Undiscovered Gems in Middle East Stocks To Watch May 2026

ALRASHEED 9601.SA | 0.00 |

The Middle East stock markets have recently faced volatility, with Gulf equities experiencing a downturn following geopolitical tensions, including drone strikes affecting key infrastructure in the UAE and Saudi Arabia. Despite these challenges, investors are increasingly interested in identifying stocks that demonstrate resilience and potential for growth amidst uncertainty. In this context, a good stock is one that exhibits strong fundamentals and can navigate the complexities of regional dynamics while capitalizing on emerging opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Al Wathba National Insurance Company PJSC | 3.95% | 9.01% | -11.62% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | 14.04% | 16.38% | 23.83% | ★★★★★★ |

| MOBI Industry | 7.46% | 5.89% | 17.98% | ★★★★★★ |

| Tureks Turizm Tasimacilik Anonim Sirketi | 5.61% | 45.04% | 46.56% | ★★★★★★ |

| Yeni Gimat Gayrimenkul Yatirim Ortakligi | 2.05% | 39.98% | 18.92% | ★★★★★☆ |

| Amir Marketing and Investments in Agriculture | 41.08% | 3.08% | 6.82% | ★★★★★☆ |

| Kirac Galvaniz Telekominikasyon Metal Makine Insaat Elektrik Sanayi ve Ticaret Anonim Sirketi | 18.06% | 129.96% | 46.35% | ★★★★★☆ |

| Smart Shooter | 69.58% | 83.01% | nan | ★★★★★☆ |

| Akmerkez Gayrimenkul Yatirim Ortakligi | NA | 38.05% | 18.53% | ★★★★★☆ |

| Etihad GO Telecom | 0.74% | 38.31% | 54.97% | ★★★★★☆ |

Here's a peek at a few of the choices from the screener.

