Undiscovered Gems in the Middle East to Explore This April 2026

MIAHONA 2084.SA | 17.50 | +1.10% |

As Middle Eastern markets see a surge, led by Dubai's stock index climbing 2% amid hopes of de-escalation in the Iran conflict and a significant economic support package, investors are closely watching the region's small-cap stocks for potential opportunities. In this dynamic environment, identifying promising stocks involves looking for companies with strong fundamentals and resilience to geopolitical tensions.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Al Wathba National Insurance Company PJSC | 10.35% | 8.65% | -7.40% | ★★★★★★ |

| Baazeem Trading | 10.02% | -1.27% | -1.66% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | NA | 17.87% | 23.67% | ★★★★★★ |

| Nofoth Food Products | NA | 20.62% | 23.75% | ★★★★★★ |

| MOBI Industry | 22.69% | 5.89% | 17.98% | ★★★★★★ |

| Najran Cement | 14.49% | -4.20% | -30.16% | ★★★★★★ |

| Alf Meem Yaa for Medical Supplies and Equipment | 27.12% | 12.68% | 18.39% | ★★★★★☆ |

| Yeni Gimat Gayrimenkul Yatirim Ortakligi | 2.52% | 43.31% | 23.27% | ★★★★★☆ |

| Saudi Chemical Holding | 47.39% | 17.85% | 39.66% | ★★★★★☆ |

| Etihad GO Telecom | NA | 38.31% | 54.97% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

Eczacibasi Yatirim Holding Ortakligi (IBSE:ECZYT)

Simply Wall St Value Rating: ★★★★★★

Overview: Eczacibasi Yatirim Holding Ortakligi A.S. is an investment holding company that focuses on marketing and selling construction products in Turkey, with a market capitalization of TRY35.41 billion.

Operations: Eczacibasi Yatirim generates revenue primarily from the marketing and sale of construction products in Turkey. The company has a market capitalization of TRY35.41 billion, reflecting its significant presence in the sector.

Eczacibasi Yatirim Holding Ortakligi stands out with its robust financial health, showcasing a debt-free status and high-quality earnings. Over the past year, it reported an impressive 41.3% earnings growth, significantly outpacing the Industrials industry average of 0.8%. Despite generating less than US$1 million in revenue, it achieved a net income of TRY 820.43 million for 2025, up from TRY 580.56 million the previous year. Basic earnings per share also rose to TRY 7.81 from TRY 5.53 last year, reflecting strong profitability despite limited revenue streams and highlighting potential for future value creation in its niche market space.

Ronesans Gayrimenkul Yatirim (IBSE:RGYAS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Ronesans Gayrimenkul Yatirim A.S. is a commercial real estate development and investment company in Türkiye with a market capitalization of TRY53.26 billion.

Operations: Ronesans Gayrimenkul Yatirim generates revenue primarily from its shopping centers and office spaces, with significant contributions from Hilltown KarSiyaka SHC (TRY2.18 billion) and Maltepe Piazza SHC and Office (TRY1.64 billion). The company also benefits from assets like Optimum Izmir SHC and Samsun Piazza Shopping Center and Hotel, which contribute TRY1.44 billion and TRY1.34 billion, respectively.

Ronesans Gayrimenkul Yatirim, a notable player in the Middle East's real estate sector, boasts impressive financial metrics that highlight its potential. The company's earnings growth of 165.8% outpaced the industry's 121.8%, reflecting robust performance despite a significant TRY6.1 billion one-off gain impacting recent results. Over five years, RGYAS has effectively reduced its debt to equity ratio from 144.8% to 26.9%, indicating improved financial health with a satisfactory net debt to equity ratio of 20%. Additionally, its price-to-earnings ratio of 3.3x is attractively below the TR market average of 17.2x, suggesting potential value for investors seeking opportunities in this region's dynamic market landscape.

