- Reveal the 144 hidden gems among our Global Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.