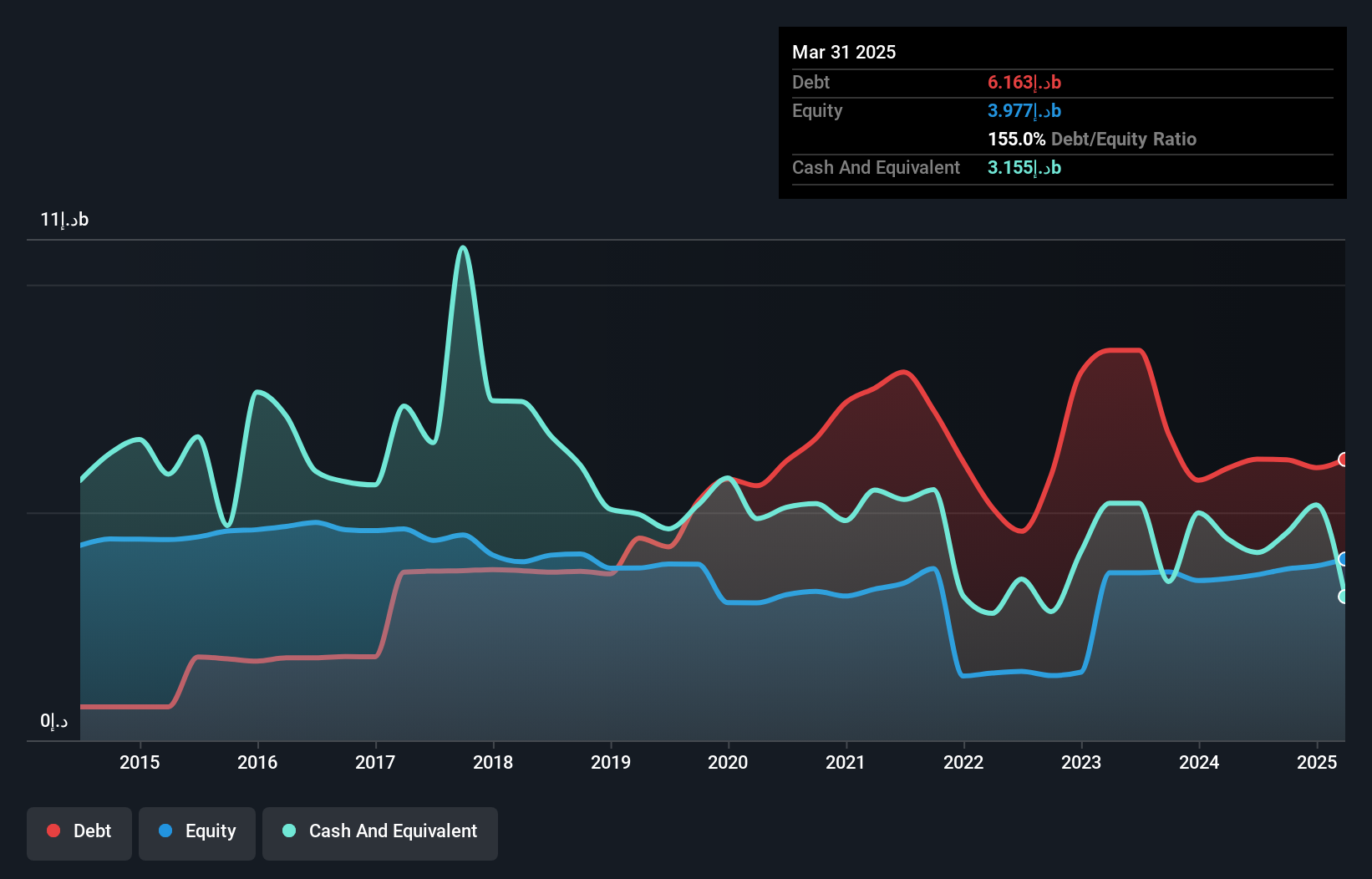

Bank Of Sharjah P.J.S.C (ADX:BOS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Bank Of Sharjah P.J.S.C., along with its subsidiaries, offers commercial and investment banking products and services in the United Arab Emirates, with a market capitalization of AED3.63 billion.

Operations: The primary revenue streams for Bank Of Sharjah include interest income from loans and advances, as well as fees and commissions from banking services. The company's cost structure is significantly influenced by interest expenses related to deposits and borrowings. Notably, the net profit margin has shown variability over recent periods.

Bank of Sharjah showcases a compelling profile with total assets of AED54.7 billion and equity at AED4.7 billion, suggesting a solid foundation. The bank's earnings surged by 81.9% over the past year, outpacing the industry average of 20.3%, highlighting its robust performance in a competitive landscape. However, it grapples with a high level of bad loans at 8.8%, which could be concerning for potential investors despite having low-risk funding sources making up 81% of liabilities primarily from customer deposits. Its price-to-earnings ratio stands attractively at 4.7x compared to the AE market's average of 11.1x, indicating potential undervaluation in this small cap space.