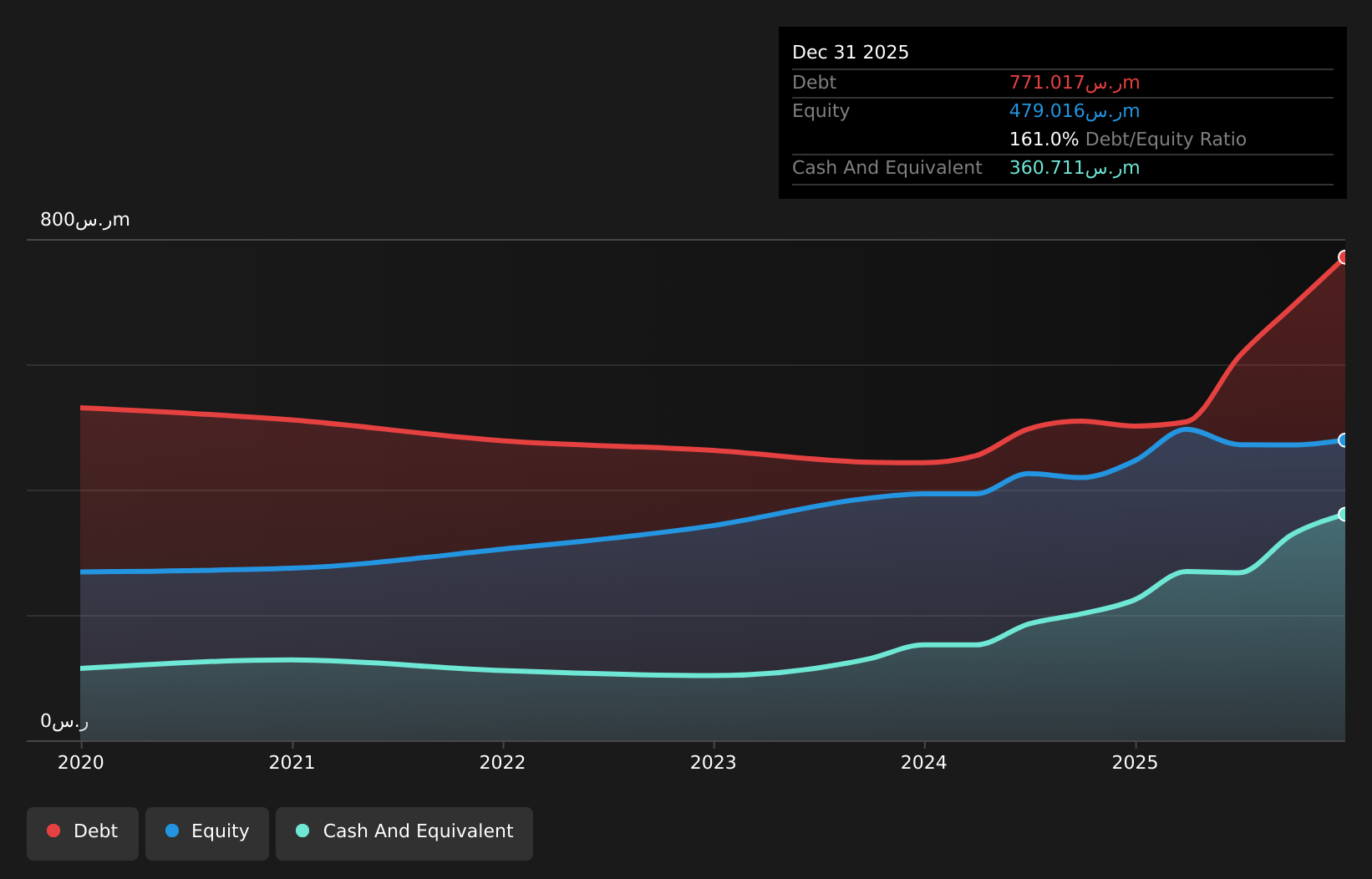

Miahona (SASE:2084)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Miahona Company Limited operates in the Kingdom of Saudi Arabia, offering water facilities and treatment services, with a market capitalization of SAR2.69 billion.

Operations: The company's primary revenue stream comes from water utilities and wastewater treatment services, generating SAR699.65 million.

Miahona, a notable player in the Middle East's water utilities sector, reported impressive financial growth with earnings surging 77.8% over the past year, significantly outpacing industry growth of 5.1%. Sales reached SAR 699.65 million from SAR 385.09 million previously, while net income climbed to SAR 72.41 million from SAR 40.73 million a year ago, reflecting robust operational performance. Despite a high net debt to equity ratio of 85.7%, debt levels have decreased over the last five years from an even higher base of 186.2%. With EBIT covering interest payments by a comfortable margin of 14 times, Miahona seems well-positioned financially for future endeavors in its industry context.

Key Takeaways

- Unlock more gems! Our Middle Eastern Undiscovered Gems With Strong Fundamentals screener has unearthed 209 more companies for you to explore.Click here to unveil our expertly curated list of 212 Middle Eastern Undiscovered Gems With Strong Fundamentals.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.