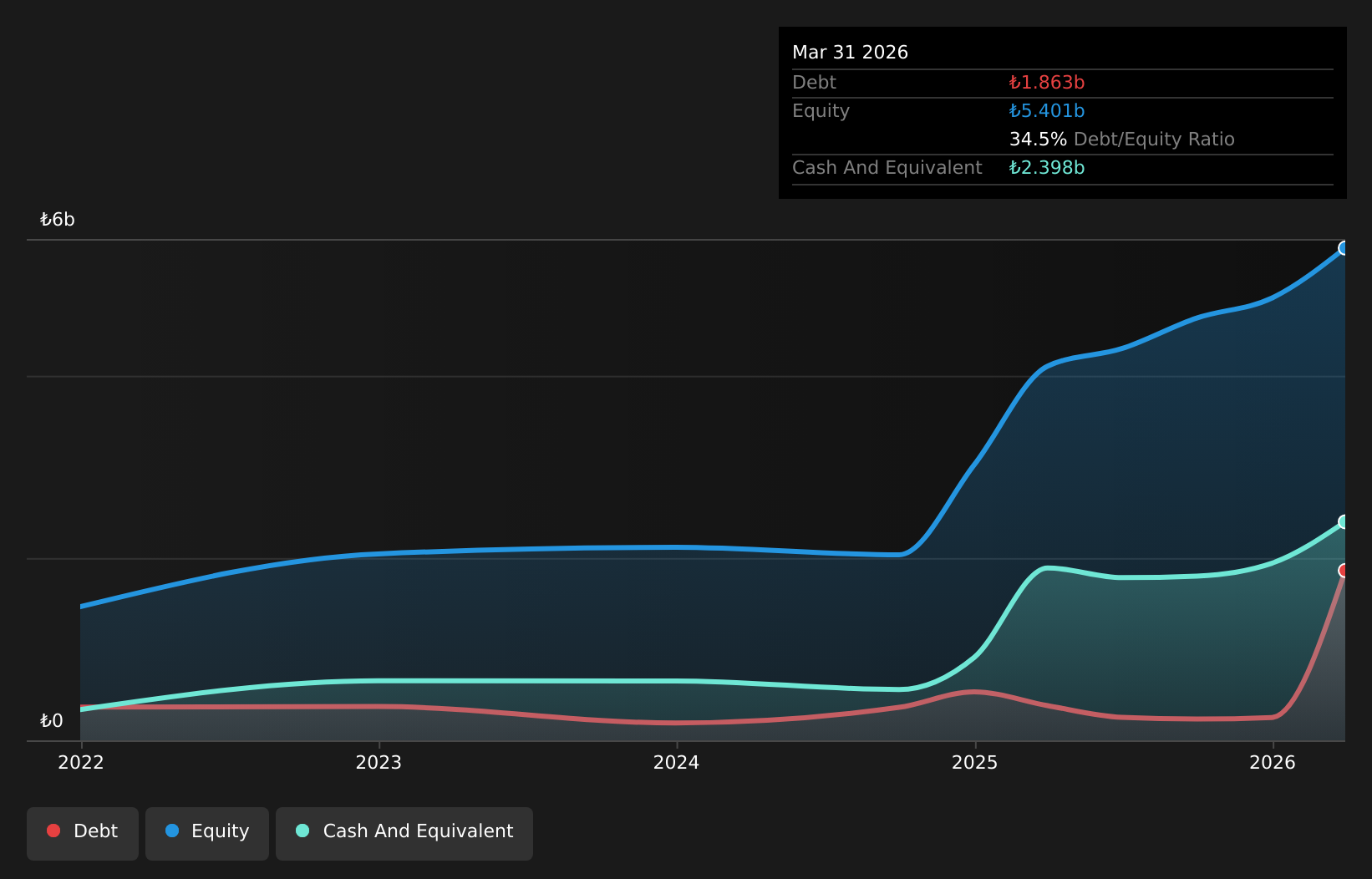

Mopas Marketcilik Gida Sanayi ve Ticaret Anonim Sirketi (IBSE:MOPAS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Mopas Marketcilik Gida Sanayi ve Ticaret Anonim Sirketi operates by selling various consumer products through both physical and online stores, with a market capitalization of TRY11.92 billion.

Operations: Mopas generates revenue through the sale of consumer products in both physical and online retail formats. The company's financial performance is highlighted by a gross profit margin of 28.5%, reflecting its ability to manage costs relative to sales.

Mopas Marketcilik, a small player in the Middle Eastern retail scene, has seen its earnings grow by 30.4% over the past year, outpacing the industry average of -7.8%. Despite this growth, net income for Q1 2026 fell to TRY 66.36 million from TRY 93.62 million a year prior, while sales increased to TRY 5,374.76 million from TRY 4,979.52 million in the same period last year. The company trades at a significant discount of 37% below its estimated fair value and boasts high-quality earnings; however, interest payments are not well-covered by EBIT at just 0.9x coverage ratio.

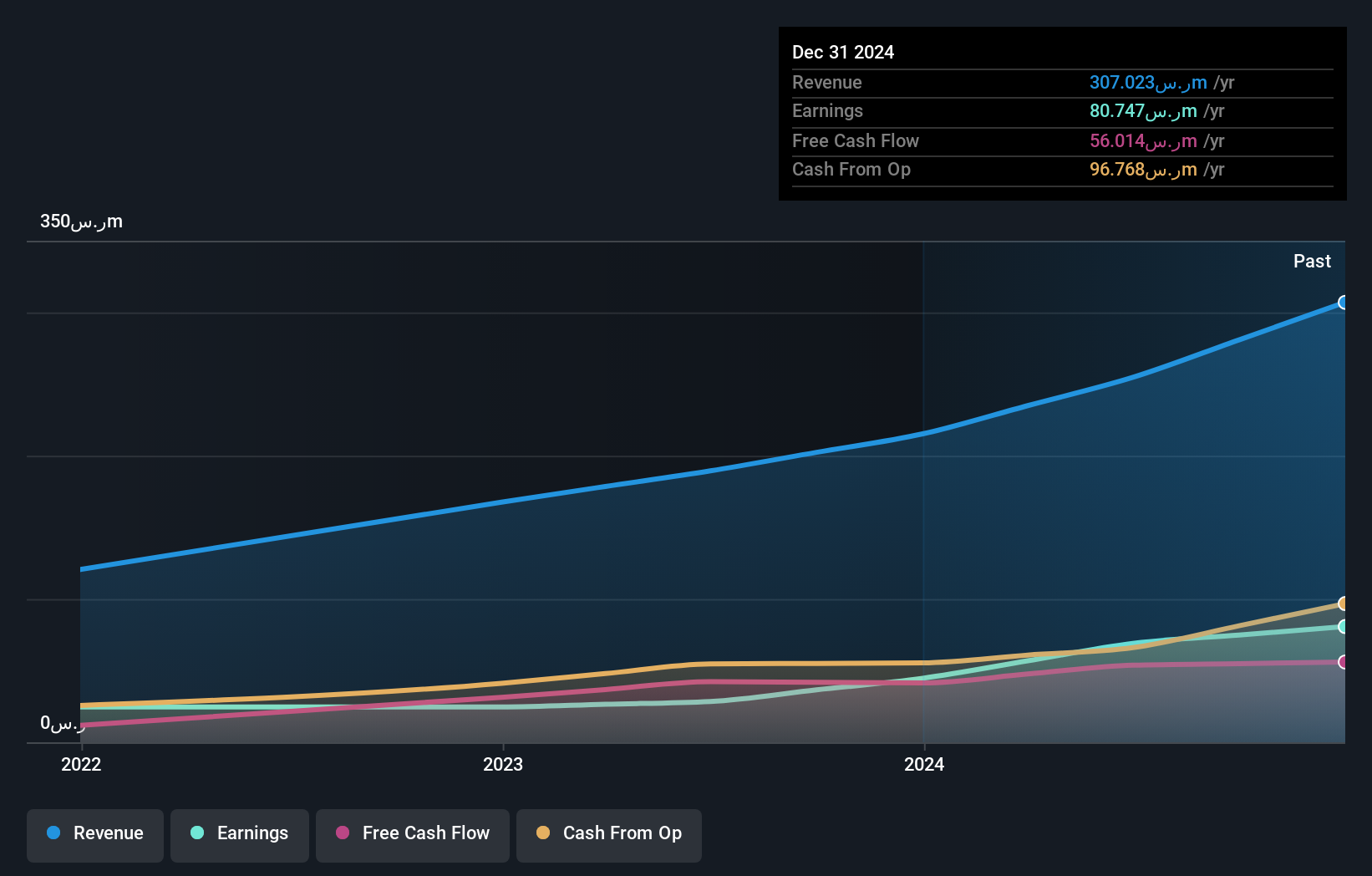

Mohammed Hadi Al-Rasheed (SASE:9601)

Simply Wall St Value Rating: ★★★★★☆

Overview: Mohammed Hadi Al-Rasheed Company specializes in the production of silica sand for various industrial applications and has a market capitalization of SAR1.34 billion.

Operations: The company generates revenue primarily from its Mining Sector, contributing SAR295.49 million, and a smaller portion from the Equipment Maintenance Sector at SAR52.21 million. The focus on silica sand production is evident in the significant revenue share from mining activities.

Mohammed Hadi Al-Rasheed, a promising player in the Middle East market, has shown resilience with its earnings growing by 5.3% over the past year, outpacing the Basic Materials industry growth of 5.1%. Its price-to-earnings ratio stands attractively at 15.9x compared to the South African market average of 18x. Despite a highly volatile share price recently, its financial health appears robust with a net debt to equity ratio of 14.6%, considered satisfactory. Recent developments include entering finance lease agreements worth SAR 15.95 million for asset acquisition and expanding their Audit Committee to enhance governance capabilities further.

Seize The Opportunity

- Investigate our full lineup of 225 Middle Eastern Undiscovered Gems With Strong Fundamentals right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.